Investors need to be cautious of the booming IPO market

")

At 4 pm on Tuesday, October 20, 2015, the rooftop venue at Trident Tower in Nariman Point, Mumbai, was chock-a-block with analysts and marketmen jostling for space at the initial public offering (IPO ) analyst meet of S H Kelkar . Unfortunately, those who happened to form the tail-end of the labyrinthine gathering had to return empty-handed, even without a draft prospectus.

"Everyone is eager to buy a good business and, therefore, there was huge interest among analysts and marketmen," says Anand Ladsariya, an angel and stock market investor who has been investing in the equity market for the past 35 years. "The business is good, but in terms of valuation it's not cheap. Investment bankers have left nothing on the table for investors," he says, adding: "I am not in a hurry to invest in the IPO. I will wait for the price to correct after listing and would buy if the price is between Rs 120 and Rs 140 per share."

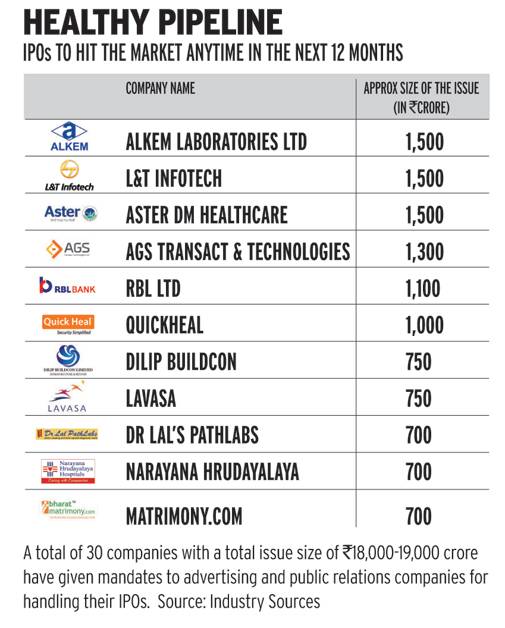

Ladsariya's voice may not reach investment bankers, who, having witnessed huge investor interest in the IPO market almost after five years, are busy bringing the companies to the floor. Says V Jayasankar, Head of Equity Capital Market at Kotak Investment Banking: "After a long time, we are seeing a robust primary market. In fact, in October, Rs 15,000 crore was raised by companies. This shows appetite for good issuances." With over Rs 9,000 crore already raised this year, it has surpassed the collections of the past three years (see Gathering Pace). Secondly, the proportion of offers-for-sale in an IPO has also become larger than new issuances. "Given the current pace of fundraising, the number of issues this year is likely to be around 70, the highest since 2007," says Ashutosh Datar, Economist, India Infoline Institutional Equities (IIFL). S. Subramanian, Head, Investment Bank at Axis Capital, is equally excited: "Investors, especially foreign institutional investors, are looking at India and Indian companies. They are ready to lap up any good business at a good price."

But, caution is the word on the street. Says Datar of IIFL: "Unless there is a convincing and compelling reason to buy a company, investors should stay away from an IPO. More than half of them are trading below their issue prices after one year of listing and two-third are below their issue price, three years after listing." (see Touch Me Not). From an investor's perspective, Datar feels, IPOs suffer from information asymmetry as well as pro-cyclicality. This should, he says, in principle, make IPOs less attractive for investors. Prithvi Haldea, Chairman, Prime Database, agrees: "The two important things retail investors must check are how the institutional book has evolved during the IPO and the behaviour of the existing investor," adding: "If the institutional book is weak and existing investors are selling it completely, then retail investors should stay away from the issue. If there is a complete sell-out from existing shareholders, then it clearly indicates that the growth story is over in the company."