We don't support landscape mode yet. Please go back to portrait mode for the best experience

With the listing of Jio Financial Services‚ Reliance Chairman Mukesh Ambani has lined up all his ducks. Will the new NBFC disrupt the financial space the way Jio roiled mobile telephony despite being a late entrant?

In 2004, Jack Ma, the Co-founder of China’s Alibaba, an e-commerce business then just five years old and yet to become a world-beater, launched payments platform Alipay for its retail customers and merchants. In a decade, Alipay (later reborn as Ant Financial) became China’s leading financial services giant, offering a digital wallet, consumer credit, money market funds, wealth management, and a digital-only bank for small enterprises. Ant Financial soon had $600 billion in assets under management as it layered various financial services atop the e-commerce platform. What also worked was China’s underserved and unbanked population, with an aspirational middle class—and a surge in smartphone use. China’s financial services sector, dominated by state-owned banks, was also ripe for disruption. Ma had struck gold.

Mukesh Ambani’s Jio Financial Services, dubbed the group’s ‘fourth engine’ after oil, telecom, and retail, aims to mirror Ma by leveraging its established consumer-facing businesses: retail and telecom.

The similarities with Ma’s model are hard to ignore, as the key is the proprietary payments or retail transaction data that will help Jio create a business model around lending, asset management, insurance, and stock broking. The 66-year-old Ambani, Reliance Industries Ltd’s (RIL) Chairman & MD, is taking one step at a time. Ambani established a beachhead in the financial services industry by acquiring a payments bank licence in 2015, two months after the Reserve Bank of India invited applications for this new class of banks. Payments banks are meant for payments and remittances, can accept small savings, and issue debit cards but not credit cards.

The market is large enough. .. Even [after] being present in 4‚000 cities [with] assets close to Rs 3 lakh crore‚ we still have less than 2 per cent [share in] India’s credit market

Sanjiv Bajaj

CMD

Bajaj Finserv

The market got a whiff of the group’s ambitions, but Reliance never scaled up the business. Then, in November 2022, ICICI Bank veteran K.V. Kamath joined the RIL board as an independent director. Jio Financial Services Ltd was spun out from Reliance in July this year.

On July 8, a week after Jio Financial Services (JFS) was born, it announced that Ambani’s daughter Isha had joined its board. On August 21, at the listing ceremony of JFS, Kamath, now its Chairman, said, “It’s possible to predict that within the next eight to nine years, our GDP could double, reaching around $8 trillion. This presents a tremendous opportunity for India.”

The $118-billion group has the war chest, management bandwidth, group synergies, and the ability to attract top-notch talent—like it has for its senior management team from ICICI Bank, State Bank of India and BRICS-sponsored New Development Bank.

“They have an exceptional ability to see large business opportunities,” says Nirav Shah, Managing Director (Investment Banking) at Equirus Capital. “Their knack for timing disruptions is impeccable. The execution from the ground up is outstanding.”

Ambani explained the JFS gambit to shareholders at RIL’s annual general meeting (AGM) on August 28. “JFS has been conceptualised to fill a critical gap in the financial services needs of a large section of the Indian economy, mainly in the informal and underserved sectors in rural, semi-urban, and urban areas,” he said.

Typical of Ambani, JFS wants the lion’s share of the fast-growing financial services market via organic and inorganic growth—grabbing products, geographies and licences. It has a modular framework with independent CEOs for each business. So Vinod Easwaran is the CEO of Reliance Payments Bank, and A.R. Ramesh heads Reliance Payment Solutions Ltd.

RIL has had a history of ruffling the feathers of established players when it enters a sector. When it entered telecom with Jio in 2016, it bled the leaders with its low pricing. “Forget telecom or retail; when they started growing mangoes at the Jamnagar refinery complex, they quickly became Asia’s largest mango exporter,” says a banker. However, financial services are certainly not low-hanging fruit.

Two years ago, investors and experts couldn’t understand why Ambani bought Justdial, an online Yellow Pages firm that featured dealers and SMEs. Reliance was after Justdial’s treasure trove of partner merchant data. Justdial was also powering small players with technology and payment capabilities. A few years ago, RIL partnered with Microsoft to adopt leading technologies, such as data analytics, AI, blockchain, etc., for SMEs. Ma’s Ant initially provided digital tools to vendors, gaining insights into their operations. Ambani appears to be following a similar path. (Ma unsuccessfully ran a Chinese Yellow Pages business.)

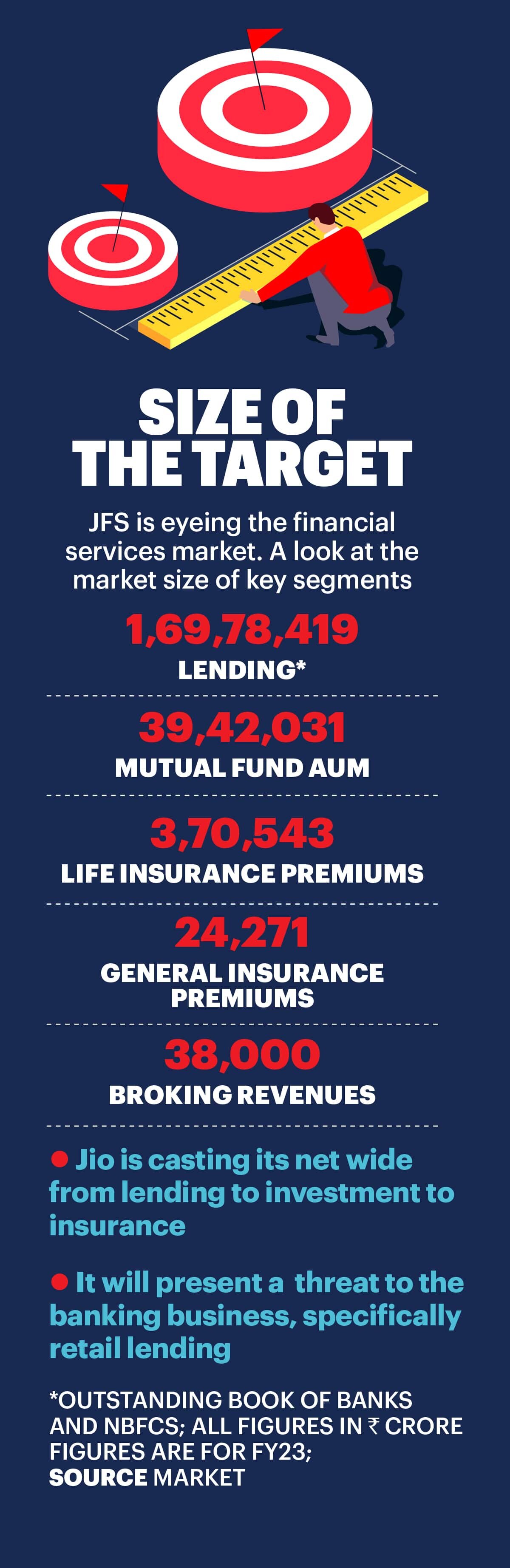

But what’s bigger is RIL’s telecom data of 426 million users—usage patterns, roaming, data consumption, family usage, and default records. Reliance Retail has data on 18,000-plus stores, with customers in grocery, consumer electronics, fashion, lifestyle, and pharma. (See box A Galaxy of Opportunities.) The delivery model is a cost-effective digital-first approach using the web, apps, and physical stores to offer products.

A public sector banker says, “They have the advantage of starting with a clean slate when traditional, well-established players are struggling with technological changes.” The cloud-based, scaleable technology model of JFS gives it huge savings. With Ma, it was timing; JFS has before it the entire India Stack of Aadhaar, e-sign, eKYC, UPI, ONDC, and the Account Aggregator framework to scale its operations.

So, what’s on offer from JFS?

K.V. Kamath‚ Chairman, Jio Financial Services

JFS is a non-banking financial company (NBFC) holding the reins of a lender entrenched in consumer durables, an asset management company (AMC), an insurance firm looking for a big-name partner, and an equity broker.

Reliance Retail Finance Ltd offers unsecured and secured loans to consumers and merchants. It has been offering loans in a small way since 2019. It will leverage the group’s retail operations in the consumer electronics, grocery, and fashion segments. Initially, JFS is targeting consumer durables financing via the EMI model through the 400-plus Reliance Digital stores. Reliance Digital and commerce generated nearly Rs 50,000 crore in revenue in 2022-23.

“The primary focus of consumer durables financing has traditionally been electronics and mobile devices, which still make up a significant portion of the market,” says Vikas Garg, Co-founder and CEO of fintech start-up Paytail. But JFS also has the grocery and fashion formats to capitalise on the credit boom. It will begin with consumer durables subsidised by manufacturers, OEMs, or dealers to build a database on repayments and defaults. Then, it will cross-sell other products, including secured loans, to those with a good credit history.

The merchant lending vertical will offer financing to merchants in grocery, digital fashion, and pharma— formats that don’t have access to cheap funds. The products include short-term personal loans, trade financing, loans for store upgrades, and unsecured business loans.

It is already helping merchants with payment capabilities. JFS has a good database of kirana stores to underwrite them for short-term working capital loans, especially during peak seasons such as festivals. JioMart offers an online shopping platform by partnering with local mom-and-pop stores.

AMCs... don’t demand significant capital unless there’s a strategy to heavily discount or offer low fees. It’s a profitable business at scale

Tej Shah

Portfolio Manager

Marcellus Investment Managers

The loans vertical for MSMEs or micro, small and medium enterprises will offer working capital financing to distributors and suppliers, who end up tapping high-interest informal channels for small loans. A recent report from Avendus Capital highlighted that the small-ticket MSME lending sector faces a credit shortfall exceeding $120 billion.

Ambani is also catching the passive-investing wave, which comprises index funds and exchange-traded funds (ETFs). Last month, JFS sealed a deal with the world’s biggest AMC, BlackRock, for a 50:50 joint venture in a market that has nearly four dozen players. BlackRock is a dominant player in passive investment, which involves tracking indices rather than individual stocks. Its ETFs are very popular globally. Jio-BlackRock, with a $150-million investment, hopes to stand out. In less than a decade, the AUM of passive funds accounts for a fifth of the market. Jio’s strategy of using the group’s ecosystem and digital-first approach could help reduce distribution expenses, which it could pass on to small unit holders. BlackRock is no stranger to the Indian market; it cut its teeth with a joint venture in DSP Mutual Fund before parting ways about five years ago.

The AMC business has good margins. For instance, HDFC AMC reported a 26 per cent return on equity, an income of Rs2,482 crore and a profit of Rs 1,423 crore in 2022-23. “AMCs operate efficiently with minimal capital. They don’t demand significant capital unless there’s a strategy to discount heavily or offer low fees,” says Tej Shah, Portfolio Manager at Marcellus Investment Managers.

Following the 2016 demonetisation, when Vijay Shekhar Sharma’s Paytm and Google Pay were amassing payments customers in the QR code frenzy by offering cash backs, Ambani, who had a payments banking licence, kept out of the fray.

Jio Payments’ senior executives would regularly present a business case in their review meetings. Ambani would listen patiently without uttering a word, perplexing the senior executives. In hindsight, the billionaire’s plan to leverage his retail and telecom networks becomes clear.

Jio’s payments bank licence allows it to offer current accounts and savings accounts (the so-called CASA combo of cheap funds) but doesn’t allow lending activity. Jio has a UPI app that allows customers to recharge their mobiles, pay utility bills, shop online, and purchase travel tickets, among other things. It also offers third-party investment, insurance, and borrowing products. Jio Payments Bank can apply for a small finance bank licence.

The equity broking industry is undergoing rapid transformation. Discount brokerage firms have quickly scaled their operations, intensifying competition

Arun Chaudhry

Chief Business Officer

m.Stock, Mirae Asset Capital Markets

Ambani is scouting for reputable global partners in life-, general-, and health insurance businesses. The insurance industry has everything going for it: low insurance penetration, a young population, rising life expectancy, growing consumer awareness about financial security, etc. Health insurance is emerging as the fastest-growing segment. “It will use predictive data analytics to co-create contextual products with partners and cater to customer requirements in a truly unique way,” said Ambani at the AGM. Currently, Reliance Retail Insurance Broking distributes insurance products and earns commissions. While life insurance is a cash guzzler because of agent commissions, the general and health insurance businesses don’t require much capital.

Equity brokerage is yet another area where JFS will likely make its presence felt. Technology advances, regulatory changes and shifting investor preferences are rocking India’s Rs 38,000-crore equity-broking industry. Zerodha revolutionised the equity brokerage business and grabbed a significant market share by offering a zero-brokerage model. New players, such as Groww, Upstox, and 5paisa, generate revenue from subscription fees, margin interest, or premium services.

“The business landscape has also evolved, with companies now offering fund-based products such as margin funding,” says Arun Chaudhry, CBO at m.Stock, a trading app that is part of South Korea’s Mirae Asset group. The surge in demat accounts after the Covid-19 pandemic’s lockdowns and disruptions has fuelled a growing market for cross-selling services like mutual funds, wealth management, research, and financial planning. It is a sector ripe for disruption. Enter JFS.

JFS has to quickly adapt and find its unique strengths in various business models, whether advisory services, margin funding, or financial planning, to achieve growth and success. “The increased regulations have made the industry more transparent and trustworthy, giving people confidence that their interests are being safeguarded,” says Chaudhry.

Corporates have historically faced challenges in the BFSI sector, often unable to innovate and scale up. “Past efforts at ecosystem monetisation have also fallen short,” believes Tej of Marcellus. The lone exception is Bajaj Finance, which has not only made consumer durables financing a success but also given banks and NBFCs a run for their money. Industry experts highlight that the leaders in commercial-vehicle financing are not manufacturers such as Ashok Leyland or the Tata group, which have finance units. The leaders are Cholamandalam and Sundaram Finance. A captive business doesn’t necessarily mean success. It will not be a cakewalk for JFS, which will now have to deal with multiple regulators in lending, payments, mutual funds, and insurance. New NBFCs from Piramal, Poonawalla, and Godrej are also spreading their wings. In addition, JFS will come under RBI’s top tier NBFCs (numbering 15) with significantly higher supervision. JFS is entering at a time when RBI is encouraging large-scale NBFCs to transition into full-fledged banks. The regulations governing NBFCs are almost like those governing banks regarding NPA recognition or liquidity requirements. That was one of the reasons mortgage giant HDFC Ltd merged with HDFC Bank.

Some experts suggest that there could be a change in RBI’s policy towards large conglomerates. Three years ago, an internal RBI group recommended allowing industrial houses into the banking sector. They also suggested that large NBFCs with assets over Rs 50,000 crore could become banks. And even if RBI allows industrial houses, banking is a diversified business and highly competitive with segments like corporate loans, MSME loans, agri-business loans, and retail loans. “There can’t be a monopolistic or oligopolistic sort of market in financial services. Jio’s kind of disruption (telecom, retail) is not possible in the BFSI space,” the experts say.

When an analyst asked Bajaj Finance’s Managing Director, Rajeev Jain, about the competition, he said, “What I can control is working towards achieving our goal of reaching 100 million consumers, which aligns with our ambition. Our aim is to capture a significant portion of these 100 million consumers’ payments and financial services needs, with a strong emphasis on providing a seamless experience. That’s my focus.”

“Jio could do some disruption in terms of technology or exploiting the synergy within the group,” says Ajit Kabi, Banking Analyst at broking firm LKP Securities. The targeted market of JFS, smaller cities and towns, is also on the radar of established banks such as HDFC Bank and ICICI Bank. Lending is a highly leveraged business. Mahesh Shukla, CEO and Founder of PayMe India, an NBFC, says it is essential to consistently secure capital at a low cost while monitoring for any decline in asset quality. “Collection is a matter of customer service, as it is important to treat customers with respect and not be overly aggressive,” says Shukla.

In the MSME segment, market players have historically faced high non-performing assets or NPAs. “When the cycle changes, it is all about collection,” says a private banker.

Similarly, Bajaj Finserv, Zerodha Broking, and Samir Arora’s Helios Capital, among others, are entering the mutual funds space, and some are trying passive funds, which JFS wants to do. Sanjiv Bajaj, Chairman and Managing Director of Bajaj Finserv, which has an AMC licence, recently said he plans to sell mutual funds to the company’s 100 million existing customers.

There is also a big challenge on the funding side, as NBFCs are not allowed to raise CASA deposits, the low-cost funds loved by banks. There is also a threat of asset-liability mismatches if one lends long-term, as the funds available are short-term.

“They have many advantages to begin with, but they will need to undergo a learning process to refine their strategy or business model,” says Rohit Garg, Co-founder & CEO of lending platform SmartCoin.

RBI is already very cautious about allowing a higher share of unsecured lending. A consultant notes that due to Jio’s significant scale, it inherently poses some systemic risks. In addition, RBI is scrutinising the strategies of banks and NBFCs, particularly those exploring riskier avenues such as unsecured lending or offering credit to lower-rated firms. It took three decades for housing major HDFC Ltd to acquire a lending book of Rs 5.68 lakh crore. But for JFS, scaling up will be very fast. Will RBI be comfortable?

The market value of JFS is Rs 1.6 lakh crore, larger than Mahindra Finance, Cholamandalam, Muthoot, LIC Housing, etc. The third-largest NBFC by market cap, JFS is already causing unease for industry leader Bajaj Finance, whose stock has remained stagnant over the past two years.

With a net worth of Rs 1.2 lakh crore, JFS is off to a strong start. The biggest advantage for JFS is the likely AAA rating, which will allow it to raise funds at the lowest cost. The access to low-cost funds puts the company in a much better position to play the interest rate game and increase margins in the lending business. V.K. Vijayakumar, Chief Investment Strategist at Geojit Financial Services, remarks that the market valuation of JFS hinges on its anticipated future growth and its 6.1 per cent ownership in RIL.

“JFS is getting a premium valuation because the group’s execution has been phenomenal. But you are paying for it now,” says a global private equity player. Insurance behemoth Life Insurance Corporation of India (LIC), a long-term player, has already acquired 6.6 per cent of the fledgeling company.

Ma’s outspokenness and high-profile global presence cut short his rise to the top and put the brakes on the world’s largest IPO three years ago. That, in a way, positively helped Ambani, who had already unseated Ma from Asia’s top billionaires list two years ago. There are now a lot of expectations. As Ambani dives into banking and finance, he’s up against biggies such as SBI, HDFC Bank, ICICI Bank, and Kotak Mahindra Bank with a similar financial supermarket model. The industry is also heavily regulated, from lending to even collection or recovery. Ambani also has to tread carefully when dealing with group MSME customers to avoid any conflict of interest and keep an eye on the new data protection laws that safeguard people’s personal information. This makes his new venture quite challenging, unlike telecom and retail.

“Jio Financial products will not just compete with current industry benchmarks but also explore path-breaking features such as blockchain-based platforms and CBDC,” says Ambani. He’s got his finger on the pulse of the next big disruptors in global finance. Will Ambani make strides where Jack Ma stumbled? For now, the jury is still out

UI Developer : Harmeet Singh

Creative Producer : Raj Verma

Videos : Mohsin Shaikh