The card data stored in e-commerce sites will also be disabled

The card data stored in e-commerce sites will also be disabled The card data stored in e-commerce sites will also be disabled

The card data stored in e-commerce sites will also be disabledThere is good news for credit card and debit card customers who make recurring and one-click payments via debit card and credit card on merchant sites for buying consumer durables, groceries, and paying subscriptions for OTT and other services.

ISSUE & HISTORY

The RBI has banned the storage of customers' credit card and debit card details by the payment aggregators, and online merchants from January 01, 2022. The deadline was extended from July to December 2021 and there is no further relaxation.

IMPACT ON CONSUMERS

There will be transaction declines on recurring payments where people have taken annual subscriptions. The card data stored in e-commerce sites will also be disabled.

The customers will be asked to fill in their 16-digit card number, card expiry date, and also the CVV, which is a card verification value every time they do an online transaction.

No more one-click faster checkouts from merchant sites.

REASONS FOR RBI'S BAN

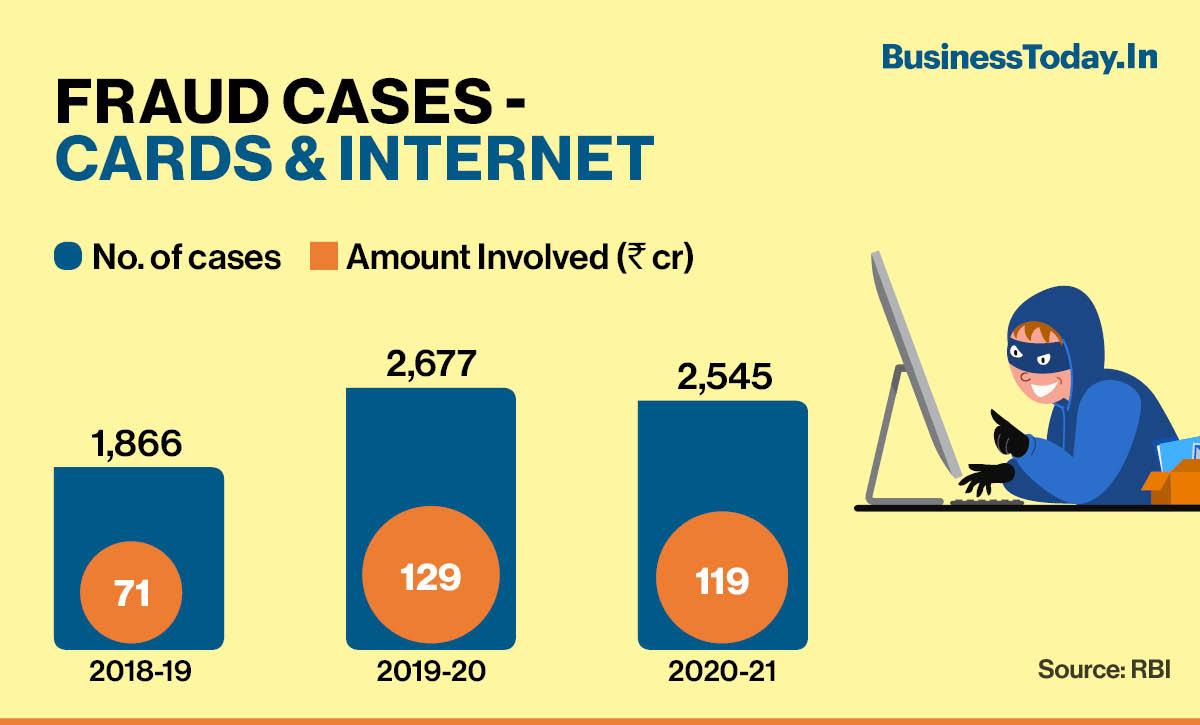

The merchants, payments aggregators, and even payment gateway players, who get to store the card data, are not registered with the RBI. The objective of the RBI's diktat is to create a better security framework for digital transactions, which have accelerated post the pandemic.

There are frequent data breaches reported in payments companies exposing customers' financial and personal details. The possibilities range from theft and hacking to misuse of the data.

SOLUTION / ROAD MAP

The industry was long demanding solutions like tokenisation, which actually means hiding the card details and replacing them with one-time tokens or codes. Under tokenisation, the card details are stored only with the card network like Visa and Mastercard and card issuing entities, which could be a bank or an NBFC.

Tokenisation was earlier restricted to only a handful of devices like mobile phones, laptops, and tablets. The RBI has now taken two sets of measures for helping customers in faster checkouts at merchant outlets.

A month ago, the RBI extended the tokenisation to newer modes like wearable devices like wristwatches and bands. But this was not enough as tokenisation is linked to a single device of the customer and hence he could pay only from that particular device. Customers, however, use multiple devices. So a payment from a mobile device for OTT cannot be done from, say, a tablet or vice-a-versa.

RBI has now allowed 'tokenisation on file' which allows the data to flow in a file. This will not link the device to the payment; instead the data will flow on a tokenised file.

Apart from card networks, the card issuers like banks and NBFCs are also allowed to issue tokenised files.

CHALLENGES FOR PAYMENT PLAYERS

All the participants in the chain from the card network, issuer, payment aggregators, and merchants have to be ready with the technology to accept tokenised files. This will certainly require some investments.

There are many smaller players in the chain, especially payments aggregators and merchants, who will need time to tie up with the card network to seamlessly receive the tokenised files.

The banks as card issuers will also have to be ready with technology infrastructure for tokenised ecosystem.

Also read: RBI expands 'tokenisation' facility to CoFT services after device-based framework

Goldman Sachs: STT, fears of Monday FPI selling drive worst Budget-day selloff in 6 years

Goldman Sachs: STT, fears of Monday FPI selling drive worst Budget-day selloff in 6 years Budget 2026: Income Tax Act from April 1, higher FPI limits, STT hike headline FM's reform express

Budget 2026: Income Tax Act from April 1, higher FPI limits, STT hike headline FM's reform express Union Budget 2026: ‘When I was in defence, bulletproof jackets were not available for soldiers,’ says FM Sitharaman

Union Budget 2026: ‘When I was in defence, bulletproof jackets were not available for soldiers,’ says FM Sitharaman February to be hotter, drier this year, says IMD; winter crops may be affected

February to be hotter, drier this year, says IMD; winter crops may be affected  Top stocks in news: Adani stocks, BSE, Hero Moto, Groww, Mphasis, IDBI Bank, MOIL, Hyundai

Top stocks in news: Adani stocks, BSE, Hero Moto, Groww, Mphasis, IDBI Bank, MOIL, Hyundai Golf’s Powerful Role As A Stress Buster

Golf’s Powerful Role As A Stress Buster Union Budget 2026 | EXCLUSIVE Ashwini Vaishnaw On Budget 2026 And India’s Growth Roadmap

Union Budget 2026 | EXCLUSIVE Ashwini Vaishnaw On Budget 2026 And India’s Growth Roadmap Union Budget 2026 | Exclusive: Anuradha Thakur, Secretary, DEA & DFS Secy M. Nagaraju On Union Budget 2026–27

Union Budget 2026 | Exclusive: Anuradha Thakur, Secretary, DEA & DFS Secy M. Nagaraju On Union Budget 2026–27 Union Budget 2026 | STT Hike Sparks Selloff As Sensex, Nifty Plunge Nearly 2% After Budget 2026 Announcement

Union Budget 2026 | STT Hike Sparks Selloff As Sensex, Nifty Plunge Nearly 2% After Budget 2026 Announcement Union Budget 2026 | “This Is A Youth Power Budget,” Says PM Narendra Modi On Jobs, MSMEs And Infrastructure Push

Union Budget 2026 | “This Is A Youth Power Budget,” Says PM Narendra Modi On Jobs, MSMEs And Infrastructure Push ITC shares at 52-week low post 15% YTD correction; what's next?

ITC shares at 52-week low post 15% YTD correction; what's next? Bharat Electronics, NTPC, Ramco Cements: How to trade these 3 buzzing stocksGoldman Sachs: STT, fears of Monday FPI selling drive worst Budget-day selloff in 6 years

Bharat Electronics, NTPC, Ramco Cements: How to trade these 3 buzzing stocksGoldman Sachs: STT, fears of Monday FPI selling drive worst Budget-day selloff in 6 years Stock market today: Gift Nifty up 10 points; key levels for Nifty, Sensex & Nifty BankTop stocks in news: Adani stocks, BSE, Hero Moto, Groww, Mphasis, IDBI Bank, MOIL, Hyundai

Stock market today: Gift Nifty up 10 points; key levels for Nifty, Sensex & Nifty BankTop stocks in news: Adani stocks, BSE, Hero Moto, Groww, Mphasis, IDBI Bank, MOIL, Hyundai