The key to building a good mutual fund portfolio, one that can help you meet your goals, is getting the asset allocation right. "Asset allocation is to investment what oxygen is to human life," says Rohit Shah, a Sebi-registered investment adviser.

"It has been seen that 91% performance of the portfolio is linked to asset allocation. A person typically lives for 40-50 years after he starts earning. Over such a long period, we believe that one's ability to move in and out of the right assets is a key determinant of the return on investment," according to a paper, 'Determinants of Portfolio Performance II: An Update', written by Gary P Brinson, Brian D Singer and Gilbert L Beebower in Financial Analysts Journal, May-June 1991.

Ajit Menon, executive vice president, DSP BlackRock, agrees. "Right asset allocation is the best way to determine the right outcome. Close to 93% outcome is determined by asset allocation and not by the stocks or products that you choose."

Here's a guide on how you can get it right.

PART -1

Building a portfolio is an art as well as science. It's an art as the first step, the most treacherous one, is estimating the risk appetite.

"The investor should link investments to goals and map the schemes according to his risk profile," says Shah.

The second part starts with a question-how to go about building the portfolio? This, say experts, involves careful planning.

Menon of DSP BlackRock explains. "The risk profile has two parts - risk tolerance and risk capacity." The risk capacity, he says, may vary, as it is based on circumstances, while risk tolerance is a natural bent and doesn't change dramatically over a period.

For instance, he says, a person may love trekking but refuse to go on a difficult trek when it's raining. This doesn't mean he is not an adventurer. Therefore, risk tolerance is an inherent attitude towards risk. However, risk capacity is a different ball game. For instance, if you have small children, your risk-taking capacity is usually low. This is unlikely to change over a short period.

Typically, we all want best returns by taking the lowest possible risk. However, experts say that this is a wrong approach. The first step towards building a portfolio, they say, is being risk-aware instead of being riskaverse. "If we are seeking good long-term returns, our risk appetite needs to be congruent with the desired returns," says Puneet Chaddha, CEO, HSBC Global Asset Management.

To ensure correct risk assessment, it's advisable to take help from a financial advisor.

After knowing the risk profile, write an investment policy with goals and timelines. This should be periodically reviewed.

"It is a good practice to have everything documented as both the investor and the advisor must be clear on the expectations and deliverables," says Chaddha.

Sanjay Chawla, chief investment officer, Baroda Pioneer AMC, says, "Since risk profile and goals will change over time, it is important that the policy is updated at least once a year."

The main purpose of asset allocation is optimal diversification. Different assets do well over different periods. This means the only way to ensure portfolio stability is investing in different assets depending upon your goals, time horizon and risk appetite.

Even within asset classes, different sub-sets rise and fall differently. Take 2013. Large-cap funds returned 6% on an average whereas midand small-cap funds returned 3%. In the debt category, income funds returned 5% and the category liquid funds around 8.76%. However, technology funds returned a whopping 52%.

This is what active asset allocation seeks to address by adjusting exposure to different assets on the basis of their relative promise, giving the best possible outcome.

Asset allocation is also the key to wealth protection. This is supported by a study carried out by Karan Datta, National Sales Head at Axis Mutual Fund.

"If we take the three base assets that are available to investors easily by way of mutual funds-equities, bonds and gold-then in any single year two outperform and one underperforms. Timing this is difficult. Our study shows that an equally weighted portfolio in the last 15 years would have given negative returns in just one year and that year is not 2008 but mid-1990s."

PART - 3

Now comes the nitty-gritty of building a portfolio. There are various asset allocation models you can consider once you have established your basic policy. Although the advisor will customise the plan for you, there are three commonly used models - Strategic Asset Allocation, Dynamic Asset Allocation and Risk & Time Matrix Asset Allocation.

Strategic allocation:

In this, the composition of the portfolio depends upon your time horizon and risk appetite. You must stick with the plan till the goal is achieved. The idea is to maintain the balance. The allocation that has been decided, for instance 60% equity and 40% debt, should be rebalanced once a year. This requires less monitoring and management fee. The risk, too, is lower.

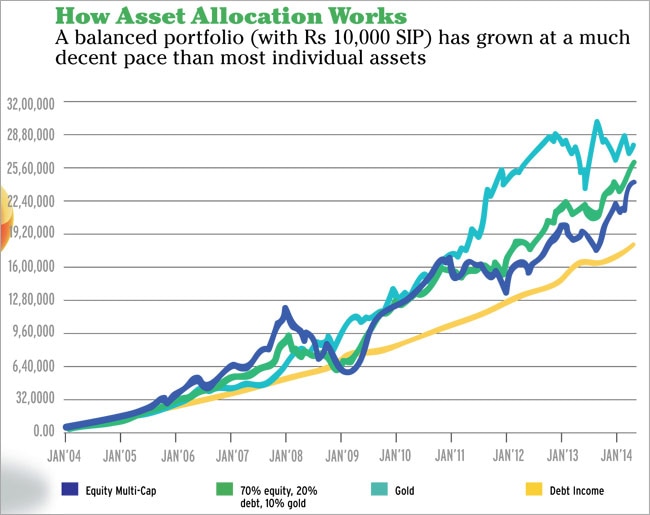

Let's take an example. Ram has been saving Rs 10,000 a month for his retirement, which is 25 years away, from 1 January 2004. His investment policy states that his risk-taking capacity is moderate and that for the next 15 years he will keep 70% funds in equity, 20% in income funds and 10% in gold. And, he will rebalance the portfolio on January 1 of each subsequent year.

Dynamic asset allocation:

It is based on market factors. The weights given to each asset are decided on the basis of the market situation. The funds are more actively managed. The costs are more due to the higher churn. The returns, too, are volatile, and success depends on getting many factors right most of the time. Biju Behanan, founder, Finwell India, says he does not recommend this strategy to investors as it is timeconsuming and leads to portfolio volatility. The portfolio is reviewed typically every quarter and rebalanced according to the market situation.

Risk & Time Matrix Asset Allocation:

One can look at aggressive, balanced or conservative asset allocation based on one's profile, goals and fund availability. Shah says that with passage of time one is likely to have fewer responsibilities and lower risk appetite. "If the critical goals are discharged, then one can choose to be more flexible. On the other hand, if the goals are coming to maturity, then one may have to start moving funds from say equity to debt," he says.

Myth 1:

The longer the time horizon the riskier products you need to choose. This is true, but time horizon is only one factor. The most important factor is the risk you are willing to take. This is based on behavioural factors, not just the time horizon. You may have a long time horizon but may be unwilling to take higher risk.

Myth 2:

Your age determines the asset allocation. While this could be true, personal factors also matter. For example, a retired high ranking official with well-settled children and other sources of income may want to invest a large portion of his pension income in equities for his grandchildren. Conventional wisdom does not allow this.

Myth 3:

Financial planners need to push/educate people to higher-risk products. Changing habits and perceptions is a longer and tougher process. "We tend to show our natural behaviour in volatile times," says Shah.