NPS continues to offer better returns than EPF

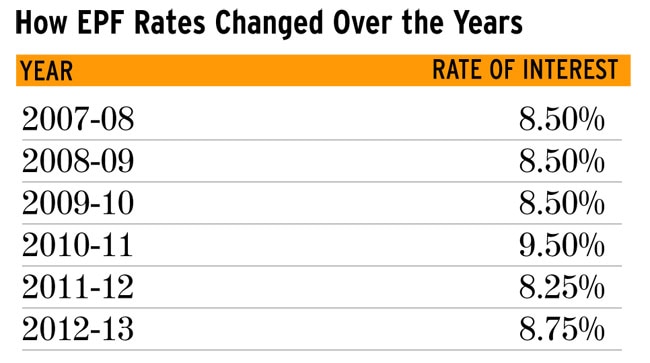

Your employee provident fund will earn 0.25 percentage points higher interest in 2013-14. This after the Central Board of Trustee of the Employee Provident Fund Organisation (EPFO) recommended 8.75% interest rate for the current financial year compared to 8.5% a year ago.

The 8.7% return over the past five year per se looks modest, but given the fact that the interest earned is tax-free and investments up to Rs 1 lakh are eligible for income tax deduction, it is one of the most attractive retirement savings instruments.

For an individual in the 30% tax bracket, the effective yield from EPF (calculated at 8.7% interest) would be 12.6% considering the fact that he can claim tax deduction on his investments.

For the same period (2013-14), the Public Provident Fund (PPF) is offering 8.7%. In 2012-13, PPF gave an annual interest of 8.8%. Like the EPF, interest on PPF is also tax-free and contribution is eligible for income tax deduction up to Rs 1 lakh.

However, returns from the New Pension System (NPS) have been much better than both the EPF and the PPF. In 2012-13, the schemes for central and state government gave a return of 12.39% and 13%, respectively. One of the reasons for high returns generated by NPS is that they are allowed to take exposure to equities, where both EPF and PPF cannot invest.

Despite that financial planners consider EPF as a very good retirement savings option. "A tax-free return of 8% or more a year over a long term will help create a substantial corpus. If you consider the fact that you can also claim tax deduction on EPF contributions, it makes the effective yield even better," says Suresh Sadagopan, a certified financial planner.

Sadagopan says that while the NPS has given better returns, the degree of variability in return will be higher in the NPS compared to the EPF, making it a much safer option.

To understand the importance of the EPF, let us consider an annual contribution of Rs 50,000 for 30 years growing at an average 8% a year. This will help you create a corpus of Rs 61 lakh in 30 years. Meanwhile, in another announcement, the EPFO has increased by 20% the maximum amount received by an EPFO member under the Employee Deposit Linked Insurance (EDLI) plan from Rs 1,30,000 to Rs 1,56,000. Under EDLI, a nominee of an EPFO member gets insurance cover if he/she dies before retirement. The employer contributes 0.5% of basic pay up to Rs 6,500 towards the premium under the EDLI scheme every month.

In another decision, the Board has also decided to increase the minimum charges payable towards administration of EPF accounts from the existing Rs 7 per month to Rs 100 a month for establishment with no contributory members and Rs 700 a month for other establishments.