In a sector where delays are common, Udaipur-based road developer GR Infraprojects has built a reputation of completing its projects well before deadlines. Founded in 1965, the company executed small projects of the public works department in Rajasthan until 2007. That year, GR Infra got a contract from Ashoka Buildcon, which had completed barely a quarter of a project it had been working on for two years in Barmer district. It roped in GR Infra to finish half of the work (69.5 km). "We finished our work in 10 months flat," says Vinod Agarwal, GR Infra's Managing Director. "The project taught us the benefits of finishing work quickly. Today, our strength lies in delivering projects ahead of schedule."

In September 2012, the company completed the 73.5-km Hazaribagh-to-Ranchi project six months before the deadline. In February, it finished work on a 47-km Shillong bypass project 12 months before the due date. Another project in Rajasthan is set for completion in December, about eight months before schedule. So far, GR Infra has executed 155 projects totaling 3,200 lane km in Rajasthan, Haryana, Uttar Pradesh, Bihar and Jharkhand. Project delivery, however, is not the company's only focus area. Bulk of its revenue comes from engineering, procurement and construction (EPC) contracts which it gets from large concessionaires such as IL&FS Transportation Networks and highways authorities.

Agarwal, the second son of GR Infra's founder Gumani Ram Agarwal, says the

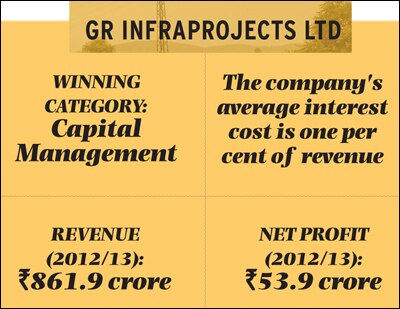

company lays huge emphasis on timely collection of payments from clients. "Late payments result in a rise in overall project costs and lower margins," he says. The average payment cycle for EPC contracts is one month for GR Infra compared with three to four months for other companies. This has helped it keep its cash flow healthy and interest costs low. Agarwal says his average interest cost is one per cent of revenue, much lower than industry standards of four to five per cent. GR Infra has also managed to keep its debt under control - the consolidated debt-to-equity ratio is 0.95 to 1.

Its strong balance sheet has attracted several investors. The company got Rs 80 crore funding from Motilal Oswal Private Equity Advisors and IDFC Investment Advisors for a 15 per cent stake in 2011. Japan Vyas, Director at IDFC Investment Advisors, says the investment was based on the company's credibility, execution track record and healthy financials. "They have completed projects well within time and costs," he says.

The company's revenue grew at a compounded annual pace of 64 per cent between 2008/09 and 2011/12. But a slowdown in the infrastructure sector and a falling rupee, which makes its machinery and bitumen imports costlier, has hurt the company. As a result, its revenue dropped more than 12 per cent to Rs 862 crore in 2012/13.

IDFC's Vyas says the issues affecting the infrastructure sector are also troubling GR Infra. "We expect the company to take away market share from others in the event of a sectoral revival because its books are fairly solid." Parvesh Minocha, Group Managing Director (transportation division) at consultancy Feedback Infra, agrees. The infrastructure sector will continue to shrink until the economy grows at a pace of seven per cent, he says. "But when the sector upturns, the company will be quick to bounce back."