TTill the end of CY2017, money was up for grabs, and plenty of it, even if you were not an extremely savvy investor always picking the right stocks and timing things right. A back-of-the-envelope calculation reveals nearly 90 per cent of the BSE 500 stocks posted positive returns last year. It means had you randomly picked up 10 stocks, nine out of those 10 were sure to ring the cash register. The markets had entered the Goldilocks phase at the time; there was low volatility or choppiness, and returns were high. Most mid-cap and small-cap indices returned huge profits.

But now a string of events, along with already sky-high valuations, has made the stocks jittery. Since the beginning of CY2018, markets have seemingly entered choppy waters, and investors who have come in late are seeing a sea of red in their portfolios. The Sensex has tumbled nearly 2,670 points or 7.2 per cent from its peak in January this year. Ditto for other indices such as the BSE Mid-cap and the BSE Small-cap that have skidded 10.5 per cent and 12 per cent, respectively. In other words, it is a new phase in the market where people have to ask the right questions before investing. Ask yourself if it is a crash or correction, a new trend setting in or some minor volatility that has always plagued the market. Should you invest more now? Has the market become riskier or has the correction brought stocks down to comfortable valuation levels?

Pricey Equities Are Dicey

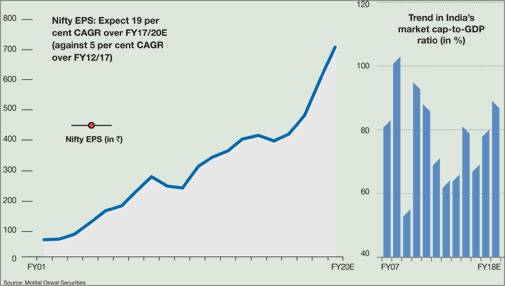

Of all the factors driving the market, valuation is still a major cause of worry. Despite earnings downgrades, markets kept scaling new highs, largely fuelled by liquidity, taking Nifty valuations to 18-19x its FY2018/19 estimated earnings, which is slightly above its long-term average of about 17x earnings. Even on broader parameters like the market cap-to-GDP ratio, now at 90 per cent of 2017/18 estimated GDP, valuations are way beyond comfortable levels (see chart Trend in India's Market Cap to GDP).

India is not alone. Globally, Shiller's cyclically adjusted price-to-earnings or CAPE ratio (a valuation measure usually applied to the US S&P 500 equity market) at current levels of 32x is much higher than the past average of 15x or that of 27x, seen just before the global equity market crashed in 2008. Increasing valuation risks across the globe only add to Indias woes as the markets here will be in step with others.

Flashes of Amber, Globally

Apart from valuations, markets are increasingly factoring in risks of higher crude oil prices. With global commodity prices soaring, including crude oil prices, investors are weighing inflation risks. Consequently, global bond yields have spiked, with the benchmark U.S. 10-year Treasury yield hitting a four-year high at about 2.9 per cent.

Rising US bond yields could have its implications on foreign inflows, which have been the prime source of optimism in the past. Imposition of long-term capital gains (LTCG) tax by the government in its recently concluded Union Budget has only compounded foreign investors' worry. During 2017, foreign investors put nearly $7.7 billion in the Indian equity markets compared to $2.9 billion in 2016 (see table Investments and Money Churners). Assuming part of it is merely tactical money, any outflow or change in views will cause volatility. Foreign institutional investors, or FIIs, have already caused huge volatility by selling close to $1 billion of their investments in the Indian equity markets. However, experts are still expecting robust inflow. "After 2008, we never had a year of negative inflow. We could have a lesser inflow but not a negative one. We anticipate a robust inflow on the back of rupee appreciation and the India growth story," says Harendra Kumar, Managing Director and Head of Institutional Equities at Elara Capital.

Meanwhile, the major tax overhaul in the US, including $1.5 trillion tax relief for corporate bodies and individuals, has fuelled concerns about the U.S. balance sheet risk and hardening of the global yield curve, which may lead to a possible rate hike by the Reserve Bank of India. Do not forget that tactical money tends to shift offshore as investors consider equity to be more expensive than debt or interest-bearing securities.

Choppiness, For Now

All this means stock markets could become choppier in the coming year. "Volatility was unusually low in 2017, not just in India but also globally. It was not sustainable, and the markets are becoming volatile again. We expect equities to be more volatile with relatively modest returns this year than in 2017," says Harsha Upadhyaya, Chief Investment Officer (Equities) at Kotak Mutual Fund.

Today, investors are worried whether the Indian stock markets are going through a correction phase. Will imposition of LTCG tax impact sentiment? And how will markets react with the U.S. yields rising and with the general elections in India next year?

"The correction over the past few weeks can be ascribed to unsupportive global developments as well as domestic policy events (especially the Union Budget). Hardening of bond yields globally is one of the key factors driving the market correction. Bond yields in India have hardened from 6.3 per cent in July 2017 to ~7.6 per cent. We think after the rise in bond yields, the markets (especially mid-caps) were looking expensive. Mid-caps were trading at a premium of 40 per cent to large-caps - an all-time high. The recent correction, however, has moderated this premium," observes Siddhartha Khemka, Head of Retail Research at Motilal Oswal Securities.

What is certain at this time is uncertainty, with a bias towards the equity market correction. "Given the current state of affairs, both international, as well as domestic, equity markets could continue to be volatile in the next five-six months. Globally, central banks, including the U.S. Fed, will be in action and movement in commodity prices will impact equity markets," he adds.

Earnings to Lead Revival

Volatility should not mean deep correction. It may not even be prudent to wait for a deep correction because the earnings growth outlook is still good. As the famous saying goes, "In the long run, markets are slaves of earnings," and markets are only supported by earnings growth.

FY2017/18 saw the steepest earnings downgrades, driven by a slowdown fear caused by the impact of demonetisation on the informal economy and the implementation of Goods and Services Tax (GST). The consensus expected Nifty earnings per share (EPS) to be around `550 at the beginning of the year, which is now `489, down about 11 per cent. But in this process, earnings have made a strong base over the last four years (see chart Nifty EPS).

To put things in perspective, Nifty EPS hardly moved up from `407 in 2013/14 to `421 in 2016/17. It is only in 2017/18 and 2018/19 that earnings are expected to move to `489 and `598, respectively, a growth of nearly 42 per cent in absolute terms and 19 per cent annualised.

The momentum was already seen in the December quarter results. "The current result season has been broadly in line with expectations. However, due to disappointment from heavyweights such as State Bank of India (SBI), Tata Motors, Lupin and Oil and Natural Gas Corporation, the overall Nifty earnings growth in Q3 has been 7 per cent. Excluding SBI, Nifty PAT grew 16.6 per cent compared to an estimated 17.5 per cent. We believe overall earnings growth is likely to be strong in the next two years. And given the expectation of a pick-up in earnings, valuations could sustain at current levels," says Khemka.

Arun Thukral, MD and CEO of Axis Securities, concurs. "The rally was on expectations of earnings growth, which is slowly materialising. The earnings revival has been observed from Q2 2017/18 where an annual growth of 10 per cent was witnessed, followed by a Q3 growth of 22 per cent compared to the same quarter in 2016/17. Moreover, the earnings revival has been broad-based except for PSU banks and oil marketing companies, or OMCs."

Reality Check

Should you buy into this correction? Interestingly, global and domestic economic growth are coinciding for the first time after 2007 and 2008. The India Economic Survey 2018 pegs the country's economic growth at 7-7.5 per cent in 2018/19 compared to 6.75 per cent in 2017/18. Also, the government's push for additional spending on infrastructure and social schemes and the expected benefits of recent reforms like GST should start to reflect on overall growth ahead.

The global environment has been conducive as well. China has stabilised; Western economies are growing faster, and oil-producing Gulf countries are recovering with oil prices hovering well above suitability levels. The International Monetary Fund, in its January 2018 Global Economic Outlook report, projected global economic growth of 3.9 per cent in 2018, against 3.2 per cent in 2016 and 3.7 per cent in 2017.

The IMF says in its report, "Global economic activity continues to firm up. Global output is estimated to have grown by 3.7 percent in 2017. Global growth forecasts for 2018 and 2019 have been revised upward by 0.2 percentage point to 3.9 percent. The revision reflects increased global growth momentum and the expected impact of the recently approved U.S. tax policy changes."

The US tax cut for both corporate bodies and individuals means more money for companies and consumers. It can fuel global growth considering the US is one of the largest consuming nations in the world. Another critical factor that can work in favour of the markets is liquidity. While the FII mood may swing as they are already heavily invested in the Indian market, domestic money flows are buoyant.

In fact, most domestic mutual funds are sitting on cash. Second, a lot of money has been shifted to balanced funds, awaiting the correction. Third, mutual fund schemes, which have stopped accepting fresh investments as they fear higher valuations and lack of investment ideas, will be waiting for the right opportunity to strike. If they come back, that will be in addition to the existing SIPs of about `6,000 crore waiting every month for deployment.

The Hunting Ground

The above insights bring us to the muted point - if fundamentals are in good shape, it may not be prudent to sell everything and wait for a deep correction as timing the market could be a risky proposition.

"The correction in the market has been driven by global risk aversion on the back of expected rise in the pace of interest rate hikes in the US, coupled with mopping up of excess liquidity. The markets are expected to consolidate at current levels in the short run, ahead of the events lined up before the next US Fed meet in mid-March. So, any correction should be used as a prospect to buy at attractive levels. People are advised to stay invested in quality companies with growth potential, use the opportunity to add to the existing portfolio and take exposure in the good companies they had missed in the last rally due to a run-up in valuations," says Thukral of Axis Securities.

At what levels markets would become attractive? Past market average valuations at around 15-16 times one-year forward earnings happen to be a good spot to hunt for bargains and look for increasing exposure. If correction takes place at around 15-16 times forward earnings, Nifty would be about 8,970-9,568 or 8-13.5 per cent lower than its current level of 10,378.

Investors would be better off buying the weakness and using the volatility to their advantage to gradually increase their exposure to equity. Warren Buffet, the legendary investor, defines risk as permanent loss of capital rather than volatility. Investors should fear the losses that could be caused by poor investment ideas or businesses rather than volatility. The second important point emphasised by the market pundits is to stay

During past rallies, investors have bought quite a few stocks in the hope of a turnaround irrespective of the quality of the business and its management. Valuations and investor interest in these stocks are at the highest, particularly in the mid-cap and the small-cap space. Moreover, at current valuations, the BSE Midcap and the BSE Small Cap indices are trading at 40 times and 114 times their trailing 12-month earnings, respectively. Investors have started factoring in many future expectations in the case of mid-cap and small-cap companies, which may or may not deliver in the near term, and that could mean a longer waiting period.

"In the recent correction phase, the mid-cap and the small-cap segments have seen more declines than the large-cap segment. However, premium valuations of these segments continue compared to the large-cap segment. If one is investing for more than five years and can withstand higher interim volatility, only then he/she should choose the mid-cap or the small-cap segment," says Upadhyaya.with quality names and not to leverage.

Strategy Rejig May Help

All in all, stock markets are at that stage where investors will have to dig deeper and find stocks with still some value left, especially in the mid- and small-cap categories. "As for valuation, the mid- and small-cap space looks stretched, but there are certain pockets which are still at a reasonable valuation and offer opportunities to make money," says Prateek Agarwal, Business Head and Chief Investment Officer at ASK Investment Managers. The rising tide of liquidity is not going to lift all boats; so, stock price appreciation will be more selective. It means nine out of 10 stocks are not going to rise. Expect more of the reverse to happen, which means one or two out of 10 will end up with positive returns. It also means you have to be sharper and more vigilant with your stock selection.

Another big factor is the holding period. Gone are the days when investors could make 30-40 per cent returns in a year. So, expect a fall in returns, which is perhaps more realistic. And here is one last criterion: Now you may have to hold on to equities a lot longer. If you are not prepared to invest and hold on to stocks for three to five years, this market may not be for you.

{mosimage}