It is noon, and 48-year-old Shankarbhai Rethalia is a bit tired as he reaches the HDFC Bank branch in Bavla, a village in Gujarat some 35 km from Ahmedabad. He takes off his shoes and enters the air-conditioned branch, some 15 km from his home in Kotha Talawadi, where he owns 50 acres of farmland. He visits the Bavla branch once a week, not just to make transactions but also to seek the advice of the executive who handles his loan portfolio, on how he can earn more on his agriculture proceeds.

Rethalia is not the only privileged customer of the branch. This semi-urban branch counts many traders among its customers. The region has 110 rice processing mills, one of the largest such hubs in the country, well located near the Mundra and Kandla ports. In the Bavla area, there

are seven state-run banks, including State Bank of India, and cooperative banks. Rethalia, who switched loyalties from a cooperative bank, is all praise for the private-sector HDFC Bank, which not only gave him a higher limit on loans, but also structured the loan according to his needs. Eight months ago, Rethalia got a loan of Rs 18 lakh for crop and working capital at an interest rate of around 11.5 to 12 per cent. His previous banker, Ahmedabad Co-operative Bank, gave him a Rs 3-lakh loan at a comparatively lower rate.

Even big traders are switching to HDFC Bank. Gyanshayam Thakkar, a trader who opened Bavla's first supermarket, explains: "Before HDFC Bank, we were dealing with co-operative and state-run banks. The biggest problem with state-run banks was that whenever the manager got transferred, our business would be affected, as the new manager's

style of operation was different. We had to start all over again and build a relationship with them." Last year, Thakkar's turnover was Rs 40 crore. Low interest rates alone are no guarantee of customer loyalty - banks must also offer customised products, higher loan limits, faster processing and good customer service. And private-sector banks have the edge.

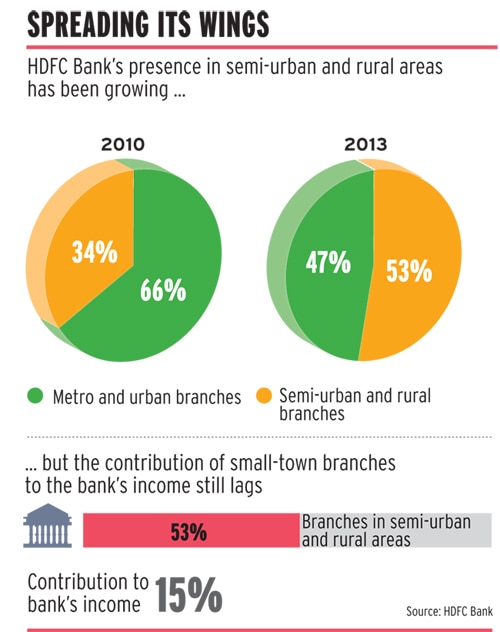

HDFC Bank's five-year-old Bavla branch is reaping the rewards. It's lending more than mobilising deposits. It has deposits of Rs 23.5 crore and assets of Rs 45.5 crore. In semi-urban and rural areas, banks typically lend more and get fewer deposits, as compared to urban branches - a big challenge. But it's also where the growth is: today, every private-sector bank is expanding its footprint in semi-urban and rural areas because the metro and urban markets are saturated. Some 53 per cent of HDFC Bank's 3,251 branches are in semi-urban and rural areas, up from 34 per cent three years ago. The bank aims to raise this number to 60 per cent in the next three years. Ninety per cent of the branches it opened in the last year were in these areas.

Paresh Sukthankar, Executive Director, HDFC Bank, says the branch expansion reflects a

shift from wholesale to retail business. "What we did in 12 to 13 years in urban areas, we are now replicating in semi-urban and rural areas," he adds. The move to smaller towns started five years ago, when the bank acquired the mid-sized Centurion Bank of Punjab. Centurion itself had acquired Lord Krishna Bank, which had a good network in southern India, especially Kerala, and the Bank of Punjab, which had a strong presence in North India.

Playing it right: Aditya Puri, MD, HDFC Bank. PHOTO: Nishikant Gamre

"The acquisition gave us dominant franchises in lot of states, and also a product range that was more suited to rural and interior areas," says

Managing Director Aditya Puri. "We were getting a much smaller balance sheet, but we were getting a large branch network, which at that point was close to 40-50 per cent of our branch network," he says.

But the Centurion acquisition weakened the bank's asset quality, and productivity and efficiency ratio. This is reflected in the fact that after topping Business Today's best banks list for four years running until 2008, it slipped in the rankings. It has taken five years for it to get back to the top.

"If the country grows, we grow," says Puri. "Our hypothesis was that if the economy is growing, it will have a trickle-down effect to rural areas." Given the limited access to organised finance in rural areas, where a large chunk of the population lives, the opportunity is substantial. But there are challenges. "Unlike urban market, the mindset, operations, products, distribution, sales and even back-office have to be different from the urban region," says Puri.

Sukthankar adds that the bank has started offering products such as loans and credit cards to existing and new customers although they are risky. "It's a good way to indulge customers," he says. He emphasises that the bank is not compromising on quality. Today 15 per cent of its income is from rural and semi-urban branches, and the bank believes it can grow to 50 per cent in five years.

Despite concerns about delinquencies in semi-urban and rural areas, experts aren't worried. An analyst from a foreign brokerage said on condition of anonymity: "They are a conservative bank. They don't take rash decisions. They understand a product and market, test it, and then expand."

Prateek Agrawal, Chief Investment Officer at ASK Investments, says: "It has the lowest cost of funds, and maintains high levels of spread without taking much risk, which is why they have low non-performing assets. Its asset-liability mismatch is the lowest in the industry." He adds that the bank has a high return on assets. Greater income generation from fee-based products augur well for the bank, he says, and the bank has a higher return on equity.

Experts say newer products such as gold loans and tractor financing will help improve margins but they don't see income from rural business rising from 15 to 50 per cent in five years. Puri, however, appears confident of achieving his target. "These are virgin markets," he says. "Penetration is still low. It's not easy terrain - every market has to be tackled differently. We have learnt the hard way, and have worked hard to achieve some success."

Semi-urban and rural operations are about more than money: there are financial inclusion and other issues. For example, the bank formed a self-help group in Bavla and gave Kanchanben Kolipatel and Bhavanaben Thakor - both local women in their thirties - Rs 17,500 each to start their own business. Thakor, who makes nearly Rs 400 a day selling cutlery, has helped her husband buy a Mahindra truck, and their children go to school. Kolipatel earns Rs 200 a day selling saris, and helped her husband buy an autorickshaw.

Small-town banking offers both potential and challenges, and perhaps the biggest challenge is giving the human touch to service in these markets. So far, HDFC Bank has got it right.

(Follow the author on Twitter: @MaheshNayak)