IT shares: BNP Paribas highlighted that the domestic IT services sector is trading at a dividend yield of 3.2 per cent — close to its highest level in the past decade.

IT shares: BNP Paribas highlighted that the domestic IT services sector is trading at a dividend yield of 3.2 per cent — close to its highest level in the past decade.  IT shares: BNP Paribas highlighted that the domestic IT services sector is trading at a dividend yield of 3.2 per cent — close to its highest level in the past decade.

IT shares: BNP Paribas highlighted that the domestic IT services sector is trading at a dividend yield of 3.2 per cent — close to its highest level in the past decade. Investor sentiment towards the IT sector remains overly bearish, with foreign institutional investor (FII) holding in IT services near a 13-year low. Domestic institutional investor (DII) ownership has also declined sharply in recent months. Historically, BNP Paribas noted, such low ownership levels have often served as a catalyst for the sector’s outperformance.

BNP Paribas highlighted that the domestic IT services sector is trading at a dividend yield of 3.2 per cent — close to its highest level in the past decade — providing downside protection to valuations. It added that management commentary, deal wins, and lateral hiring data suggest that the demand environment has remained largely steady in recent months.

“Our global economists believe that while the US economy may slow in 2025–26, it is expected to avoid a recession. Also, Accenture’s Q4FY25 guidance, issued at the upper end of its range, implies a recovery in organic growth. Management noted an improvement in pricing, with client discussions moving from a ‘pause’ to ‘focus’ and even ‘leapfrog’ initiatives,” BNP Paribas said.

While near-term risks from any escalation in trade tensions remain, the brokerage believes that excessively bearish sentiment toward Indian IT services — as reflected in investor ownership rather than prices — more than prices in such risks.

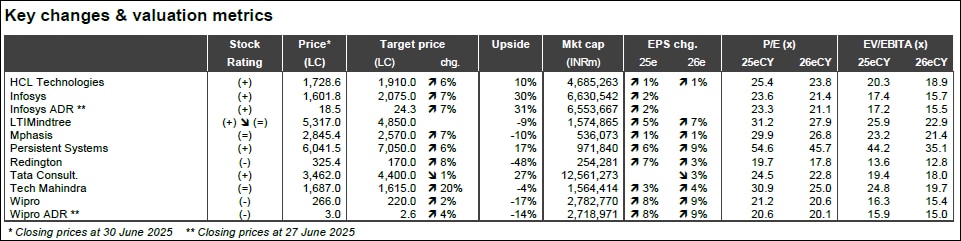

“We add Infosys to our list of top large-cap picks, alongside TCS. Persistent Systems remains our preferred mid-cap pick. We also like HCL Technologies. We downgrade LTIMindtree to Neutral following the recent run-up. We remain cautious on Tech Mahindra and Mphasis, and see significant underperformance risk in Wipro,” it said.

For the June quarter, BNP Paribas expects seasonality-led divergence across the Tier I IT pack, with strong numbers from Infosys and Persistent Systems, and weaker results from Wipro and TCS.

“For our large-cap coverage, we expect Q1FY26 quarter-on-quarter (QoQ) constant currency (CC) organic revenue growth between -1 per cent and -2.5 per cent, as companies face project ramp-downs and seasonal headwinds. Infosys is expected to outperform, with 2.1 per cent CC growth. Among mid-caps, we forecast 1 per cent to approximately 4 per cent QoQ dollar organic revenue growth,” it said.

The brokerage expects EBIT margins to remain flattish or decline for large caps, while mid-caps are likely to see improvement on account of operational efficiencies and currency tailwinds.

“We expect Infosys to narrow its guidance to 1.5–3.5 per cent and HCL Tech to retain its 2–5 per cent FY26 year-on-year (YoY) CC revenue growth guidance. We see Wipro guiding for -1 per cent to +1 per cent QoQ CC revenue growth in Q2FY26,” it added.

Management commentary is expected to remain broadly unchanged from the previous quarter — blending caution with optimism on execution.

‘Absolutely no compromise on agriculture, dairy, sugar’: Piyush Goyal on India-US trade deal

‘Absolutely no compromise on agriculture, dairy, sugar’: Piyush Goyal on India-US trade deal operations") Exclusive: Adani Group to start coal gasification work this year, expand MRO operations, says Jeet Adani

Exclusive: Adani Group to start coal gasification work this year, expand MRO operations, says Jeet Adani Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why

Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why Shipping Corp shares zoom 14% on Q3 earnings, dividend; check details

Shipping Corp shares zoom 14% on Q3 earnings, dividend; check details  Elon Musk shifts SpaceX focus to ‘self-growing’ Moon city over Mars colony

Elon Musk shifts SpaceX focus to ‘self-growing’ Moon city over Mars colony India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers

India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China

US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China “India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal

“India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted

Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political Firestorm

Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political Firestorm Zerodha's new 'Terminal Mode' on Kite trading platform: How it proposes to change user experience

Zerodha's new 'Terminal Mode' on Kite trading platform: How it proposes to change user experience  FIIs turn buyers in February so far: Temporary bounce or start of a new trend?Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's whyShipping Corp shares zoom 14% on Q3 earnings, dividend; check details

FIIs turn buyers in February so far: Temporary bounce or start of a new trend?Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's whyShipping Corp shares zoom 14% on Q3 earnings, dividend; check details  YES Bank shares snap two-day fall; analysts advise caution on near-term outlook

YES Bank shares snap two-day fall; analysts advise caution on near-term outlook