One of the sectors worst affected by the economic slump of the last few years has been infrastructure . Star companies of the 2000s - the GMR Group, the GVK Group, or Lanco Infratech - have been reeling under debt and struggling with delayed projects. This, however, is not the whole story. Many lesser-known infrastructure companies have prospered despite the adverse circumstances.

A common feature of most of these resilient companies has been their business model. Different from the asset-owning developer model of the likes of GMR, GVK and Lanco, these are construction companies. They have largely stuck to the traditional EPC (engineering, procurement and construction) format, in which the client is billed and pays for the costs incurred for the project, rather than the BOT (build, operate and transfer) one, where the company raises its own funds and recoups them after completion by imposing a toll on users or getting an annuity from the client. Until the downturn struck, the BOT route was all the rage for mega-projects, with government departments rooting for it and many companies responding enthusiastically. But all that has changed. "In today's environment, EPC is a better model because capital is not easily available for companies," says Shirish Rane, Head of Research at IDFC Securities, who has tracked the sector for years. "In future, most projects will come on EPC basis and that will be good for EPC players."

Apart from the choice of model, sharp focus on the segments and geographies they are most familiar with, as well as a tight rein on costs, has helped these companies. "Chances of growth are greater for those companies which have good execution skills, are able to manage their cash flows well and have minimised their exposure to BOT," says A.A.V. Ranga Raju, MD of NCC (formerly Nagarjuna Construction Co.), which has largely focused on EPC. NCC is now concentrating on cash contracts, but wants to monetise its assets and reduce its Rs 2,200-crore debt. "If there is, say, a one year delay in completing an EPC contract, project costs go up by five to six per cent, but if there is a similar delay in a BOT project, they rise 20 to 25 per cent."

BT profiles six companies - Transstroy (India), Sadbhav Engineering, IRB Infrastructure Developers, MBL Infrastructures, PNC Infratech, and J. Kumar Infraprojects - which have beaten the overall trend.

Transstroy (India): Dam Politics

Along with the futuristic international airport, built by the GMR Group, the eight-lane Outer Ring Road is one of Hyderabad's infrastructural marvels. A 22-km stretch of the road, en route to the airport from the city's IT hub at Gachibowli, was built by Transstroy (India), which gets its tongue twisting name from its Russian joint venture technical partner. In Russian, Transstroy simply means "transport construction". Its CMD and CEO Sridhar Cherukuri is related to Rayapati Sambasiva Rao, formerly with the Congress and now a Telugu Desam MP, but insists the political connection has nothing to do with his success. "This is a company run on professional lines by professionals," he says. He readily admits Rao's wife has a 24 per cent stake in the company, but points out that he and his immediate family own 74 per cent.

Started in 2001, Transstroy too prefers the EPC mode, though it has taken up BOT ones - and variations of BOT to include design and finance - as well. "Though we have BOT projects, our focus since 2013 has been only on direct EPC ones," says N. Kalyana Sundar, Vice President, Accounts and Corporate Affairs. With revenues of Rs 4,538.1 crore in 2013/14, it built its reputation and strength through road building, but in the last two years has diversified considerably. "Till 2013, roads brought in about 80 per cent of our revenues," says Sundar. "Now it is down to about 50 per cent. But roads have been the key growth drivers for the company." Of the remaining 50 per cent, 45 per cent comes from irrigation and the remaining from power and port infrastructure. About 35 per cent of its projects are in Andhra Pradesh and around 30 per cent each in Tamil Nadu and Madhya Pradesh.

With a Rs 21,000-crore order book, Cherukuri is optimistic. "We will be growing at 10 to 15 per cent every year for the next five years." But he will have to take care of one major problem, like many other infrastructure companies. Transstroy today has a Rs 4,000-crore debt, according to Cherukuri. He is likely to sell some of his road assets - 13, of which four are generating revenue - to bring the debt equity ratio down to 3:1 by 2016/17. Even for Polavaram, half the land needed for the project has yet to be handed over to the company.

Sadbhav Engineering: Ruling the Road

Patel is confident that roads, in particular, will continue to provide good business. "In the current financial year, we have added Rs 2,600 crore worth of new business, and by the time it ends, we hope to get another Rs 5,000 crore to Rs 6,000 crore worth of business in roads alone." To grow competency and strength, in its core sector, he says, as against one tendering department that the company had four to five years ago which looked at all road, irrigation and mining contracts, each tendering department has now been separated. This too will help to improve margins.

Vishnubhai M. Patel, CMD of Sadbhav Engineering, attributes another reason for the company's success. "We have not lost sight of the need to take care of the interests of our employees," he sums up.

IRB Infrastructure Developers: Building on BOT

It is also careful about which states it invests in. "We are very clear that we will only take up projects in states where there is no law and order problem and there are bright prospects for economic development," Mhaiskar adds. IRB has built, for instance, the entire Ahmedabad-Pune corridor of about 650 km, barring the Vadodara to Bharuch stretch (which was done by L&T). "Collecting toll on this high traffic corridor has been a key driver of growth for us," he adds. "We consolidated in this belt between 2004 and 2011 and it has been doing quite well."

Doubts, however, have arisen over the company's return on equity (ROE), down from 19 per cent in 2009/10 to around 13 per cent in 2013/14. "That is because the government has changed the duration of concessional agreements," says Mhaiskar. "Earlier these were for 15 years, but since 2009, they are usually between 25 and 30 years. The longer tenure concession means a longer gestation period, which brings the ROE down."

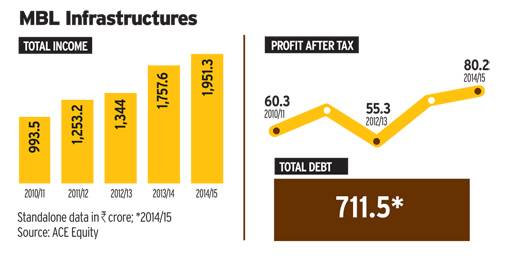

MBL Infrastructures: Prudence the Watchword

Some EPC players were also affected by the mood. "People started quoting lower and lower and got trapped in a vicious cycle," says Lakhotia. How did MBL avoid the pitfall? "We kept ourselves away from all this, focusing on execution in keeping with our fundamentals," he adds. "There were times when, for three or four quarters, we did not have any fresh orders. Some of my rivals said MBL was going down as we were not getting any fresh fare. But I told them I was happy with what we were eating. The strategy has worked for us."

MBL is involved in some BOT projects, but mostly as an EPC player in the special purpose vehicles (SPVs) set up to implement them. Here too Lakhotia is choosy. "We go for clients such as National Highway Authority of India (NHAI), Delhi Metro Rail Corporation (DMRC), Steel Authority of India (SAIL) and projects in states which have World Bank or Asian Development Bank backing. There is a professional environment here and funds are never a problem."

Hailing from Lakshmangarh in Rajasthan's Sikar district, Lakhotia admits he has a soft spot for the state. Even so, he does not let sentiment overwhelm him. He was keen to take up the 50-km Sikar to Reengus highway contract, but ultimately held his hand. "I was emotional about it and would have even done it on a no-profit, no-loss basis," he says. "But the bidding was aggressive and irrational, so I decided not to participate." He did, however, bag the over Rs 500 crore project for developing and operating Bikaner to Suratgarh section of NH-15 in Rajasthan, one of the few BOT projects he has taken up. "What drew me was the kind of traffic this stretch will attract," he says. "There is a national highway and several roads leading to Bikaner from different cities of Rajasthan, but they all terminate at Bikaner. Similarly, there are roads from Suratgarh to both Punjab and Delhi. But there is no other good road between these two points."

Lakhotia is optimistic about the future, as the government has no choice but to keep improving infrastructure. "We expect a compound annual growth rate of 25 per cent for the next five years."

PNC Infratech: Rigorous Due Diligence

The company's focus area is clear - North India in general and Uttar Pradesh in particular. "We have worked in 13 states, but around 60 per cent of our total revenue comes from UP and about 90 per cent from the North," says Yogesh Kumar Jain. Working in and around UP helps since PNC has 11 stone crushers of its own in the state, which cut down its cost of transporting construction material. The brothers have taken up a few BOT projects, but never those in which premium has to be paid to the client (usually a government department). Instead, they make sure the government too puts in some money. Isn't it bothersome dealing with bureaucratic government departments? "That is our strength," says Yogesh Kumar Jain. "It is a skill the company has honed and perfected."

As of end-August, PNC had an order book of about Rs 4,000 crore, but the unmoving top line has been bothering the brothers. "We decided not to depend too much on NHAI projects, which are becoming very competitive," says Yogesh Kumar Jain. "We've been diversifying into fully-funded state government projects in UP, Delhi and Madhya Pradesh. In our order book, projects of these three states make up about 40 per cent." In the last five years, CAGR has been 15 to 20 per cent, which he hopes will rise to 20 to 25 per cent in the next five. "We are currently among the top 20 infrastructure companies in the country. Our goal is to figure among the top 10."

J Kumar Infraprojects: Self Reliant

Currently, around 34 per cent of the company's business is in roads and highways, 25 per cent in flyovers, 27 per cent in metro rail projects and the rest in miscellaneous civil works. But the metro segment, both elevated and underground, is rapidly becoming its main focus. The company's main focus now is metro rail systems, both elevated and underground. "Every smart city will have a metro," Gupta adds. "In the next two years, Maharashtra alone will be awarding around Rs 1 lakh crore worth of projects. Many will involve metro rails."