For Shriram Finance, Nomura India has a target of Rs 2,900 is based on 2 times FY25F book. Risks included a slower than expected loan growth, asset quality issues from riskier segments such as personal loans, two-wheeler and MSME.

For Shriram Finance, Nomura India has a target of Rs 2,900 is based on 2 times FY25F book. Risks included a slower than expected loan growth, asset quality issues from riskier segments such as personal loans, two-wheeler and MSME. For Shriram Finance, Nomura India has a target of Rs 2,900 is based on 2 times FY25F book. Risks included a slower than expected loan growth, asset quality issues from riskier segments such as personal loans, two-wheeler and MSME.

For Shriram Finance, Nomura India has a target of Rs 2,900 is based on 2 times FY25F book. Risks included a slower than expected loan growth, asset quality issues from riskier segments such as personal loans, two-wheeler and MSME.It has reiterated its cautious stance on non-bank financial companies (NBFCs), especially small and mid-tier NBFCs, going into FY25 due to various compliance-related regulatory actions being taken in recent times, potential slowdown in unsecured loans (25-30 per cent of incremental loan growth from unsecured during FY22-3Q24), elevated competition from banks in secured segments, elevated cost of funds, and normalisation of credit cost amid multi-year low provisioning levels for various NBFCs.

Nomura India said the cost of funds should remain elevated for most part of FY25 due to a potential increase in rates at which banks lend to NBFCs post the RBI increasing the risk weights on these loans, a potential rise in corporate/NBFCs yields after the RBI announcement on risk weights as NBFCs rushed to the corporate bond market for funding and lower probability of a repo rate cut in H1FY25.

Nomura India said even if the rate cut happens in late FY25, the positive impact on cost of funds for NBFCs would be visible only in 1HFY26F. A lower growth in unsecured loans would be margin-dilutive, it said adding that the elevated competition in secured segments would make the yield competitive as well.

Assuming a rate cut will take place by the end of FY25, SBI Cards would be the one with the maximum positive impact, and LIC Housing Finance the lowest in FY26. Within other NBFCs, Bajaj Finance and Cholamandalam Investment & Finance Company Ltd would be the least positively impacted due to rate cuts.

Nomura India prefers Shriram Finance - a play on used vehicles; and Five-Star - a play on secured micro SMEs, in the NBFC space.

"In other unsecured loans (consumer durable/credit cards), NBFCs are losing market share to banks due to elevated competitive intensity. Even in secured segments like auto/home, NBFCs are losing market share to banks due to elevated competitive intensity. Further, in auto, volume growth should moderate in coming years with which disbursements growth of various auto NBFCs are highly correlated," it noted.

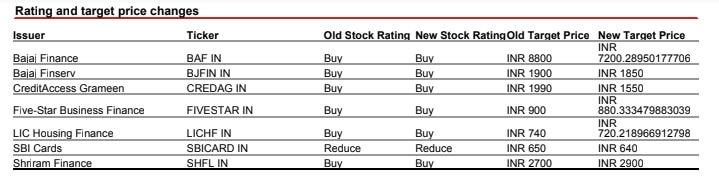

Nomura India values Bajaj Finance at Rs 7,200 per share using Residual Income model, implying 4.8 times FY25F BVPS.

Risks that may impede the achievement of the target price include a potential stress in personal loan portfolio, lower than expected AUM growth and structural challenges, like bank conversion and listing of Bajaj Housing Finance remain key downside risks.

In the case of Bajaj Finserv, the brokerage sees the stock at Rs 1,850. In Insurance, inability to improve margins in life insurance and growth in general business remain the key risk.

For CreditAccess Grameen, the target price is Rs 1,550 based on a residual income model, which implies 3 times FY25 book multiple. Risks include a slowdown in economy, especially in rural areas leading to growth slowdown and/or asset quality deterioration and Inability to scale up in new states remain the key downside risks

For Five-Star Business Finance, Nomura India has a target of Rs 880 based on a residual income model, valuing it at 4.2 times FY25F BVPS. Key risks include inability to scale up growth in core or new geographies, deterioration in asset quality and competition from banks and NBFCs

For LIC Housing Finance, the target is Rs 720. Key downside risks included continued underperformance on asset quality and adverse/weak macros. For SBI Cards, the target is Rs 640 based on a residual income model, valuing it at 4.1 times

FY25F BVPS. Key things to watch will be higher than expected pick up in revolver portion while maintaining pristine asset quality; reduction in competitive intensity driving higher growth and margins and positive regulations around MDR in terms of no cap on it.

For Shriram Finance, Nomura India has a target of Rs 2,900 is based on 2 times FY25F book. Risks included a slower than expected loan growth, asset quality issues from riskier segments such as personal loans, two-wheeler and MSME.

FIIs turn buyers in February so far: Temporary bounce or start of a new trend?

FIIs turn buyers in February so far: Temporary bounce or start of a new trend? RIL, IREDA, GRSE, United Breweries & Bharat Forge shares: Nilesh Jain of Centrum Broking weighs in

RIL, IREDA, GRSE, United Breweries & Bharat Forge shares: Nilesh Jain of Centrum Broking weighs in 2 million barrels deal: Indian Oil Corp, HPCL buy Venezuelan Merey crude for April

2 million barrels deal: Indian Oil Corp, HPCL buy Venezuelan Merey crude for April Varun Beverages shares under bear attack, oversold on charts; what lies ahead?

Varun Beverages shares under bear attack, oversold on charts; what lies ahead? 1,370 litres of milk destroyed: Gujarat plant raided for making milk with detergent, urea

1,370 litres of milk destroyed: Gujarat plant raided for making milk with detergent, urea India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers

India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China

US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China “India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal

“India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted

Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political FirestormRIL, IREDA, GRSE, United Breweries & Bharat Forge shares: Nilesh Jain of Centrum Broking weighs inVarun Beverages shares under bear attack, oversold on charts; what lies ahead?

Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political FirestormRIL, IREDA, GRSE, United Breweries & Bharat Forge shares: Nilesh Jain of Centrum Broking weighs inVarun Beverages shares under bear attack, oversold on charts; what lies ahead? Zerodha launches new 'Terminal Mode' in beta version: How it proposes to change user experienceFIIs turn buyers in February so far: Temporary bounce or start of a new trend?

Zerodha launches new 'Terminal Mode' in beta version: How it proposes to change user experienceFIIs turn buyers in February so far: Temporary bounce or start of a new trend? Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why

Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why