We don't support landscape mode yet. Please go back to portrait mode for the best experience

The current mood of the market is aptly reflected in the latest edition of the BT500 study, as the combined valuation of the Top 500 companies on the list has risen. but the gains have not been as spectacular as 2022, mirroring the sentiment of investors

The second week of October saw something curious happen. The Indian stock markets were in the doldrums after a strong September—both the benchmark S&P BSE Sensex and the Nifty 50 had touched their respective all-time highs that month.

But even as the domestic equity markets were facing headwinds on account of a combination of geopolitical and macroeconomic concerns, global financial major CLSA said it was raising its India portfolio allocation on account of factors like strong credit impulse, improving external balance dynamics, robust GDP and earnings per share (EPS) growth, increasing profitability, and a supportive macro outlook, among other things. The bullish note by CLSA came as a ray of optimism in an otherwise bearish month—October has been the worst month in CY2023 with the Sensex shedding nearly 3 per cent.

What was the reason for this dichotomy? Simply put, the Indian stock markets were witnessing a confluence of sentiments—persistent conviction in the long-term growth story and heightened volatility in the short-term leading to increasing uncertainty amongst the investing community. That, in a nutshell, also sums up the latest edition of the BT500 study—an exhaustive analysis that Business Today has done every year since 1992.

“ Emerging market flows will stay iffy and India may continue to see outflows. But [the] mediumterm looks very good to us... India will benefit from strong positioning geopolitically also... All these factors are a positive in total ”

R. Venkataraman

Chairman

Iifl Securities

The cumulative growth in the valuations of the 500 biggest companies by market capitalisation has been subdued this year compared to last year, even though there have been more instances of firms registering a rise in their respective market capitalisations when compared to those whose valuations have shrunk. Some of the biggest companies on the BT500 list have seen their valuations erode even as their top line and bottom line rose, reflecting the jittery sentiments of investors.

But the BT500 is not merely a listing of the biggest firms; it is also a deep dive into how the companies have fared in terms of important metrics like income, profit, debt, and other financial ratios. The rankings are based on the average market capitalisation for the 12-month period from October 1, 2022, to September 30, 2023.

On an aggregate basis, the combined average market capitalisation of the BT500 companies this year was pegged at Rs 261.53 lakh crore, registering a growth of 4 per cent when compared to the previous year’s figure of Rs 251.33 lakh crore. More importantly, it is significantly lower than last year’s rise of 26 per cent in the combined average market capitalisation of the Top 500 companies.

What is significant, though, is that the almost flattish growth in the valuations came at a time when the Sensex was touching new highs consistently—the BT500 study period saw the 30-share barometer gaining nearly 15 per cent or around 8,400 points. Further, the subdued rise happened even as more than 300 companies registered a rise in their respective market capitalisations in this year’s BT500 list and over 50 firms saw their profits more than double in FY23, when compared to the previous fiscal.

Another interesting trend witnessed this year was around the new entrants as a majority of the debutants were comparatively much smaller in size when compared to their counterparts in the previous year’s study. But first let’s have a look at the toppers that include the Street favourites—that have remained favourites consistently over the years—even as some of the biggies saw their valuations dip and were overtaken by entities that were much smaller earlier.

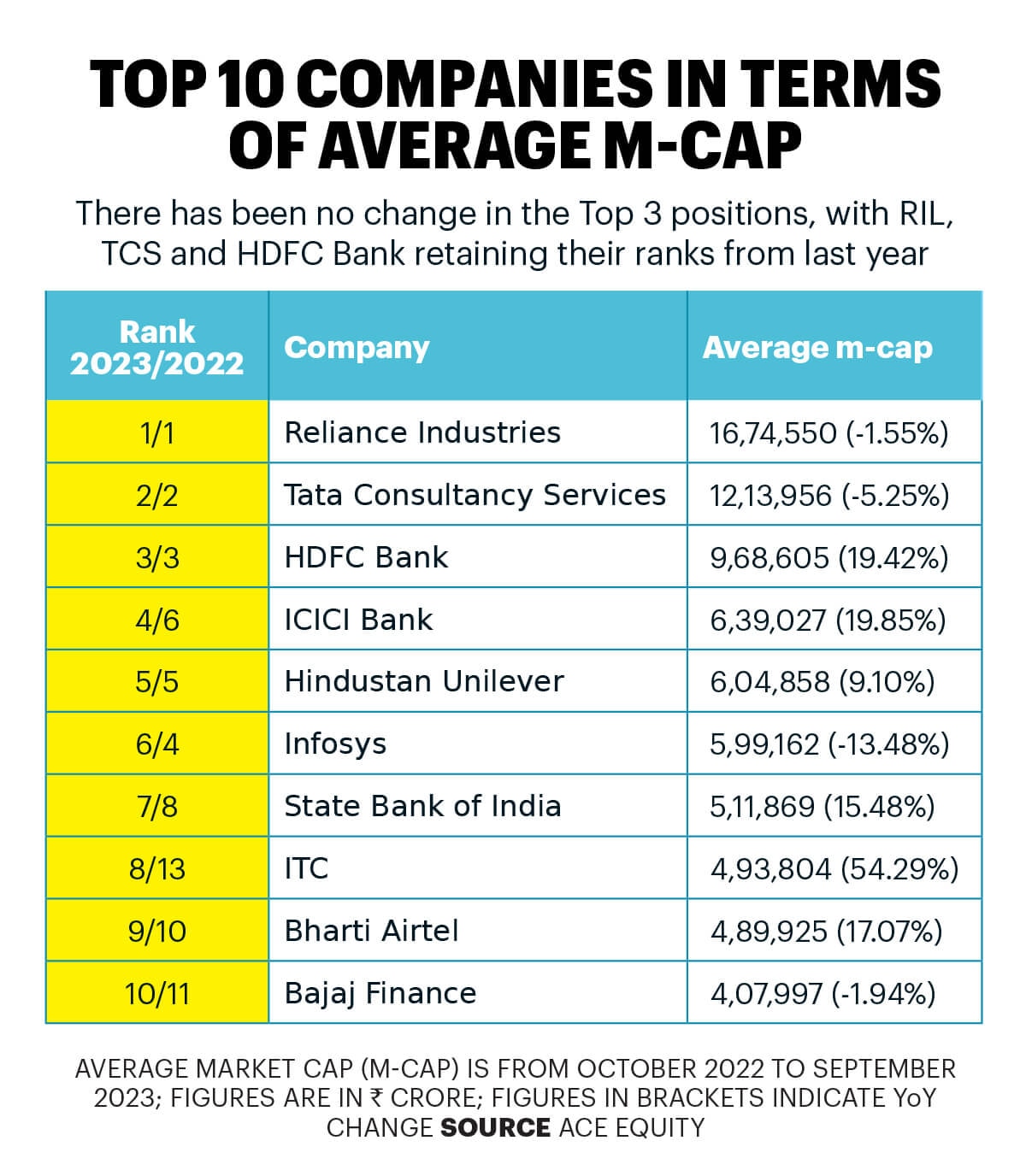

There has been no change in the Top 3 occupants on the BT500 list with Reliance Industries Ltd (RIL) topping it, followed by Tata Consultancy Services (TCS) and HDFC Bank. The private sector lender registered a 19.4 per cent rise in its average market capitalisation during the period under review, while the other two saw their valuations dip.

Meanwhile, ICICI Bank has broken into the Top 5 this year by jumping two positions to No. 4, while FMCG major Hindustan Unilever (HUL) occupies the No. 5 spot. It is followed by Infosys and State Bank of India (SBI)—in that order—while ITC breaks into the Top 10 at No. 8; the FMCG major was at No. 13 in 2022 and has seen a 54.3 per cent rise in its valuation. Bharti Airtel and Bajaj Finance at No. 9 and No. 10, respectively, round up the Top 10.

In terms of valuation, four of the Top 10 firms—RIL, TCS, Infosys and Bajaj Finance—have seen their respective market capitalisations dip even as the aggregate valuation of the 10 companies has risen a little over 6 per cent. Insurance behemoth Life Insurance Corporation (LIC), which made a high-profile debut at No. 9 on the list in 2022, follows the Top 10 this year at No. 11, with a 10.8 per cent fall in its valuation.

Another interesting trend has been the performance of Adani Group firms. In contrast to last year, when most group firms had made stellar gains in market capitalisation, this year, barring Adani Enterprises, Adani Power and Ambuja Cements, the rest of the companies have seen their valuations dip and as a result have seen their rankings slide in the BT500 list.

Why has there been a subdued growth in valuations, a conspicuous trend in this year’s BT500 list? Market participants attribute it to a combination of factors including a spike in crude prices and geopolitical concerns, among other fears. “There have been concerns about crude oil levels, and while they are back at $80 (Brent), they had been till recently above $85, and those levels begin worrying markets, as India is a major crude importer,” says R. Venkataraman, Chairman of IIFL Securities. He explains that the crude oil prices had spiked because of the worsening geopolitical situation, with the Russia-Ukraine war continuing and the Israel-Hamas conflict flaring up. “Further, the US Fed had initially sent the markets tumbling with another higher-for-longer comment before changing to a more dovish stance… India-specific economic factors that are worrisome are not many, but worries about the BJP failing to get a clear majority on its own in next year’s general elections [exist],” he adds.

That also explains the vagaries seen in the country’s market capitalisation to GDP over the years, and more importantly, in the recent past. A recent report by Motilal Oswal Financial Services highlights this trend and states that this ratio fell to 95 per cent in FY23 from 113 per cent in FY22 and 103 per cent in FY21. In the current financial year, the ratio is pegged at 107 per cent—much above its long-term average of around 80 per cent—per the domestic broking major’s analysis.

Besides valuations, the BT500 study also has interesting insights with respect to the overall health of the biggest companies of the country. For instance, this year’s BT500 list includes 47 companies that saw their profit after tax (PAT) more than double in FY23 when compared to the previous financial year. This was, however, lower than last year’s study that had 77 such instances.

Some of the prominent names that saw their PAT more than double in FY23 include Adani Enterprises, Bata India, Ceat, Sun Pharmaceutical, Just Dial, VIP Industries, Adani Power, Maruti Suzuki India and Raymond. On the other hand, companies like SAIL, BPCL, Tata Steel, JSW Steel, Glenmark Pharmaceuticals, Jindal Steel & Power, GAIL (India), Indian Oil Corporation, ACC, NMDC, and Vedanta saw a significant fall in their PAT in FY23 when compared to FY22.

“FY23 had been a strong earnings year for auto, capital goods, NBFCs, insurance firms, and banks, as well as other sectors like tyres, real estate, etc., with a very strong growth in mid-caps and small-caps. On the other hand, cement, pharma, diagnostics saw a rout… Further deceleration should be expected as monetary tightening globally throughout 2022 and 2023 takes its toll on the growth of Indian companies’ earnings,” explains Venkataraman.

On a different note, the cumulative debt of the BT500 firms (ex-BFSI) in FY23 was pegged at Rs 33.34 lakh crore, against cash and bank balance of nearly Rs 8 lakh crore. Some of the companies that saw the maximum jump in their absolute debt levels include Sun Pharma, TV18 Broadcast, Hindustan Zinc, Biocon, JSW Energy, Network 18 Media & Investments, GAIL (India) and Aurobindo Pharma, among others. Meanwhile, entities like DLF, Mangalore Refinery & Petrochemicals, Indus Towers, Adani Power, Tata Chemicals, Tata Motors, Apollo Tyres and Adani Enterprises lowered their absolute debt in FY23.

In terms of the largest quantum of debt (ex-BFSI), RIL tops the charts with a debt of nearly Rs 3.14 lakh crore followed by NTPC (Rs 2.2 lakh crore), Vodafone India (Rs 2.02 lakh crore), Bharti Airtel (Rs 1.66 lakh crore), and Indian Oil Corporation (Rs 1.4 lakh crore).

RIL and Indian Oil Corporation, however, also occupy the top two spots, respectively, in terms of companies with the highest quantum of total income. The total income of RIL and Indian Oil Corporation was pegged at Rs 8.91 lakh crore and Rs 8.46 lakh crore, respectively, in FY23—both registering strong growth over FY22.

With important metrics being captured in the BT500 study every year, it also provides insights on the companies that are bleeding badly. Not surprisingly, the list of the biggest loss-making companies features many new-age digital majors. For instance, One97 Communications—the parent entity of Paytm—registered a net loss of Rs 1,777 crore in FY23 though it is lower than the previous fiscal’s Rs 2,396 crore. Delhivery, Zomato, and PB Fintech (Policybazaar) are also among the top loss-making companies in the BT500 list though the quantum of losses in FY23 has been brought down by each of the digital majors. Besides these companies, old economy firms from the energy, infrastructure and utilities space also feature on the loss-making list.

On an overall basis, however, there are only 30 loss-making companies in the BT500 list that clearly shows that both the study and India Inc. have fundamentally strong and robust companies for investors to choose from. This assumes significance as experts believe that while the stock markets are facing headwinds, there are plenty of tailwinds as well.

“Emerging market flows will stay iffy and India may continue to see outflows. But [the] medium-term looks very good to us, and after perhaps more than a decade, the US Fed is armed with 550 basis points of loosening capability as inflation cools, and that augurs well for global liquidity, and hence rates and growth,” says Venkataraman, adding that India will benefit from strong positioning geopolitically as well. “All these factors are a positive in total,” he says, adding that the outcome of the forthcoming general elections remains the biggest risk to markets.

Indeed, but for investors looking to invest in companies with strong fundamentals and an equally robust growth potential, the BT500 list is a good place to start.

UI Developer : Pankaj Negi

Creative Producer : Raj Verma