Healthcare discount cards offer savings aside from health cover

Health insurance, usually, covers expenses related to hospitalisation. This means that you will have to pay for other common medical needs such as checkups, diagnostic tests or consultations with a doctor.

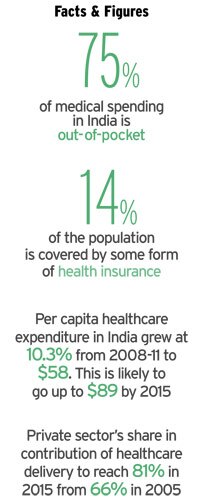

In addition, given that diagnostic and preventive healthcare costs account for 70-75% of medical expenses, covering a family's healthcare needs is expensive. Increasing costs do not help either.

This leaves a gap between what your insurer covers and what you spend on healthcare. Trying to bridge this gap are companies providing healthcare discount cards. They promise between 30-50% discount on diagnostic tests, doctor consultation and even medicine.

What is it?

To offer a comparison, healthcare discount cards are similar to loyalty cards. You pay a membership fee and the company offering the card helps you get discounts on hospitalisation and non-hospitalisation-related expenses.

"We approach the medical fraternity and tell them (that in) whichever area they are operating, we will provide customers," says RK Sharma, business head, Sharak Healthcare, an Escort Group company that provides discount cards. The idea is to offer medical facilities to those who do not have bargaining power at discounted rates, he adds.

Just like insurers, they collaborate with diagnostic centres, hospitals and clinics. Customers with healthcare cards can get discounts at these places, ranging from 10-100% depending on the type of treatment, consultation or test.

Benefits and cost

We checked the plans offered by two, Indian Health Organisation and Sharak Healthcare, healthcare discount card providers.

They offer discounts on care at home, dental care, diagnostic services, cost of medicine, and OPD (out patient department) and doctor consultation fee. In some cases, the discount is extended to treatment that requires hospitalisation and even ambulance charges.

They also offer discounts on 'wellness services', such as diet programs and spa treatments, and alternative treatments such as ayurveda and homeopathy. Both offer a free 'second opinion' before any major surgery. "In India, seeking a second opinion before a surgery is not a must and there are cases where a surgery could have been avoided," says Sharma of Sharak.

The benefits can be availed by individuals, a couple or by a family of up to four members. Extra charges will apply for additional members.

What you should know

Remember the following points when you are looking for a discount card:

Cost-benefit analysis: As simple as it sounds, ensure that the price of the card is not more than the savings that you would make from discounts. If you or someone in your family needs frequent medical help, calculate the average cost you incur and compare with the cost of getting a discount card.

If your medical needs are not frequent, an alternative could be to use the cost of membership to create a health corpus that can be used in case of a medical emergency.

Provider background: Healthcare discount cards are not yet popular in India. So, while there are a couple of established names, most are new. First, check if the company is registered with the Ministry of Corporate Affairs.

Second, check the company's background. This is a specialised service and a company with exposure to the healthcare sector would be a better choice. A company with experience as a TPA (third party administrator) or in healthcare services (hospital, diagnostics) would know the business.

There is no regulator: Remember that these firms are not health insurers. The insurance regulator has no say in these firm's activities. In the absence of a regulator, if you have a complaint, the only recourse is consumer court.

Check the network: Just like health insurers, discount card companies have to collaborate with a lot of hospitals, clinics, diagnostic centres and chemists to be useful to you. So, check their network of service providers. It doesn't make sense for you to travel 15kms to a network hospital to avail a 20% discount on consultation. Cost of travel and the inconvenience should weigh in less than the discount.

The empanelled hospitals and diagnostic centres should also be of repute and not just small nursing homes and pathology labs. If possible, check with the hospitals if they do offer discounts on being a subscriber to a particular healthcare discount card.

What about health insurers?

For long, health insurers have not considered covering outpatient needs. "Due to the small ticket size, insurers have stayed away from OPD and preventive healthcare," says Sanjay Datta, head, underwriting and claims, ICICI Lombard.

However, he says the rising cost of OPD care has provided opportunities for insurance companies. Indeed, some insurers have started covering OPD expenses.

"The health insurance industry is going through a phase of evolution, where we will soon see a gamut of benefits such as medical check-ups, doctor consultation fees and discount on medicines bundled with health insurance plans," says Antony Jacob, CEO, Apollo Munich Health Insurance.

Bajaj Allianz General Insurance is offering policyholders discounts as a value-added service. Discounts are available on medical tests, checkups, doctor consultation and at select dental and eye clinics. It is offered to all existing customers without extra charge.

Abhijeet Ghosh, vertical head- networks and health analytics, Bajaj Allianz General Insurance says research shows that customers feel premium paid is wasted if they don't make a claim in a policy year. "However, customers may use services, such as consultation with specialist doctors, that are not admissible claims under a health plan. So, we pass on the discounts we get from network hospitals."