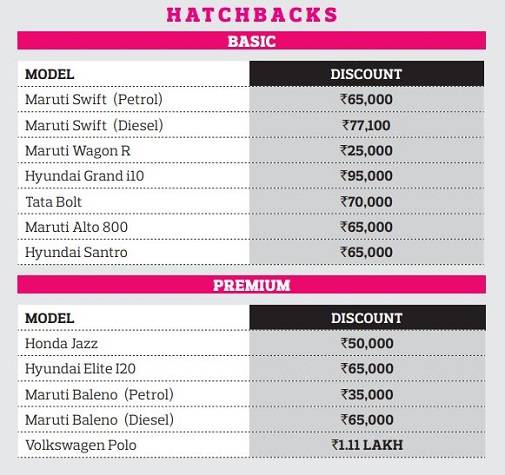

Are you planning to buy a car - perhaps your first wheels or a second one for a family member or a much-coveted upgrade? Traditionally, the festive season is the best time to make a prestige purchase as carmakers, dealers and lenders often come up with substantial discounts and lucrative schemes. Even then, new cars got more expensive year after year. Well, not any more. Economic uncertainties, rise of ride-sharing and car leasing and stringent emission norms have led to a double-digit fall in car sales. As per data from the Society of Indian Automobile Manufacturers (SIAM), overall sales of passenger vehicles declined by 23.54 per cent in April-August 2019 compared to the same period last year. Sales of passenger cars, utility vehicles and vans dipped by 29.41 per cent, 6.27 per cent and 34.04 per cent, respectively, year on year. So, struggling automakers can't sell you enough to boost sales and clear inventories, and most of them are offering great deals. In brief, it has become a buyer's market, and you are getting huge cash discounts, lucrative exchange offers, extended service and warranty, discounted accessories and other freebies.

"Discounts increased a lot, especially on diesel cars, and also in the SUV segment, due to stiff competition. Last year, there was no deal on best-selling SUVs such as Maruti Brezza and Hyundai Creta. But this time, Maruti is offering a discount of Rs 1 lakh on Brezza and Creta comes with a discount of Rs 80,000," says Gagan Modi, Founder and CEO of MyCarHelpline.com.

All this may sound exciting but buying a car still involves plenty of analysis and forethought. There is a smorgasbord of vehicles out there. There is no shortage of deals either. But you must not let aspiration or fantasy blur your judgement and put you in debt for a long time. Before you buy, it is important to assess whether the car matches your requirement, lifestyle and budget, and the exact nature of the benefits you would be getting from a deal. Here are five must-follow tips to make the best of everything and emerge a smart buyer.

Cash Is King

Getting a cash discount upfront makes sound sense as it brings down your total payment and, consequently, the EMI amount and long-term costs. Besides, one's financial situation changes over the years, and the fewer obligations you have, the better it is for you. You will mostly find freebies such as free insurance or accessories, instead of an outright discount, but there lies the problem. Most of these freebies are priced differently by different manufacturers and dealers, and it is difficult to know how much you have gained from the deal. If you have cash in hand, you can buy many of these items from the open market and they might cost you less.

"Insurance premiums quoted by dealers are usually on the higher side compared to online rates. Accessories, too, come with higher price tags. So, it is best to go for deals which offer maximum cash discounts," says Modi. If your preferred car comes with a free insurance offer, check out if you can get a cash discount instead, he adds. C.S. Sudheer, Founder and CEO of Bengaluru-based IndianMoney.com, a financial education company, agrees. "Explore all car insurance plans at the time of purchase. Buying online policies is convenient. Plus, you will be able to pay a lower premium and get better options like easy renewal. In fact, you can save up to 40 per cent on insurance premium compared to what you pay to offline dealers. For instance, you can save Rs 10,000-12,000 on a mid-sized sedan and Rs 14,000-18,000 on an SUV priced over Rs 10 lakh."

But the same may not be true for an extended warranty as it is provided only by manufacturers and so the pricing of services rendered depends entirely on them. Therefore, if you are getting an extended warranty for free or at a discounted pricing, it may be worth taking.

Negotiate for Trade-in Value

When upgrading their cars, people prefer exchange offers to escape the hassles of selling their old vehicles and getting good prices. But this may not be the best idea as dealers often get higher mark-ups on used cars and so paying less increases their profit margins. "In these cases, a dealer is not likely to offer fair market value. As there are no fixed rates in the used car market, one must be ready to negotiate hard to match the best price available," says Modi. "The best way to go about it is to first assess the car on your own. Is the car well maintained and timely serviced? Have there been previous incidents of road accidents, major repairs or issues with tyres and battery life? Check online the estimated value of the vehicle based on good or average condition. And involve a second dealer to make sure that the assessment price is based on car conditions and service history. Then you can approach your dealer for the final valuation and exchange bonus."

Budget It Right

Buying a car is a big affair for most and you may be tempted to stretch your budget for a better model, especially if it comes with an attractive discount. On the other hand, you have to remember that it is not a one-time expense. Maintenance is a recurring expense and you also have to service your loan EMIs. So, instead of getting swayed by discounts, you should stick to your budget.

The next question is - what should be your car budget? "If one can buy the car outright without affecting other important goals, that is the way to go," says Suresh Sadagopan, Founder of Mumbai-based Ladder7 Financial Advisories. But many would find it difficult to amass the entire amount within a reasonable time frame and most people would not like to wait so long. So, should you determine your budget based on your loan eligibility? This could be a risky proposition as lenders may offer a larger amount (these are secured loans, after all). "You can follow the rule of 20-4-10," says Sudheer. "Make a down payment of at least 20 per cent. Make sure that the EMIs are paid within four years. Also ensure that the total monthly expense (the principal amount, the interest paid on it and the insurance premium) does not exceed 10 per cent of the gross income."

Do You Need Diesel?

If you are opting for a diesel car, keep the long-term scenario in mind. Although you will spend less on fuel than you do for a petrol car, it will lead to higher maintenance costs. Experts generally advise one to go for a diesel car in the non-luxury segment only when your daily commute is more than 50 km. Besides, you need to keep in mind the Supreme Court's decision on October 29, 2018, to ban 10-year-old diesel cars in Delhi-NCR, which could be followed by other cities and states. The apex court also ruled that BS-VI emission norms will kick in from next year and no BS-IV vehicle will be sold in India from April 1, 2020. All these may result in more expensive cars and fuels, and current versions (both diesel and petrol cars) may rapidly lose their value. But if it has higher utility and if you are willing to retain your vehicle for its entire life span instead of looking for resale value, go ahead.

Make the Best of Auto Loans

As most of the new cars are purchased with auto loans, lenders, too, have joined the bandwagon to grow their businesses. Selecting the best loan is not easy, though, as it includes calculating and comparing different financing combinations across loan tenures. For instance, you can input the new car's price, your exchange price and different loan tenures to find out what your EMI would be. But the first thing you should be clear about is the extent of finance. There is always some confusion regarding ex-showroom and on-road pricing. But once you have the right information, it will be easy to determine the down payment and plan the tenure and EMI.

As auto loans may continue up to seven years during which your priorities are likely to change, make sure that you know your future options. According to Anuj Kacker, Co-founder and COO of Bengaluru-based fintech firm MoneyTap, you should ask your car loan provider some quick questions to get a better perspective. For example, what is the EMI amount per Rs 1 lakh? What are the processing charges? Is pre-payment allowed or will there be charges and restrictions? What is the type of interest rate - flat or floating? Here is a quick look at the four crucial elements of an auto loan.

Down payment: The 100 per cent finance offer may not always cover 100 per cent as it may not include registration, documentation and insurance costs. Many lenders only offer a certain percentage of the on-road price (ex-showroom price plus registration and insurance costs) and the rest has to be down payment. "Banks mostly offer 80 per cent of the on-road price or 100 per cent of the ex-showroom price. Interestingly, the former is roughly equivalent to 95 per cent of the ex-showroom price. However, a large down payment is always recommended as it reduces high-value EMIs," says Kacker. According to Sudheer of IndianMoney, "EMIs must not exceed 10-15 per cent of your monthly income. Making a big down payment means you will owe less on the car every month and can invest for other financial goals."

Interest versus processing fee: "One should look for both - lower interest rate as well as processing fee waiver - as these will add to your savings. But if you have to choose between the two, grab the lower interest rate deal," says Rishi Mehra, CEO of Wishfin.com, a Noida-based financial planning and lending marketplace. Interest rates matter more and even a small difference of 0.25 per cent will result in better savings than a processing fee waiver. "For auto loans, the repayment tenure varies between three and seven years. So, bargaining for a lower interest rate will lead to more affordable EMIs, and you can also choose to foreclose the loan. On the other hand, the processing fee is just a one-time payment, about 0.5 per cent of the total cost. If you do your research well and purchase a car during the festive season, you may get a waiver," says Kacker of MoneyTap. "If you have a good credit score, you can most certainly negotiate the processing fee and the rate of interest," affirms Aditya Kumar, Founder and CEO of Bengaluru-based digital lending start-up Qbera.

Loan tenure: If you are stretching your budget for a high-end car, a longer tenure will keep the EMI low but increase your interest liability, points out Mehra. It will also hinder your ability to save and invest for other life goals. "Opt for a short tenure if you can pay higher EMIs. This will lower interest costs and you can pay off the loan quickly," says Sudheer.

Fixed versus floating: Interest rates help determine the actual cost of a loan. Lenders offer both fixed and floating rates. But the latter seems more attractive just now as your EMIs could get cheaper due to the external benchmark-linked interest rates which banks have started rolling out for retail borrowers. "The floating rate, which changes based on the changes in market rates, is always welcome as the payment obligation often remains lower compared to a fixed-rate loan. As interest rates are going down, opting for a floating rate makes sense. This will bring down your EMI outgo," says Mehra of Wishfin. In case you are not comfortable with frequently fluctuating interest rates, go for a fixed one, but make sure that the rate is not too high.

@naveenkumar80