This was an economic cliff-hanger, and

Manmohan Singh knows a thing or two about staring into the abyss. A disastrous Parliament session, a brewing divorce from a petulant partner, the bad odour of corruption, foot-dragging and stasis, sickly business sentiment and citizens sick of high prices had combined to drive India's government into a dark corner.

The ground finally began to move about two months after a new finance minister took charge, and it was clear the September 13-14 announcements on

subsidies and foreign investment were the first broadside from a rejuvenated prime minister widely seen as having done little to arrest a sliding economy.

Almost overnight, the critics have faded into the background with corporate India, economists and the media standing up to applaud the measures. Some even call it Reforms 2.0, a reference to the structural changes Singh himself uncorked in 1991. The seed for the high octane announcements was sown about two months earlier. Singh and Congress president Sonia Gandhi flew to Assam together to assess the flood damage in the state towards the end of July. "From the time they left Delhi at about 8 am, to the time they returned at about 7.30 pm, the two spent a lot of time onboard discussing several issues, particularly reforms," says a senior government official, promising candour in return for anonymity.

Over the next few weeks, Singh persisted with his efforts to gain support. By end August, economic data bolstered his "now or never" argument within his Congress party. The economy had grown a modest 5.5 per cent in the April-June period, the second consecutive quarter of sub-six per cent growth.

Growth this slow was last seen a decade ago. Singh needed two more meetings to convince Gandhi. One in August after he returned from the Non-Aligned Movement summit in Tehran. And, the next one after the rowdy monsoon session of Parliament, where the Congress was on the defensive after government auditor Comptroller and Auditor General's critical report on the allocation of coal blocks. Singh's urgency was no doubt also fuelled by the nadir to which his own image of integrity had sunk.

The clincher in the prime minister's pitch was his argument that without immediate action there would be not enough money to fund a proposed food security legislation. The food bill, which will cost up to Rs 1.2 trillion (one trillion equals 100,000 crore) annually, is a plan cherished by Gandhi and her son Rahul. Several analysts agree with the Congress view that the food security law could be a plank on which the party could hold its own in an election - just like an employment guarantee scheme introduced in 2005, NREGA, helped it get re-elected in 2009.

Gandhi eventually gave her assent early in September. Within a few days, the United Progressive Alliance (UPA) government hiked the price of diesel by 12 per cent and created more space for foreign investment in contentious areas such as multi-brand retail, aviation and broadcasting. Fiats notifying the changes were issued within a week.

The firm resolve with which Singh and his Cabinet are moving is long overdue - and more announcements are promised in the weeks ahead - but the changes don't constitute a magic potion that will transform the economy overnight. While industry associations and corporate leaders have been applauding Singh, catch them in more reflective moments and they will tell you that the country needs further and deeper reforms alongside continuous political stability for the economy to rebound.

"We need to have more," says Sanjiv Goenka, Chairman, RPSanjiv Goenka Group, echoing the view of some two dozen economists, financial experts and company CEOs Business Today spoke to. "Hopefully it is not too late."

Credit profile will benefit both from fiscal consolidation and growth enhancing structural reforms: Andrew Colquhoun

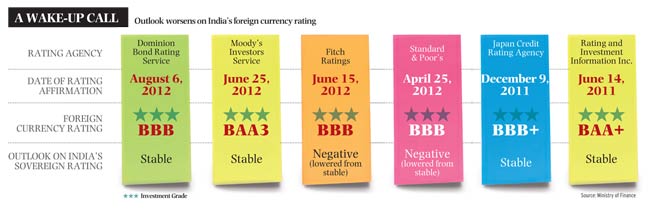

So far, credit rating agencies, two of which - Fitch Ratings and Standard & Poor's - had lowered India's rating from 'stable' to 'negative' in recent months, have not yet rushed to applaud or to revise their view. "We don't see the reforms as sufficiently material in a way that would lead us to review our negative outlook on ratings," says Hong Kong-based Andrew Colquhoun, Senior Director, Sovereigns, Fitch.

Others are only a few shades less pessimistic. "These measures have pulled the economy back from the brink," says D.K. Joshi, Senior Director and Chief Economist of rating agency Crisil. He adds that the steps taken would, indeed, shore up business sentiment and expand the pipeline of investments, but it would be a slow process given the uncertain global environment. "I see a potentially good 12 months under Prime Minister Singh and a crack economy team," says Glenn Levine, Senior Economist, Moody's Analytics, a research division that has no relation with the ratings teams at the agency.

The icing on the cake would have been a stimulus through an interest rate cut and fiscal measures that wouldn't trigger demand-pulled inflationary pressures: Harsh Goenka

But he adds he is not yet revising his gross domestic product (GDP) growth forecast for India in 2012/13, which would remain at 5.5 per cent. Banks and research units are equally circumspect. "It is a good signal," says Singapore-based Manoj Vohra, Research Head, Economist Intelligence Unit (EIU). But the EIU, too, has stuck so far to its earlier growth forecast for 2012/13, set at six per cent. It is the same story with Citigroup, which forecast 5.4 per cent growth for the same year.

However, even after the announcement, Standard Chartered Bank has lowered its growth forecast for the same period from 6.2 to 5.4 per cent, concluding that the damage the economy had already suffered could not be reversed so soon. Standard & Poor's lowered its GDP forecast by one percentage point to 5.5 per cent on September 24, as part of a broader revision for Asia-Pacific economies.

Industry's Wish ListSo, what more should be done to move the needle on the economy? "A host of things," says Kris Gopalakrishnan, Executive Chairman, Infosys. "Two of them are fast-tracking and executing infrastructure projects and implementing the goods and services tax (GST)."

It is a good start. We need to have more (reforms): Sanjiv Goenka

India at present has a patchwork of indirect taxes, varying from state to state, which the GST seeks to replace with a single one, in effect creating a common market across the country. The difference in tax structure across states acts as a fiscal barrier between them and makes doing business more costly. Different bodies which have studied the subject, including the 13th Finance Commission, have all supported a uniform tax structure, estimating that it could add 0.9 to 1.7 per cent to the country's GDP. "FDI (in retail) will definitely allow us to become debt-free faster. But the real turning point for modern retail will be when GST comes in," says Kishore Biyani, Founder & Group CEO, Future Group.

{mosimage}

A Much-needed Boost

A rule that was changed to allegedly benefit one airline in 1996 was finally altered last week. Ironically, this time, too, the change seems to have been made to help another airline.

After opening up Indian aviation to private operators in 1990, the government, in 1993, allowed foreign airlines to own stakes in Indian carriers. When the Tatas were looking to re-enter Indian aviation with Singapore Airlines as their partner, however, the government in 1997 - reportedly under pressure from Jet Airways- disallowed foreign airlines from owning stake in their Indian counterparts. Even at the start of this millennium, when the BJP-led NDA government was looking to partially-privatise Air India, foreign airlines were eventually barred from pitching for a stake. An industry person on the condition of anonymity says: "The Parliamentary Standing Committee on this matter quoted verbatim from a FICCI committee report. And the head of the FICCI aviation committee at that time was Jet Airways owner Naresh Goyal."

Over the last one year, however, there has been a growing demand - led largely by Vijay Mallya - to save his teetering-on-the-brink carrier Kingfisher Airlines- that this rule be discontinued. On September 14 the government finally permitted foreign airlines to own up to 49 per cent in Indian carriers.

While the verdict on whether Kingfisher will gain from this policy change is divided, there is no denying the benefits that will accrue to the sector from the decision. "Allowing 49 per cent stake to foreign airlines will bring capital, global connectivity, technology and best practices," says Amber Dubey, partner and head-Aviation, KPMG.

The biggest positive will be a fresh source of capital. The total debt of all the Indian airlines is pegged at Rs 75,000 crore, with banks having an exposure of Rs 40,000 crore. "Airline promoters don't have money. The government doesn't have money. Banks are tired of lending to sector with most of it becoming non-performing assets. The only alternative is FDI," says Chokkalingam G, Executive Director and Chief Investment Officer, Centrum Wealth Management. However, Chokkalingam adds that bankers may not be enthused by the announcement alone. "Lending sentiment towards the sector will improve once bankers see some positive movement from foreign airlines," he adds. Along with better access to capital, the move is also likely to improve sentiment in leasing markets for Indian airlines. "Due to Air India's gigantic losses and Kingfisher's downward spiral, aircraft and engine leasing companies were unwilling to sign contracts with even relatively debt-free companies like GoAir and IndiGo. The policy change will certainly improve sentiment in these markets," says an industry person on the condition of anonymity.

Ramesh Vaidyanathan, Partner, Advaya Legal feels one of the benefits of the FDI announcement will be the reduction in political interference in the sector. "The discretion of the babus is likely to give way to transparency," he says. Allocation of parking and landing slots, granting of pilot licences, etc, are expected to see more transparency.

But how are foreign airlines viewing this move? Carriers from the Gulf like Emirates, Etihad Airways and Qatar Airways, other international behemoths like British Airways, Lufthansa, Singapore Airlines, and low-cost champion AirAsia have shown interest in Indian carriers. But most industry experts agree that a deal is highly unlikely in the short term given the weak balance sheets of Indian airlines and their structural challenges.

"If we get relief in airport charges and fuel, it would make a huge difference," says Alex Hilgers, Director-South Asia, Lufthansa. Hilgers says FDI is not very important for Lufthansa. The airline is instead focusing on increasing capacity and bringing in a new business class product to India with the Boeing 747-8. The airline is the launch customer of the newest aircraft in the Jumbo Jet family, the 747-8, and has chosen Delhi and Bangalore - along with Washington - to fly to in this aircraft. Also, Lufthansa's muted response to the FDI announcement is in keeping with its international strategy of concentrating on integrating recent acquisitions rather than making new ones.

Others are a little more enthusiastic. "India is one of the world's most important aviation markets. While Emirates' philosophy is to focus on organic growth, we always welcome any reform which liberalises markets, including FDI rules," says an Emirates spokesperson. The airline, which flies into 10 Indian cities, operates 185 flights a week to India and deploys 11 per cent of its total capacity here, has little room to expand further.

Industry persons also feel that the policy change could lead to the formation of new airlines. For an airline like AirAsia, which is very bullish on India despite the challenges, joining hands with a start-up is the most likely route of entry. "We have joint ventures in Thailand, Indonesia, Philippines and Japan. In each of these AirAsia owns 49 per cent and 51 per cent is owned by the local entity. The local partners in all these cases have been start-ups. This was a deliberate decision as there is no baggage and our branding can be very strong," explains Sunil Nair, country head-India, AirAsia.

However, others like Vaidyanathan of Advaya Legal feel that action in the start-up airlines space is unlikely. "I would be surprised if there is a deluge of action in the new airlines space. Most of the action will be seen among existing airline companies," he says. "Investments will come only to efficiently run entities that are losing out due to lack of cash."

The consensus among industry insiders is that SpiceJet and GoAir are likely to benefit the most from the changed rules. Management teams of both airlines were unavailable for comment. Kingfisher will be an attractive target only if valuations are very cheap or its debts are wiped off the balance sheet. The only positive for a prospective Kingfisher buyer is its brand recall. "Regaining market share may not be difficult for Kingfisher because even now the brand has high recall," says S.P. Tulsian, independent investment advisor. For a deal to go through with Jet Airways and IndiGo, there would have to be restructuring of promoter shareholding. Jet Airways is 80 per cent owned by Naresh Goyal via Tailwinds, an entity registered in the tax haven of Isle of Mann. With IndiGo, 48 per cent is held by Rakesh Gangwal through a US-based company called Caelum Investments, 51 per cent by InterGlobe Aviation and about one per cent by Chairman Rahul Bhatia and others in their personal capacities.

While most are enthusiastic about foreign airlines being allowed to invest in Indian carriers, there are some who are raising concerns. Key among the concerns raised is the fear that the new money may be used by airlines to chase market share. "A foreign airline partner could lead to irrational behaviour in terms of pricing playing out in the market again," says an industry person on the condition of anonymity. The other concern is whether this decision marks the end of an Indian legacy carrier. "It will be difficult for Indian airlines to aspire to become legacy carriers once Emirates or Singapore Airlines invest in them. They will most likely end up becoming feeder services into big hubs like Dubai or Singapore," says another industry insider who does not wish to be named.

-Geetanjali Shukla

|

Supporting legislative changes, alongside the GST, are also required for the country to derive full benefit from the move to open up retail to foreign investment. Changes, for instance, are required in the Agricultural Produce Market Committee (APMC) Act, which governs the relationship between wholesalers - who sell through wholesale markets or mandis - and farmers.

"The APMC does not allow retailers to source from farmers directly," says Ankur Bisen, Associate Vice President, Retail and Consumer Products, at management consulting firm Technopak.

Similarly, speeding up infrastructure projects requires, above all, the proposed new Land Acquisition Bill becoming law. Data from Centre for Monitoring Indian Economy shows that projects of around Rs 4.9 trillion, about six per cent of the country's GDP, are currently stalled. A key reason, in many cases, is the promoter's inability to acquire the land required for them. The proposed bill has been referred to a group of ministers.

Passing the GST will require a constitutional amendment, which means it needs majority assent in both Houses of Parliament and support of two-thirds of members present at the time of voting. This, in turn, implies it cannot go through without the support of the main opposition party, the Bharatiya Janata Party. Ditto with the challenges of getting the amendment ratified by at least half the state assemblies.

Bringing in the new Land Acquisition Bill, too, will demand some Opposition support. And, while no opposition party is implacably opposed to either - as some of them are to FDI in retail, for instance- they have apprehensions about both which need to be tactfully allayed. The big question is: does the UPA government have the political capacity any more to undertake these and other big reforms, given the way it has been weakened and relations with the opposition parties soured since the recent lot of reforms were announced?

The current deadline for implementing GST is April 2013. "I do not think it will be met," says Kavita Rao, Professor, National Institute of Public Finance and Policy.

The survival of the Congress-led government does not seem to be in question immediately, but it is no doubt more vulnerable to the demands and whims of its partners in the UPA coalition. Protesting both the diesel price hike and the entry of FDI in retail, the Trinamool Congress with 19 members of Parliament (MPs) quit the coalition, withdrawing its ministers, reducing the coalition's strength to 254 members in a House of 543.

We had stopped investing in our retail business because of the uncertainty about FDI. That will change now: Venugopal Dhoot

Currently, the minority UPA government survives with the "outside"support of the two leading Uttar Pradesh parties, the Samajwadi Party (SP) and the Bahujan Samaj Party (BSP), with 22 and 21 MPs, respectively, giving the UPA a total strength of 297. While the SP has roundly criticised the reforms, and lent its support to the September 20 Bharat Bandh called by the opposition parties against the decisions, it has also clarified it will continue to support the UPA. The BSP will only announce its decision after an executive committee on October 10. Both are rivals of the Congress in UP and have proved unreliable allies in the past.

BJP MP and former finance minister Yashwant Sinha feels the Congress has tied itself up in knots by playing politics. "When we were in power, we had deregulated the prices of petrol and diesel in 2002, but this government reversed the decision when it came to power in 2004," he says. "Why has Manmohan Singh done this? Because in recent months, he came in for very shrill criticism from the Western media."Among others, Time magazine called Singh an "underachiever" on its cover, while

The Washington Post labelled him a "tragic figure".

Deep CrisisBut that is hardly the only reason. As Singh emphasised in his television address to the nation on September 21, the economy is in serious trouble. He even invoked the crisis of 1991, which forced India to liberalise, to remind listeners of the consequences of further drift. "We are not in that situation now but we must act before people lose confidence in our economy," he said. "The world is not kind to those who don't tackle their own problems."

FDI will bring in not only dollars but also effi ciency in the entire food supply chain. On a long-term basis, it should help correct even food inflation: Harsh Pati Singhania

The problems are hardly a secret. The Indian economy grew by just 5.4 per cent in the first half of the current calendar year, against an average growth of 7.8 per cent in the past five financial years. The rupee has depreciated around 12 per cent against the dollar in the past year, while the current account deficit - the excess of imports over exports - hit a record 4.2 per cent of GDP in 2011/12. In the past few quarters, fresh investments have been tapering off. Fixed capital formation grew a measly 0.65 per cent in the April to June quarter of 2012/13. In the preceding quarter, it had grown a modest 3.61 per cent, and in the quarter before that had actually contracted by 0.1 per cent. Meanwhile, direct tax collections grew just 6.52 per cent in the April to August period, with corporate tax collections rising a measly 0.15 per cent.

Several global retail chains are looking to enter India

Most of all, the fiscal deficit for the current fiscal year has been estimated at Rs 5.13 trillion, or 5.1 per cent of the economy. No less a person than Finance Minister P. Chidambaram has indicated that it may ultimately turn out to be higher.

Not surprisingly, given the deficit - bridged by borrowing - inflation refuses to be tamed. So long as inflation remains high, the Reserve Bank of India remains reluctant to reduce interest rates, which, in turn, may well be affecting growth. Lowered rates alone can pull in investment and create the 50 million non-farm jobs the Planning Commission has targeted for the 12th Five-Year Plan from 2012 to 2017.

It is hardly a coincidence that in the week following the reforms'announcement, the rupee gained 93 paise against the dollar. The diesel price hike - whatever its short-term inflationary impact - is expected to save the government around Rs 15,000 crore a year.

Indeed, tackling the deficit will make all the difference. "Once we lay out the path of fiscal consolidation, and it is a credible path, the RBI will be far more supportive to growth," Chidambaram told a meeting of the Planning Commission on September 15. India's credit profile, too, could improve subsequently. "Credit profile will benefit both from fiscal consolidation and growth enhancing structural reforms," says Fitch Ratings' Colquhoun.

FDI In RetailWhat will be the impact of the most contentious decision - allowing 51 per cent FDI in multi-brand retail? The pros and cons of the step have been debated ad nauseam for years.

It is unfortunate that in this country people do not put good economic decisions ahead of minor political considerations. I am surprised that some political parties are opposing it. It is a shame: Adi Godrej

To its opponents, it means the death of mom-and-pop stores, and no amount of argument will convince them otherwise. Even so, with the Rubicon now crossed, support for the move is coming from stakeholders such as farmers. "FDI in retail will help the farmer, cutting down wastage, and link the buyer with the producer,"says Chengal Reddy, Secretary General, Consortium of Indian Farmers Association. Others such as farmers grouping Bharat Krishak Samaj, too, support FDI in retail. This direct linkage between global chains and farmers, cutting out middlemen, is expected to stem inflationary pressures in the economy, and also improve agri-commodity management.

A number of global retail chains have already shown keen interest in entering India. The US's J.C. Penney has set up sourcing operations here. Others said to be interested in India include France's Group Casio, UK's Sainsbury's, Germany's Lidl and The Netherlands' Royal. "Along with food and grocery, the three big categories where we are likely to see significant interest are pharmacy, home and furniture and durable and electronics," says Raghav Gupta, Principal, Booz & Co. Walmart, which already has a joint venture with Bharti Retail for back-end supply chain management operations in India, is likely to step up its presence further. But many others are still assessing the situation, since the final decision rests with the states, and opposition-ruled states are almost certain to keep the global chains out.

What the government - and the rest of us in the world's third-largest economy by buying power - can best bank on is that the bold changes it is making will turn the sentiment in the economy. This coupled with clearances for mega projects could boost capital investments and push growth. That may take a few quarters to show up but, to paraphrase Singh, late is better than never.

(By Sanjiv Shankaran, Sebastian P.T., Anusha Subramanian, Shamni Pande, Geetanjali Shukla and Anilesh S. Mahajan)