The budget speech by Finance Minister Arun Jaitley lasted nearly two hours. By the time it was over, the hopes of millions were dashed. The tax exemption limit was not revised, and there was no rise in the deduction limit under section 80C. The middle class had very little to cheer about. On the top of it, the cost of mobile phones and televisions will go up due to a hike in customs duty.

Given that the Lok Sabha polls are going to be held sometime next year, Union Budget 2018 has primarily focussed on the rural economy. Benefits have been showered upon farmers and the underprivileged, ranging from 1.5 times increase in minimum support price to an all-new National Health Policy Scheme, providing a healthcare cover of Rs5 lakh a year to 10 crore poor and vulnerable families. Under the previous Rashtriya Swasthya Bima Yojana, it was only Rs30,000 per family. It is a welcome move considering medical inflation is growing at a faster clip in India compared to general inflation. But there are negative aspects as well. If you are still wondering about the good, the bad and ugly parts of the budget, here is a detailed analysis of what it means and how you can rejig your finances to leverage it most.

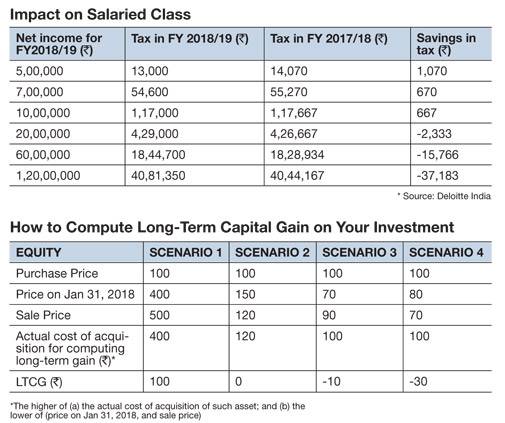

Sleight of Hand for the Salaried?

Jaitley said in his speech that the government had already made several changes in personal income tax rates over the last three years, suggesting one should not expect more. Interestingly, the standard deduction of Rs40,000 has been brought back this year, but the government has taken away two key exemptions - the transport allowance of Rs19,200 a year and medical expenditure worth Rs15,000 per annum. So, the net increase comes to Rs5,800 (Rs40,000 minus Rs34,200), only a marginal benefit for the salaried class.

Moreover, the three per cent cess (two per cent for primary education and one per cent for secondary and higher education) has been increased to four per cent on the tax payable to cater to the educational and healthcare needs of rural families and those below the poverty line. Although it may strain your budget, the additional taxation will amass an estimated Rs11,000 crore.

As far as the salaried class is concerned, it seems Jaitley has put the money in one pocket and taken it out from another. The Rs40,000 standard deduction and an increase in cess translate in tax savings of Rs1,070-667 for an individual with an income of Rs5-10 lakh. However, tax benefits continue to dip with the rise in income. For instance, people earning Rs60 lakh a year will have to bear an additional tax burden of Rs15,766 (see table Impact on Salaried Taxpayer). But here is the positive side. With the medical reimbursement being subsumed with the standard deduction, one does not have to submit medical bills at the end of every month to claim tax exemption.

Akhil Chandna, Director, Grant Thornton India, says, "The Finance Minister enthused the salaried class by reintroducing standard deduction, but soon gave it away by withdrawing current exemptions on transport allowance and medical reimbursement. Together with the additional education cess of 1 per cent, there is not too much for the salaried class in this budget."

LTCG Tax

Long-term capital gain or LTCG tax has been reintroduced on capital gains exceeding Rs1 lakh. It is proposed to be levied at 10 per cent without allowing any indexation benefit. The holding period for calculating LTCG remains one year from the date of share purchase.

The good news is that existing investors will be exempted from paying it until January 31, 2018. All gains made after this cut-off date will be taxed, though. Imposing LTCG tax, however, will be a double whammy for investors who pay the Securities Transaction Tax, or STT. The government has already imposed STT on transactions in shares, bonds and debentures.

Calculating LTCG: LTCG is calculated by deducting the cost price of the share from its sale price. To calculate the cost of acquisitions in respect of long-term capital asset (before February 1, 2018), it shall be deemed higher of

a) the actual cost of acquisition of such asset; and

b) lower of

(i) the fair market value of such asset (as on January 31, 2018); and

(ii) the full value of the consideration received or accruing as a result of the capital asset transfer

Explaining the method of calculation in his budget speech, the Finance Minister gave an example. "If an equity share is purchased six months before January 31, 2018, at Rs100 and the highest price quoted on January 31, 2018, in respect of this share is Rs120, there will be no tax on the gain of Rs20 if this share is sold after one year from the date of purchase. However, any gain in excess of Rs20 earned after January 31, 2018, will be taxed at 10 per cent if this share is sold after July 31, 2018. The gains from equity share held up to one year will remain short-term capital gain and will continue to be taxed at the rate of 15 per cent."

The example given above takes into consideration only the scenario where prices go up. To understand how to calculate capital gain when prices go down see table Computing Long-term Capital Gains.

Impact: Market experts say the imposition of LTCG tax may lead to portfolio churning every year as people may book their long-term capital gains (if exceeding Rs1 lakh) annually to exhaust the threshold limit of Rs1 lakh. This, however, runs against the principle that one should stay in equities for the long term. Says Archit Gupta, founder and Chief Executive Officer of tax solutions firm ClearTax, "People may sell their stocks towards the end of the year to avail of the Rs1 lakh limit next year. But this is not what one should do as the portfolio should be in tune with your long-term goals."

The imposition of LTCG tax on mutual funds can also boost sales of insurance policies considering that the maturity amount is completely tax-free under life insurance.

"ULIP emerges as a beneficial long-term investment option under the new tax regime. Overall economic growth and more people joining the formal economy will give impetus to the growth of the life insurance sector," says Pankaj Razdan, Deputy Chief Executive of Aditya Birla Financial Services Group, and Managing Director and CEO of Birla Sun Life Insurance Company.

What will be the impact on the stock markets? The Sensex went down 839 points the day after the budget, which shows the markets were jittery. But according to Rahul Jain, Head of Edelweiss Personal Wealth Advisory, "On the investment front, the introduction of 10 per cent LTCG tax on equities is a sentimental negative and that too, for the short term. Globally, most countries have the LTCG tax. Given the grandfathering of LTCG by the government, it should not be a big deterrent."

The dividend option: Another proposal is the introduction of a 10 per cent Dividend Distribution Tax (DDT) on the dividend options of equity funds to bring them on par with the growth schemes. But this move may impact the inflow in balance funds where investors are primarily entering because they expect regular dividends.

It is advisable not to opt for dividend option mutual funds (primarily balanced funds) if you are eyeing balanced funds and hope to earn dividends every month. Instead, go for a systematic withdrawal plan, which allows you to withdraw every month. It will attract LTCG tax if the gain exceeds the limit of Rs1 lakh.

What this family thinks

Background: The family with whom we have talked has seven members - Sachin Gupta, his wife Tripti, children Aarna and Arika, his grandmother, grandfather and great-grandmother. Gupta runs his family business, a stockbroking services firm, as the CEO. The family has controlled expenses, good savings and a well-structured financial plan in place.

Budget expectations: Like many people, the Guptas were looking forward to a revision in income tax slab and a rise in basic exemption limit. "We expected that the basic exemption limit would be increased by at least Rs50,000 to Rs3 lakh, reducing the IT burden. Plus, it would have increased disposable income in the hands of the lower-income groups," says Gupta. An increase in deduction limits under section 80C by Rs50,000 (to Rs2 lakh) could have incentivised people to save more. The enhanced limits should have been available to first-time investors in capital markets so that people are motivated to reap the benefits of stock markets. There should have been tax reduction on petrol and diesel whose current tax implications are exorbitantly high in India.

Budget impact: Gupta says there is very little cheer in the 2018 budget. But there are a couple of things that will benefit the common man. Senior citizens have gained considerably as the tax exemption limit on interest income has been raised from Rs10,000 to Rs50,000 with no TDS deduction on such income. Also, deduction on health insurance premium has been upped to Rs50,000 under section 80D.

There were high expectations regarding tax rebate but it was not addressed. The government should have brought a tax percentage cut-down for those falling under the higher tax bracket. Steps should have been taken towards reducing petrol and diesel prices. Also, items such as mobile phone, television, car, furniture and jewellery will now be costlier. Education expenses are soaring as well but the education cess has been increased from 3 per cent to 4 per cent.

Gupta feels the deduction limit under section 80C should have been raised to motivatepeople towards equity investments. Instead,the tax on long-term capital gains - 10 per cent levied on gains exceeding Rs1 lakh - is very disappointing. This tax comes as a big burden on business people like Gupta as they are already paying taxes such as STT. "As it was the last full-fledged budget of the current government, we expected a lot better," he says.

Benefits for Senior Citizens

There is some relief for senior citizens in the budget. As old and retired people tend to depend on interest income, the exemption limit on fixed and recurring deposits (with banks and post offices) has been increased from Rs10,000 to Rs50,000. Moreover, no tax will be deducted at source on such incomes under section 194A.

Considering that medical cost tends to go up as one advances in age, the government has also increased the deduction limit for health insurance premium and/or medical expenditure from Rs30,000 to Rs50,000 under section 80D.

Antony Jacob, CEO of Apollo Munich Health Insurance Company, says, "This is really good news for senior citizens as they will be able to claim the benefit of a deduction up to Rs50,000 per annum in terms of health insurance premium." The deduction limit for medical expenditure involving certain critical illnesses has also been increased from Rs60,000 (in case of senior citizens) and Rs80,000 (in case of super senior citizens who are above 80) to Rs1 lakh irrespective of the age slab, under section 80DDB.

For the pension scheme called Pradhan Mantri Vaya Vandana Yojana under the Life Insurance Corporation of India (LIC), the existing investment limit of Rs7.5 lakh has been raised to Rs15 lakh.

The scheme provides an assured return of 8 per cent over a tenure of 10 years. In case there is a shortfall between the actual returns earned and the guaranteed return, the government will subsidise LIC for the same. Senior citizens can increase their investments in the scheme, considering the high rate of interest it is offering when deposit and interest rates on small savings schemes are at a record low.

Cryptocurrencies: Should You Invest?

As several investors dabble in cryptocurrencies with little or no knowledge about the risks involved, Jaitley put out a word of caution against investing in virtual currencies. It came after three warnings were issued by the Reserve Bank of India. In his budget speech, Jaitley said, "The government does not consider cryptocurrencies legal tender or coin and will take all measures to eliminate the use of these crypto assets in financing illegitimate activities or as part of the payment system."

Ashish Agarwal, Founder of Bitsachs, India's first multi crypto tokens exchange, is of the opinion that "the Finance Minister's statement does not make bitcoin illegal in India. But it will create panic among investors and service providers, most importantly the banks. If banks stop support, exchanges will have to shut down services with fiat money."

Investing in cryptocurrency as a commodity is "still an open question as Jaitley has not given a black-and-white answer on the investment side of cryptocurrency.