The article is authored by Square Capital research team. Square Capital is India's first unbiased loan advisor for best deals on all types of loans and is known for its unmatched advisory services. It is the mortgage arm of Square Capital - India's largest real estate transactions company.

Across the globe it is the government in-power which issues the currency notes and that currency is known as the "Legal Tender" i.e. accepted by all in that country. In India it is the role of the Central bank of the country i.e Reserve Bank of India that prints currency notes and it bears the Governor's signature on it.

The primary functions of RBI is:

1.To control the supply of money in the economy i.e how much money is available for the industry or the economy and

2. The cost of credit.' meaning, and what is the price that the economy has to pay to borrow that money.

These two things (Supply of money and cost of credit) are closely monitored and controlled by RBI. The inflation and growth in the economy are primarily impacted by these two factors.

The various methods employed by the RBI to control credit creation power of the commercial banks can be classified into two groups, viz., quantitative controls and qualitative controls.

Quantitative controls are designed to regulate the volume of credit created by the banking system Qualitative measures or selective methods are designed to regulate the flow of credit in specific uses.

To control inflation and the growth, RBI uses certain tools like CASH RESERVE RATIO, STATUTORY LIQUIDITY RATIO, REPO RATE, and REVERSE REPO RATE

What is Statutory Liquidity Ratio (SLR)?

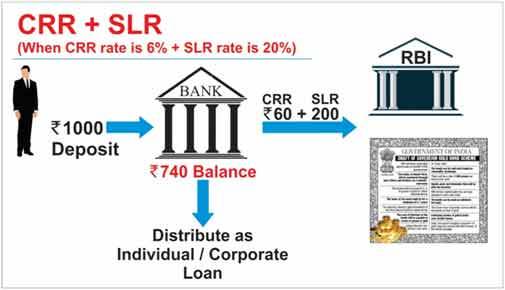

Besides CRR, Banks have to invest certain percentage of their deposits in specified financial securities like Central Government or State Government securities. This percentage is known as SLR.

This money is predominantly invested in government approved securities (bonds), Gold, which mean the banks can earn some amount as 'interest' on these investments as against CRR where they do not earn anything.

Example - An Individual deposits say Rs 1000 in bank. Then Bank receives Rs 1000 and has to keep some percentage of it with RBI as SLR. If the prevailing SLR is 20% then they will have to invest Rs 200 in Government Securities

Higher reserve requirements such as SLR make banks relatively safe (as a certain portion of their deposits are always redeemable) but at the same time restrict their capacity to lend. To that extent, lowering of reserve requirement increases the resources available with a bank to lend and helps control inflation and propels growth.

What is Repo Rate?

When we need money, we take loans from banks. And banks charge certain interest rate on these loans. This is called as cost of credit (the rate at which we borrow the money).

Similarly, when banks need money they approach RBI. The rate at which banks borrow money from the RBI by selling their surplus government securities to RBI is known as "Repo Rate." Repo rate is short form of Repurchase Rate. Generally, these loans are for short durations up to 2 weeks.

It simply means Repo Rate is the rate at which RBI lends money to commercial banks against the pledge of government securities whenever the banks are in need of funds to meet their day-to-day obligations.

Banks enter into an agreement with the RBI to repurchase the same pledged government securities at a future date at a pre-determined price. RBI manages this repo rate which is the cost of credit for the bank.

Example - If repo rate is 5% , and bank takes loan of Rs 1000 from RBI , they will pay interest of Rs 50 to RBI.

So, higher the repo rate higher the cost of short-term money and vice versa.

Higher repo rate may slowdown the growth of the economy.

If the repo rate is low then banks can charge lower interest rates on the loans taken by us.

So whenever the repo rate is cut, can we expect both the deposit rates and lending rates of banks to come down to some extent?

This may or may not happen every time. The lending rate of banks goes down to the existing bank borrowers only when the banks reduce their base rates (Base Rate is the minimum rate below which Banks are not permitted to lend) as all lending rates of banks are linked to the base rate of every bank. In the absence of a cut in the base rate, the repo rate cut does not get automatically transmitted to the individual bank customers. This is the reason why you might have observed that your loan EMIsremain same even after RBI lowers the repo rates.

Banks check various other factors (like credit to deposit ratios etc.,) before reducing the Base rates.

What is Reverse Repo Rate?

Reverse repo rate is the rate of interest offered by RBI, when banks deposit their surplus funds with the RBI for short periods. When banks have surplus funds but have no lending (or) investment options, they deposit such funds with RBI. Banks earn interest on such funds.

Current CRR, SLR, Repo and Reverse Repo Rates:

The current rates are (as of last week of December 2015) - CRR is 4 % , SLR is 21.50%, Repo Rate is 8% and Reverse Repo Rate is 7%.

RBI website has repository of all CRR, SLR & Base Rates

Impact of Repo Rate /CRR/SLR rate cut :

Here are some points on 'how the RBI's rate cuts impact homeloans-

'Chennai-Bengaluru in 1:13 hours, Varanasi-Siliguri in 2:55': Ashwini Vaishnaw maps high-speed rail plan

'Chennai-Bengaluru in 1:13 hours, Varanasi-Siliguri in 2:55': Ashwini Vaishnaw maps high-speed rail plan Budget 2026: Arbitrage fund returns may drop 25–30 bps after STT rate revision, says Edelweiss MF

Budget 2026: Arbitrage fund returns may drop 25–30 bps after STT rate revision, says Edelweiss MF 'America First policy unintentionally pushing US allies toward sovereign AI,' warns Coursera co-founder

'America First policy unintentionally pushing US allies toward sovereign AI,' warns Coursera co-founder Adani Ports, HAL, M&M, LG India among top picks post Budget for upto 40% upside potential

Adani Ports, HAL, M&M, LG India among top picks post Budget for upto 40% upside potential 18% excise duty on unmanufactured tobacco withdrawn; will tobacco stocks be impacted?

18% excise duty on unmanufactured tobacco withdrawn; will tobacco stocks be impacted? Why FIIs Are Dumping India: Valuations, Earnings & The Budget Signal, Raamdeo Agrawal Explains

Why FIIs Are Dumping India: Valuations, Earnings & The Budget Signal, Raamdeo Agrawal Explains STT Hike: Curbing Excess Or Hurting Markets? Raamdeo Agrawal Speaks

STT Hike: Curbing Excess Or Hurting Markets? Raamdeo Agrawal Speaks Union Budget 2026: Why Policy Certainty Matters More Than Populism

Union Budget 2026: Why Policy Certainty Matters More Than Populism Budget’s Biggest Gorilla: Raamdeo Agrawal On Data Centre Opportunity

Budget’s Biggest Gorilla: Raamdeo Agrawal On Data Centre Opportunity Post Budget Analysis | What Budget 2026 Means For Indian Agriculture | BT Exclusive

Post Budget Analysis | What Budget 2026 Means For Indian Agriculture | BT Exclusive Budget 2026 boosts India's data centre ambition; MOFSL's Raamdeo Agrawal on FPI selling, rupee fall

Budget 2026 boosts India's data centre ambition; MOFSL's Raamdeo Agrawal on FPI selling, rupee fall HAL, BEL, BDL, Astra Microwave, Zen Tech: Defence stocks to gain from Budget announcements

HAL, BEL, BDL, Astra Microwave, Zen Tech: Defence stocks to gain from Budget announcements 'Buy' Anant Raj, Delhivery & Bajaj Consumer shares: LKP Securities' analyst

'Buy' Anant Raj, Delhivery & Bajaj Consumer shares: LKP Securities' analyst NSE IPO: Unlisted shares hold firm despite STT hike in budget as issue timeline clears

NSE IPO: Unlisted shares hold firm despite STT hike in budget as issue timeline clears 'Indian markets are still domestically focused': Navam Capital MD calls for opening up for global listings

'Indian markets are still domestically focused': Navam Capital MD calls for opening up for global listings