Some two years ago, an affiliate of KPMG in India detected foul play in the books of Mumbai-based Fourcee Infrastructure, a logistics provider for specialty chemicals. The auditor subsequently raised an alarm for accounts irregularities.

Such issues are generally swept under the carpet in most small-sized closely held companies, but private equity (PE) companies are indubitably more transparent. General Atlantic, Fourcee's 36.5 per cent PE partner, escalated the matter by appointing another independent auditing firm, EY (erstwhile Ernst & Young), to further investigate the matter. The promoter duo, Rajesh Lihala and Vinay Singh, agreed half-heartedly - together they hold a majority stake. EY stumbled upon more instances of wrongdoing, including inflated revenues and profits and forged bank statements.

Indeed, Fourcee is an example of bad investments that PE companies are increasingly getting stuck with in India. General Atlantic was not new to the game. It was an early investor in Patni Computer, among its biggest investments in Asia, way back in 2002, and picked up a stake in Fourcee only in 2012. There are PE companies who have invoked "arbitration clauses" in Singapore and London courts to put pressure on promoters to honour contractual or commercial agreements.

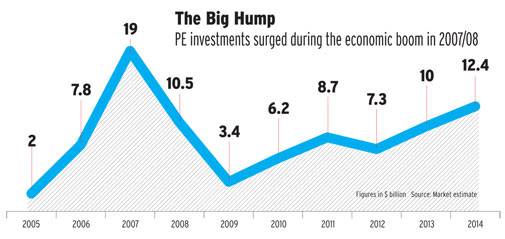

The problems of PE firms have their genesis in the high octane growth period of 2005 to 2008 for corporate India. PE players are widely believed to have been carried away and invested in companies at generous valuations. "PEs went in with their eyes closed. They did not think through exits properly," says a veteran private equity player who has now started a fund of his own.

Many PE players had little understanding of India's family-owned companies. They were also not well informed about governance issues related to the country's small and medium enterprises. These players - flush with cheap funds - poured big money into real estate, infrastructure, capital goods & engineering and consumer durables companies. "In several cases, the mismatch of demand for investment grade assets and the available supply of capital led to inflated valuations," observes a recent McKinsey report on the PE industry.

The PE industry poured $40 billion in mid-sized growth companies in the boom period of 2004 to 2008. It is time to exit for these funds but many of them are struggling to cash out. Ideally, General Atlantic should have exited Fourcee this year after a five-year holding period.

Meanwhile in India, the PE industry is also grappling with another problem. It is taking a haircut as the rupee has depreciated against the US dollar over the past five years by around 40 per cent.

Notwithstanding the challenging environment and the financial stress in mid-sized companies, the PE industry doesn't have much influence on investee companies. Almost 90 per cent of the deals are for a minority stake with the promoters managing the affairs of the company. "This has restricted their influence. They are called upon for advice when needed, but have limited scope for direct intervention," explains the McKinsey report.

The PE players, or general partners (GPs), are actually custodians of money advanced by limited partners (LPs) - high net worth individuals, pension funds and institutions. PE funds have to return the money of these LPs after a few years along with substantial returns (usually 20 per cent per annum). While the industry has now lowered its return expectations in India, how will they explain poor performance to an LP? "At best, these PEs can extend the period of the fund for a few more years," says Anish Jhaveri, founder of Olphans Capital, a provider of seed capital.

How It Works

Typically, a PE firm invests in a portfolio company with a four-to-five year time horizon. During this period, the investor brings additional capital, helps in driving operational efficiencies, and lends its expertise in technology and markets to give a fillip to revenues and profitability.

A PE investor looks to exit at the peak of the company's financial performance after making super normal returns. In the pre-2008 period, the average holding period was just three years. "But the longer you hold on to an asset, the more difficult it becomes to get out because the operating leverage goes away," says Vivek Pandit, Director at McKinsey & Company.

Historically, the most favoured route for a PE exit is an initial public offering (IPO). This is largely because shares often get the best valuation in an IPO. The US-based PE firm Warburg Pincus, one of the early entrants in India, has made a fortune (3.5x to 6.2x) post listing in some of the blue-chip Indian companies, including Bharti Airtel, Kotak Mahindra Bank, Alliance Tire, Sintex and Max India. In the past, one-third of the exits has happened through the IPO route. In the current year, Aditya Birla PE and SAIF Partners have made good returns in fruit drink maker Manpasand's IPO. Similarly, Sequoia Capital and Tiger Global made profitable exits in Just Dial's public offering in 2013.

But not all investors are lucky. There are over 2,000 PE-backed companies waiting to launch their IPOs. "So far, the investors are cheering only select sectors like FMCG or unique business models like Just Dial. The rest have to show inspiring financials to get value through an IPO," says an investment banker on condition of anonymity.

SEBI is flooded with draft prospectuses. At last count, experts estimate over Rs 1,00,000 crore worth IPOs are in the pipeline, but only a handful of companies has raised funds. Clearly, promoters are not happy with the valuations being offered in the primary market. Blackstone was almost ready to exit from Emcure Pharmaceuticals some two years ago, but the IPO had to be withdrawn because of poor response. This US-based PE company later managed to sell its stake to another fund, KKR, without making much money. Mauritius-based New Silk Route (NSR) managed to sell its stake in Ortel Communication through an IPO but the stock price plunged after listing. "Small investors are getting stuck with a lemon," says a market observer. Adlabs Entertainment, in another instance, saw its offer price changing twice - from Rs 221-230 per share to a much lower band of Rs 185-215 per share. Ortel's share price recovered after close to four months of listing, and is currently trading at Rs 205 per share. Experts blame the investment banking community for setting unreasonable price bands in an IPO. "In nine out of 10 cases, the i-bankers in their enthusiasm go out and build very optimistic scenarios, which is not the case on the ground," says a market observer.

PE firms also don't have the luxury to exit completely in an IPO. "It's not considered good by the market as money doesn't come to the company. The IPO has to be a combination of fresh equity and offer for sale," says Mayank Rastogi, Partner (PE Transaction Services) at EY. Institutional as well as retail investors look for growth prospects in a company launching its IPO. And that will happen when new money comes into the company.

Dialling Another PE

PE-to-PE secondary sale has never been a popular exit route in the past. Prior to 2008, one-tenth of the deals took place through this route. Surprisingly, this route is now getting crowded, accounting for one-third of the exits in the last five years. (See Changing Exit Strategy.)

"The distress in many of the investee companies is because of the cyclical nature of the industries and the slowdown in the overall activity in the economy," says an executive of a PE firm. "This route offers a good investment opportunity for a new player as the valuation expectations of an existing PE player is also low." In June this year, KKR bought Warburg Pincus's stake in pathology chain Metropolis. Similarly, Everstone is in talks with Advent for buying its stake in Care Hospital.

Sceptics, however, say secondary sales won't be able to absorb the $40 billion stuck in many of the struggling sectors such as real estate and infrastructure. Indeed, almost 30 per cent of the funds are locked in real estate.

As a fall-back option, PEs have a compulsory buy-back clause with promoters - it allows them to sell their stake to promoters. In the pre-2008 years, buy-back was non-existent as IPO, strategic sale and PE-to-PE emerged as the dominant exit routes. In the current challenging environment, the PE industry is making last ditch attempts to exit investee companies. Today, one-fifth of the exits in India is taking place through the buy-back route. In June, Baring Private Equity invoked the buy-back clause in cement major Lafarge India - this move came after the global merger of Holcim and Lafarge. Baring, which bought 14 per cent stake for e200 million, sold the stake for e270million.

According to experts, promoter buy-back is a very contentious issue. It often leads to "valuation" differences between the promoter and the PE player. The buy-back price is based on the internal rate of return (IRR, normally over 20 per cent per annum) promised at the time of entry. The fair value price or the company valuation should factor in the IRR. "We also have to understand that an investee company's assets are the only assets of an Indian promoter which he or she holds by way of shareholding in the company," defends Nishant Parikh of Trilegal.

Legal luminaries contend that a fair value is ultimately an opinion. "There is a good deal of subjectivity in arriving at fair valuation," believes Parikh of Trilegal. The UK-based PE 3i Investment, for instance, is embroiled in a legal battle with promoter CVR Group of Krishnapatnam Port over the buy-back agreement. "In India, you cannot alienate a promoter. You have to sit with the promoters," says a PE player. In the West, the rights of PE firms are well protected by the judicial system, which is fast and efficient. "In India, even a cheque bouncing case can take a couple of years to resolve," says Jhaveri.

Strategic Sale

The promoter-driven or family-owned characteristics of the Indian industry also come in the way of strategic transactions, which are built in the agreements. The promoters generally have a first right of refusal. In April, the UK-based Apax Partners sold its 28.91 per cent stake in IT major iGate to Capgemini, which is a leading consulting and outsourcing company. Recently, Malaysia-based Parkway Hospital acquired 74 per cent stake from Everstone Capital and Anand Rathi Capital Advisor in Hyderabad-based Global Hospitals. PE players are now predicting that the next transaction in Alliance Tire will be a strategic transaction. In April 2013, KKR bought 90 per cent stake in global tire maker from Warburg Pincus, another PE. Pankaj Kalra, Senior Executive Director at Kotak Investment Banking, says that the challenge tends to be the valuation. "Valuations are not cheap in India," says Kalra.

An executive with a PE player narrates an incident where his firm had to threaten the promoter of a real estate company with a strategic sale to force him to buy-back at a higher price than initially offered. The price offered by a competitor was almost double the price quoted by the promoter. "The developer finally relented to buy back at the new discovered price," says the executive.

But there are also agreements where a PE can sell out only to a financial investor and not to a strategic investor. There are many deals where promoters have stated that a PE can only sell to a third party with prior approval of the promoter family. "PEs have given away their rights without realising what they are getting into," says a domestic PE player.

The Pipe Deals

The Way Forward

Some are predicting a shakeout in the PE space. "There are PE investors who are scouting for buying out entire portfolios," says Kalra of Kotak Investment Banking. Experts see this happening as there could be a possibility of an LP forcing a complete exit of portfolio where the fund is small with no visibility of exit in the near future. There is already one deal where JP Morgan acquired the entire portfolio of Canaan Partners in April this year. Globally, complete buy out of funds is very common.

A consultant on condition of anonymity shares that there are lot of strategic direction initiatives, including performance matrix and sales maximisation. "They are hedging or guarding their downside. This is not a true blue PE attitude," says Deep Mukherjee, Director, India Ratings.

Some $100 billion PE money in the last one and a half decade has found its way into Indian companies. It has provided a new source of financing Indian entrepreneurs. Warburg has taken early bets in the telecommunication space which has changed the industry landscape. Similarly, IT, pharma and health-care sectors have received ample PE funding. "Out of the $8-10 billion that came in the last one year, a disproportionate amount has gone in the technology and Internet space," says Kalra of Kotak. In fact, billions of dollars are expected to pour into new technology driven start-ups.

But General Atlantic's experience with Fourcee is a stark reminder of the need for PE companies to temper exuberance with realism. It is important to exercise prudence while investing to avoid getting singed.