![[Photo: Ajay Thakuri]](https://akm-img-a-in.tosshub.com/businesstoday/images/story/201607/bull660_071116124735.jpg "https://akm-img-a-in.tosshub.com/businesstoday/images/story/201607/bull660_071116124735.jpg")

The Aditya Birla Group-owned UltraTech Cement, India's largest cement maker, recently announced the acquisition of Jaiprakash Associates' (JAL's) cement plants for Rs 16,189 crore. UltraTech increased its earlier offer price by Rs 289 crore, fearing rival offers from companies such as Sajjan Jindal's JSW Cement and private equity player KKR. Though the acquisition price is still 5-10 per cent less than the cost of building the 21.2 million tonnes (MT) capacity that UltraTech will get, the revision in the offer price and the number of suitors show that India Inc. is back to betting on a sector that was among the worst hit by the slowdown in the economy after 2011/12 that hit infrastructure building and home construction alike.

Kumar Mangalam Birla, Chairman of the Aditya Birla Group, says economic revival will trigger a rise in demand for cement in the country. "India is moving to a higher growth trajectory and to that extent the cement sector is poised for pick-up in growth - around 7 per cent this financial year," he said in the 2015/16 annual report of UltraTech. The deal with JAL will take UltraTech's capacity to 91.1 MT, far ahead of its closest rival, Holcim, which has 60 MT capacity.

Holcim, which had taken over ACC and Gujarat Ambuja in 2005, is in the middle of a global merger with French cement maker Lafarge. The merger would have increased its India capacity further if it was not for the Competition Commission of India forcing Lafarge to sell its 11 MT capacity in the country. According to news reports, those in the race to grab these assets - worth around Rs 10,000 crore - include Ajay Piramal Group, Nirma, JSW Cement, Mexico's Cemex and China's Anhui Conch. In February this year, Birla Corp acquired the cement business of a wholly-owned subsidiary of Reliance Infrastructure for an enterprise value of Rs 4,800 crore. The assets included 5.08 MT capacity at Maihar in Madhya Pradesh and Kundanganj in Uttar Pradesh, and a grinding unit of 0.5 MT capacity at Butibori, Maharashtra. Last year, Birla Corp had agreed to buy two assets - 5.15 MT - of Lafarge for Rs 5,000 crore, but the deal fell through.

This consolidation couldn't have come at a better time for the industry. Cement demand has been poor for the past three-four years, even as surplus capacity and pricing pressures have been squeezing companies' margins. Things started looking up a bit only in the last financial year when production growth, which was 3.1 per cent in 2013/14, improved to 4.7 per cent. The January-March quarter was even better and saw growth of 11.48 per cent, the highest for any quarter in almost four years for the 410-MT industry, thanks in large part to the award of infrastructure and low-cost housing projects by the government. Ratings agency ICRA has projected 6 per cent growth for this financial year and 7 per cent for 2017/18.

Bottom Line/Stock Gains

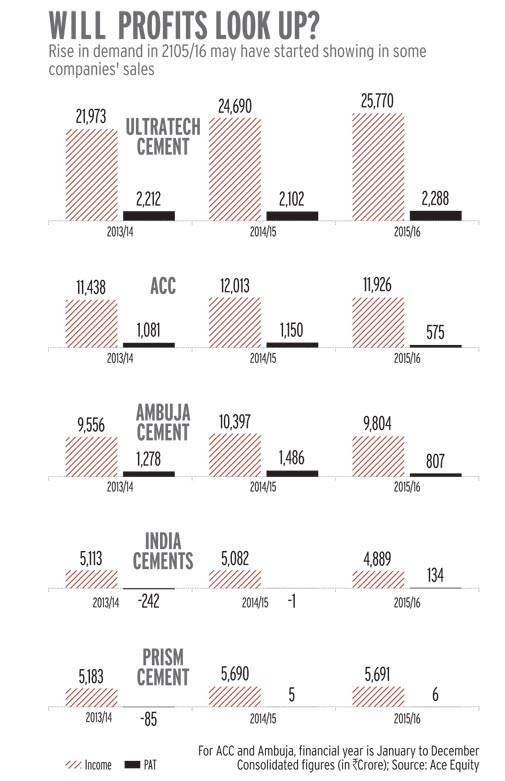

In the last financial year, ACC and Ambuja Cement revenues fell a bit. However, higher raw material costs (mostly limestone), freight charges and taxes hit bottom lines badly - ACC's net profit fell 50 per cent to Rs 575.55 crore, while Ambuja's net profit fell 45.65 per cent to Rs 807.88 crore. Shree Cement's profit less than halved to Rs 455 crore. Another global giant, the German HeidelbergCement, which sells under the brand mycem, also struggled. UltraTech, however, reported stable performance. Its revenues rose 4 per cent to Rs 25,770 crore, while profit jumped 9 per cent to Rs 2,288 crore. The company has an added advantage of low debt (Rs 10,000 crore).

The pressure eased somewhat in the March ended quarter on account of reduction in raw material costs and oil prices. The stock market is, however, expecting better tidings in the future. Shares of UltraTech, ACC, Ambuja Cements, India Cements, Shree Cement, HeidelbergCement India, JK Lakshmi Cement, Dalmia Bharat, Deccan Cements, Mangalam Cement, Birla Corporation, Sagar Cements and The Ramco Cements touched 52-week highs on the Bombay Stock Exchange towards the end of June or early July (see Stock Markets Smell Recovery).

The revenues of the top 10 cement companies rose 3 per cent to Rs 77,750 crore in the last financial year while profit fell 19 per cent to Rs 4,875 crore. Despite the weak numbers, the shares of these players rose over 20 per cent on average in the past three months. The BSE Sensex rose 6 per cent during the period.

Sanjay Sethi, Managing Director and CEO, Nestor Consulting, says pricing is crucial in the cement sector. The Indian cement industry, the world's second-largest after China's, is fragmented with close to 100 players. So, consolidation is the need of the hour. "The consolidation will give companies pricing power and improve margins," he says.

However, not all marginal companies will attract buyers. Only companies with access to resources (raw material and power/fuel) and proximity to underserved markets will. The area where the plants are located is important, too. Because it is costly to transport cement across large distances, prices depend upon demand in specific areas of the country. An ACC Cement official, for instance, said that cement prices continued to be volatile in the March quarter. "The pricing situation improved in North but remained weak in East and West. South is stable compared to the rest of the country," he says.

Demand Push

After two-three years of slowdown, expectation soared high when the NDA government took charge in 2014 and promised projects such as 100 smart cities, Housing For All and Pradhan Mantri Gram Sadak Yojana. All these are expected to increase the demand for cement, which analysts say is expected to touch 550-600 MT by 2025. The biggest buyer of cement in India is the housing sector, accounting for about 67 per cent consumption. The others are infrastructure (13 per cent), commercial construction (11 per cent) and industrial construction (9 per cent). Even the focus on roads will push up demand as the government plans to use cement instead of bitumen for a large number of big road projects; the former is more durable.

To keep pace, manufacturers are expected to add 56 MT capacity over the next three years. The capacity may rise 8 per cent to 395 MT by next year and 421 MT by the end of 2017, say analysts. The top 20 cement companies account for 70 per cent production. A total of 188 large cement plants account for 97 per cent installed capacity. Of these large plants, 77 are in Andhra Pradesh, Rajasthan and Tamil Nadu.

A big part of new growth is expected from newer markets in eastern states. Over the next 10 years, India could become a big exporter of clinker and gray cement to Middle-East, Africa and other developing nations. Plants near ports, for instance in Gujarat and Visakhapatnam, will have an advantage if that happens.

The government's investment in infrastructure - roads, metro rail, airports and inland waterways - will also push up demand. Another positive is the above-normal monsoon that is expected to revive construction activity in rural areas.

Deven Choksey, Managing Director, KR Choksey Investment Managers, says the growth phase has begun. "The revival of low-cost housing and infrastructure projects has triggered growth. The building of industrial corridors will also help the industry," he says. Cement sales are an early indicator of rise in economic activity.

However, private sector investment must also pick up if the sector is to do well. Many cement companies are betting on that happening. The JSW Group plans to expand capacity from 5 MT to 30 MT by setting up grinding units closer to its steel plants. It will set up a three-MT clinker plant at Chittapur in Karnataka at a cost of Rs 2,500 crore. Dalmia Bharat has already invested around Rs 2,000 crore in expanding in the North-East, where it has three plants - one in Meghalaya and two in Assam. UltraTech, too, is charting out its next phase of greenfield expansion after the spate of acquisitions. It plans to set up two grinding units in Bihar and West Bengal.

S.P. Tulsian, an independent analyst, says that the rise in offtake will lead to higher capacity utilisation. "The states are competing to build infrastructure projects. This is a good sign for the construction and cement industry. The companies must improve their efficiencies to cash in on the opportunities," he says.

The boom, it seems, is just at the door step.