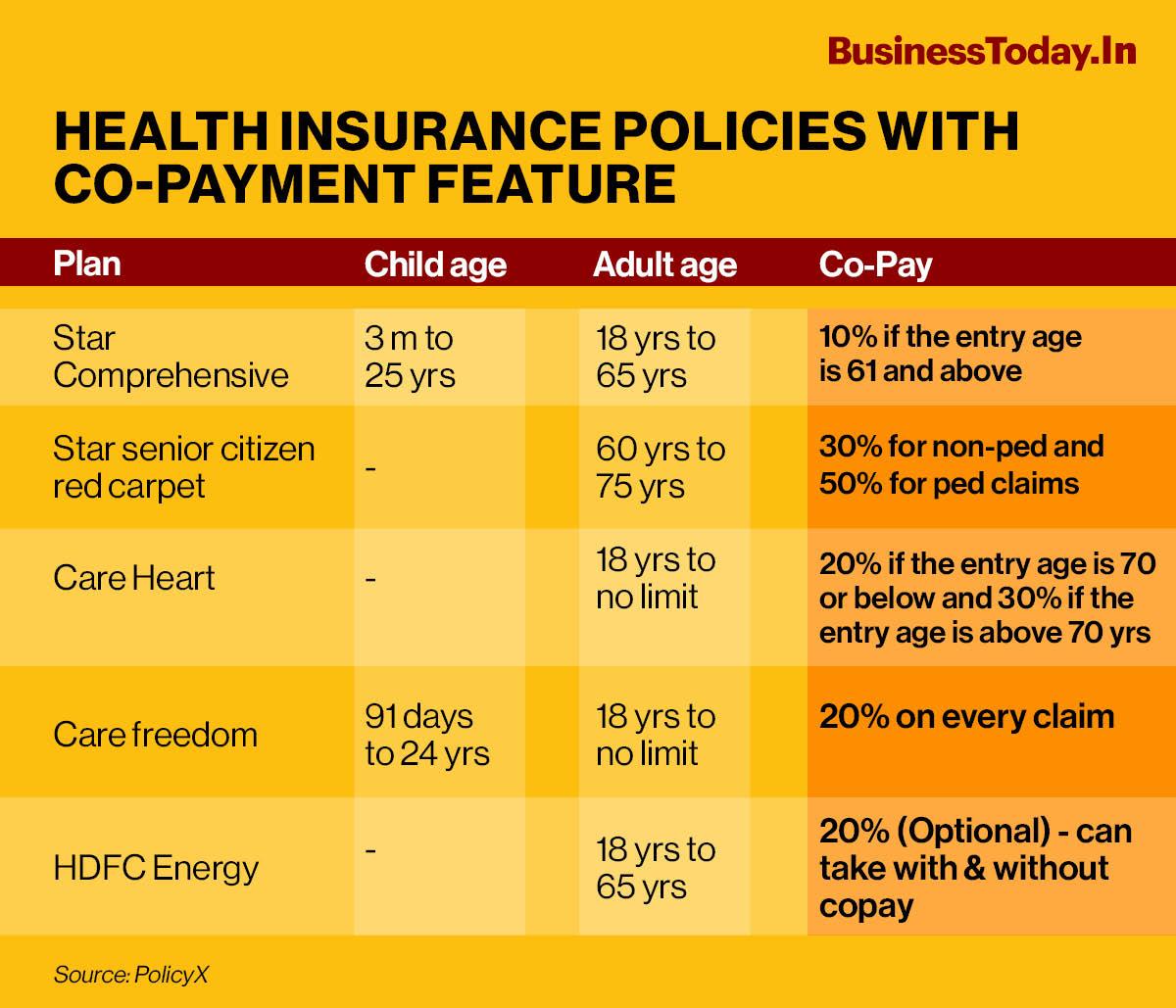

Since the insured has to foot the percentage of the hospital bill, premium rates tend to be lower for health insurance policies with co-payment featureSince the insured has to foot the percentage of the hospital bill, premium rates tend to be lower for health insurance policies with co-payment feature

Since the insured has to foot the percentage of the hospital bill, premium rates tend to be lower for health insurance policies with co-payment featureSince the insured has to foot the percentage of the hospital bill, premium rates tend to be lower for health insurance policies with co-payment featureNanda Kishore, 50, was in for a surprise when he was asked to pay 20 per cent of the hospital bill for his mother’s illness. Covered by an insurance policy he thought everything would be taken care of by the insurance company. “I was not prepared to pay the amount as I thought our health insurance policy would take care of the bill. I later came to know that the policy had the co-payment feature which we overlooked at the time of buying the policy.”

There are many like Nanda who agree to pay less premium in lieu of the co-payment feature without understanding its implications. Co-payment is a contract where you agree to pay for some percentage of medical expense from your own pocket and share the burden of the medical expense. For example, if your hospital bill comes for Rs 1 lakh then your health insurance policy will cover only Rs 80,000 the rest has to be paid from your pocket.

Should you opt for co-payment?

Ideally one should not opt for co-payment feature. But if paying premium is difficult then co-payment is a better option than not buying a cover at all. Moreover, co-payment can be suitable for senior citizens, as premium rates are higher during old-age.

“Co-payment is a good way to regulate the premium cost. While co-payment helps in reducing the premium prices and ensures affordability but in exchange for this, the policyholder has to pay exorbitant hospital expenses from their own savings. Thus, co-payment either should be avoided or kept limited to bear least hospital expenses,” says Naval Goel, founder and CEO, PolicyX.com.

He adds, “The policyholder can choose co-pay by weighing his/her health and financial situation as it is today and is expected to be during the health policy. If they can afford it, paying a higher premium now can save the policyholder in the long run.”

Impact on premium

Since the insured has to foot the percentage of the hospital bill, premium rates tend to be lower for health insurance policies with co-payment feature. The percentage depends on the percentage of co-payment one has opted for. “The copayment generally makes a difference of 20-25 percent in the premium rates varying according to the plan and age of the policyholder,” says Goel.

Co-payment should not be considered with a view to lower your premium rates. However, if paying premium is difficult than going for a copayment feature is better than not having a health insurance policy.

Also read: Guaranteed insurance plans emerge as preferred choice among policyholders

Also read: LIC introduces new savings life insurance plan; check out details

for that fiscal year.") Union Budget 2026: Just 0.08% of companies earned two-thirds of India Inc's profits before tax

Union Budget 2026: Just 0.08% of companies earned two-thirds of India Inc's profits before tax Joint statement on India-US trade deal in 2-3 days; $500 bn imports lined up over 5 years: Sources

Joint statement on India-US trade deal in 2-3 days; $500 bn imports lined up over 5 years: Sources Budget 2026 maintained continuity and consistency, says DEA Secretary

Budget 2026 maintained continuity and consistency, says DEA Secretary Rice exporters cheer as US cuts tariffs to 18%, boosting India’s export competitiveness

Rice exporters cheer as US cuts tariffs to 18%, boosting India’s export competitiveness 'Left, right switches checked, found satisfactory': DGCA rejects fuel switch malfunction claims on Air India Boeing 787

'Left, right switches checked, found satisfactory': DGCA rejects fuel switch malfunction claims on Air India Boeing 787 India–US Trade Deal Ignites Record Rally, Markets Add ₹20 Lakh Crore

India–US Trade Deal Ignites Record Rally, Markets Add ₹20 Lakh Crore 21-Year Tax Holiday Clears The Path For India’s GCC Boom, Where's The Big Opportunities?

21-Year Tax Holiday Clears The Path For India’s GCC Boom, Where's The Big Opportunities? India–US Trade Deal Sparks Massive Market Rally | Amit Goel Explains

India–US Trade Deal Sparks Massive Market Rally | Amit Goel Explains India–US Trade Deal After Tariff War: Trump Slashes Tariffs, Modi Welcomes Trade Reset

India–US Trade Deal After Tariff War: Trump Slashes Tariffs, Modi Welcomes Trade Reset India-US Deal: Not A Blanket Cut, But A Big Boost | Fine Print Matters

India-US Deal: Not A Blanket Cut, But A Big Boost | Fine Print Matters Bajaj Housing shares up 2% after Q3 results: What lies ahead for investors?

Bajaj Housing shares up 2% after Q3 results: What lies ahead for investors? IREDA shares climb 2%, snapping 4-session fall; trend still cautious or reversal sign?

IREDA shares climb 2%, snapping 4-session fall; trend still cautious or reversal sign? Sensex, Nifty roar back with 2.5% surge as India-US trade deal brightens outlook for markets, rupee

Sensex, Nifty roar back with 2.5% surge as India-US trade deal brightens outlook for markets, rupee Solar Industries Q3 earnings: Defence firm logs highest revenue, EBITDA; stock ends higher

Solar Industries Q3 earnings: Defence firm logs highest revenue, EBITDA; stock ends higher  Adani Enterprises Q3 earnings: Net profit surges 97 times; stock zooms 12%

Adani Enterprises Q3 earnings: Net profit surges 97 times; stock zooms 12%