Equity markets are not for the faint-hearted. The boom that ran from 2004 to 2007, the slump that hit in 2008, the sharp recovery a year later, interspersed with numerous short periods of extreme volatility, suggest that people nearing retirement should stay away from stocks. However, beyond this madness is a fact that is as clear as the sun-equities have given the best returns among all assets over long periods. Keeping a few quality stocks in the portfolio even if you are nearing retirement may not be a bad idea.

A CASE FOR EQUITIESAn analysis of various assets shows that equities have given the best returns during periods of high inflation, albeit with higher volatility. Stocks have returned 19% a year, followed by bonds (8.8%) and fixed deposits (7.4%). Average inflation during the period was 6%.

Among all asset classes, stocks are the most volatile. As a result, investors find it difficult to negotiate equity markets. "A number of retail investors have not gained from equities' performance over the long term. They get drawn in after a good cycle and suffer when it turns," says Pankaj Murarka, senior fund manager, Equity, Axis MF.

Devang Mehta, head, Equity Advisory & Sales (Retail), Anand Rathi Financial Services, says volatility can work for you as well as against you. It can hit you badly if have to sell at a market trough to meet an expense that cannot wait. It can also erode your wealth if it makes you panic and sell when the market is down. However, for long-term investors, volatility can be an advantage, as it helps them buy at lows. That's why, says Mehta, systematic investment plans are the best way to invest in equities & equity-oriented funds.

HOW MUCH SHOULD YOU INVEST?

"As a thumb rule, it should be 100 minus your age. However, a lot depends upon personal goals, aspirations and risk appetite," says Mehta. Current and anticipated cash flow also play a part.

Nirmal Rewaria, senior vice president & business head, Edelweiss Financial Planning, says those who are retiring in 30 or more years should keep at least 50% funds in equities. This should come down over the years.

Anil Rego, CEO & founder, Right Horizons, recommends the following allocation assuming 55 as the retirement age and moderate risk profile

Building an equity portfolio intelligently throughout the working life is the key to amassing a big retirement fund, say wealth planners.

ARE EQUITIES THAT RISKY?Investors feel that stocks involve too much risk. But there is some risk attached to every investment product. It's just that it is more apparent in some and not so in others.

Take bank fixed deposits, the safest of them all. Abhishake Mathur, head of Investment Advisory Services, ICICI Securities, says fixed deposits may give regular income but will not beat inflation over the long term.

For instance, at retirement, it may appear that with a fund of Rs 1 crore and expenses of Rs 8 lakh per annum, it is best to put all the money in a deposit that pays 8% per annum.

"In reality, considering inflation and tax on the interest earned, this is not a good investment decision," he says. This is because inflation will keep lowering the purchasing power of your interest income, which will remain fixed for years on end.

That is why experts say that a person, even if he is nearing retirement, can invest 20% funds into equities for extra returns. However, factors such as risk profile, time horizon and standard of living must also be kept in mind while taking such decisions.

AVENUES FOR EQUITY INVESTINGApart from investing directly in stocks, one can look at diversified equity mutual fund schemes as well.

Rego says investments in equity mutual funds should be diversified across categories like large-cap, mid- and small-cap and balanced funds. While large-cap and bluechip funds are less risky than others, and so fit well into the retirement plan, one can also consider small investments in mid-cap and small-cap stocks and funds due to their potential to give higher returns, though by taking more risk.

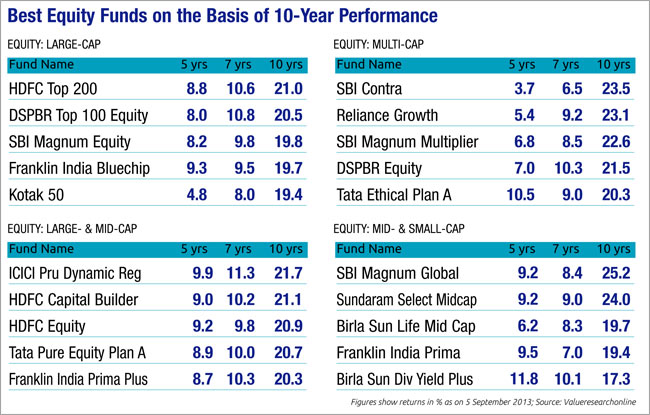

In fact, top equity funds have returned more than 20% a year for the last 10 years. HDFC Top 200, Franklin India Bluechip and DSPBR Top 100 Equity have returned 20% a year over the last 10 years and 8-10% in the last five years. The Sensex has risen 5% in the last five years. During this period, mid- and small-cap funds have also done stupendously well, giving returns in the range of 20-25%.

When it comes to stocks, typically, blue-chips are the best choice as they have an enviable record of giving consistent returns and dividends, while mid-cap stocks have the potential to rise sharply when markets are rallying.

If we take a look at the performance of the BSE Sensex vis-a-vis the BSE Mid Cap index, we can see that the mid-cap index catches up with the broader market and outperforms during rallies. However, in falling markets, it underperforms.

Further, during this period, top large-cap stocks have returned in excess of 20% a year, while top mid-cap stocks have returned more than 40%.

"While buying mid-caps, select those in safer sectors such as pharmaceutical, automobile and fast moving consumer goods (FMCG) which have a good record," says Mehta of Anand Rathi. These sectors fall the least during bad times and are ideal for a postretirement portfolio.

"The portfolio should also have a mix of banks and non-banking financial companies as well as automobile and capital goods companies which are available at attractive valuations and offer more upside when growth and capital expenditure cycle pick up," says Mehta. Those willing to take some additional risk can go for mid-cap companies in the above-mentioned sectors.

P Phani Sekhar, fund manager, Portfolio Management Service, Angel Broking, recommends funds benchmarked to indices, that is, index funds. Indices factor in the survivorship bias, which ensures that only the best companies are included. This also makes sure that returns do not depend upon the ability of the fund manager.

Economic and business cycles generally last for five-seven years. Hence, investors should not stick with a strategy beyond this period, says Sekhar. Those willing to take additional risk can use 25% of their funds marked for equities to build a portfolio that tracks mid-cap indices. Picking clear winners is not easy, and that's why tracking the index can work, says Sekhar.

But which way is the market cycle headed at this stage? Stock market returns have been very low or negligible for the past five-six years. During this period, gold & real estate have performed much better than stocks.

"Going forward, we feel that equities can now start to outperform over the next 5-10 years. India is slated to be back on the growth path," says Mehta. He says expectation of 15-17% a year stock market returns from here on is not unreasonable, provided one's horizon is 10-15 years.

MONITOR YOUR PORTFOLIO

Building a portfolio is easy. But the real challenge, especially in later years of the life, is to keep it growing. This, say financial planners, requires continuous monitoring and nimble-footedness.

"Ideally, one needs to look at the portfolio at regular intervals, may be once in three-six months or a year," says Mehta of Anand Rathi. One must also remain in touch with one's advisor for any changes required in the portfolio. A portfolio needs to be shuffled whenever a stock or sector reaches unsustainable valuations or there is extreme optimism/pessimism.

**TIPS FOR SUCCESSFUL INVESTING**

>> BE PREPARED FOR VOLATILITY - Ups and downs are an inherent feature of equity markets. A fall just after you have made an investment does not make the decision wrong. It's best to remain disciplined and not get swayed by market sentiment.

>> RISK Vs RETURNS - According to Murarka of Axis MF, investors should not get swayed by the short-term performance of equity funds and instead look at risks that the fund managers are taking. They must also check whether the performance is sustainable. Also, investors should evaluate fund managers on the basis of the performance of all the funds that they manage and not just the best ones.

>> DON'T CHASE WINNERS, CHASE CONSISTENCY: An analysis has shown that schemes get much higher inflows following a period of outperformance as compared to redemptions following underperformance. This may put pressure on fund houses to focus on the short term. "The analysis further shows that close to 50% top performing funds in any year tend to see a fall in performance in the subsequent year," says Murarka.

>> PICK WELL-ROUNDED STOCKS: If you intend to build a stock portfolio, you should keep in mind factors such as the company's corporate governance standards, return on equity, business model and competitive advantages. This means the company should have a unique product or service