Volatility is defined as fluctuations and variations in stock prices and is measured with statistical tools like standard deviation, variance and beta. These variations are very strong in the short and medium term and intensify the probability of loss, thereby imparting risk. The variations stem from several factors that influence market movements. However, by using a combination of call and put options one can use volatility to one's advantage.

Long Straddle: This strategy involves buying a call and a put option with the same underlying security, expiry date and strike price. The premium and commissions paid while buying the options comprise the cost of trade. This is used when the market is expected to show large movements but it's difficult to predict its direction. It is 'direction neutral' as the investor need not be concerned about the direction. This is because if the market goes up, the investor can exercise the call option and let the put option expire. Similarly, if the market falls, the investor can exercise the put option and let the call option expire. For the strategy to be successful, the market must show large movements to give adequate profits after covering the cost of trade.

Short Straddle: This strategy is the reverse of long straddle and is implemented by selling a call and a put option with the same underlying security, strike price and expiry date. The investor receives the premium by selling the call and put options, which is his income. The strategy is useful if the market does not show any significant movement or volatility during the option tenure and the underlying security closes near the strike prices of the options sold. If the market does not move significantly, neither the call option nor the put option will be exercised and the investor can retain the entire premium that comprises his profit. However, since the investor is not holding the underlying security, a significant market movement could result in a substantial loss.

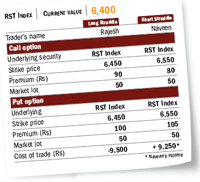

Let us consider an example. The RST Index is currently trading at 6,400. Take two investors, Rajesh and Naveen, who have totally different views on the markets. Rajesh expects it to remain extremely volatile in the near term, whereas Naveen expects it to show very little movement. The call and put options on the RST Index with strike prices of Rs 6,450 are available at Rs 90 and Rs 100, respectively, while the call and put options on the RST Index with strike prices of Rs 6,550 are available at Rs 80 and Rs 105, respectively. The market lot of the RST Index is 50 contracts. Rajesh purchases 6,450 RST Index options and enters the long straddle; Naveen sells 6,550 RST Index options and enters short straddle. The cost of trade for long straddle is Rs 9,500 [(100+90)x 50], and for short straddle, it is Rs 9,250 [(80+105)x 50]. For simplicity, we are assuming zero brokerages and commissions. Thus, Rs 9,250 is Naveen's income.

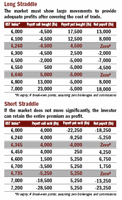

Long straddle reaches break-even points at 6,260 and 6,640. The upper break-even point of 6,640 is calculated by adding the total premium paid to the strike price of call option purchased (6,450+100+90), whereas the lower break-even point of 6,260 is calculated by subtracting the total premium paid from the strike price of put option purchased (6,450-100-90). To profit, the market should be volatile enough to move beyond these break-even points (see Long Straddle).

Short straddle reaches its break-even points at 6,365 and 6,735. The upper break-even point of 6,735 is calculated by adding the total premium received to the strike price of sold call (6,550+105+80), whereas, the lower break-even point of 6,365 is arrived at by subtracting the total premium received from the strike price of sold put (6,550-105-80). The maximum profit results if the RST Index closes at its strike price of Rs 6,550. The market should show limited volatility; it should stay between the upper and lower break-even points for a positive payoff. If the expectation of low volatility proves wrong, short straddle leads to massive losses (see Short Straddle).