This newly introduced uniform LTCG tax rate of 12.5% replaces the previously existing varied tax rates that were applied to different asset classes.This newly introduced uniform LTCG tax rate of 12.5% replaces the previously existing varied tax rates that were applied to different asset classes.

This newly introduced uniform LTCG tax rate of 12.5% replaces the previously existing varied tax rates that were applied to different asset classes.This newly introduced uniform LTCG tax rate of 12.5% replaces the previously existing varied tax rates that were applied to different asset classes.Budget impact: In the Union Budget 2024, the Centre has made noteworthy adjustment regarding the treatment of long-term capital gains (LTCG) in property transactions. Specifically, the indexation benefit has been eliminated, resulting in substantial modifications to the LTCG calculation.

Despite this change, it has been affirmed by the government that properties purchased or inherited prior to the year 2001 will continue to enjoy the indexation benefit, even as the LTCG tax rate has been lowered from 20% to 12.5%.

Furthermore, the government has explicitly stated that properties acquired before the year 2001 will retain the privilege of receiving indexation benefits upon their sale.

A report by BankBazaar has indicated that property owners may experience a considerable rise in long-term capital gains (LTCG) tax obligations following the implementation of the new regulations. This apprehension stems from the elimination of indexation benefits in the Union Budget 2024. Consequently, there is a possibility that tax liabilities could escalate by as much as 290% for properties acquired post-2010.

Indexation is a process that involves adjusting the original purchase price of an asset, such as real estate, to reflect the impact of inflation over a period of time. This adjustment is implemented to mitigate the effects of inflation on the asset's value, thereby resulting in a more accurate calculation of the taxable capital gains upon the sale of the property.

Historically, the adjustment to manage tax burdens for property owners has been a significant practice. However, Finance Minister Sitharaman's recent announcement regarding the introduction of a new flat Long-Term Capital Gains (LTCG) tax rate of 12.5% has sparked concerns within the financial community.

This newly introduced uniform LTCG tax rate of 12.5% replaces the previously existing varied tax rates that were applied to different asset classes. For example, equities were subjected to a 10% LTCG tax rate, whereas non-financial assets such as real estate and gold were taxed at a higher rate of 20% for LTCG.

It is important to highlight that the Finance Ministry has clarified that the decision to eliminate the indexation benefit for property sales was not primarily aimed at generating additional revenue. Furthermore, the Ministry has assured that this new capital gains tax regime will not result in an increased tax burden on real estate transactions.

What does the BankBazaar report say

The report delved into the tax implications associated with property sales under two scenarios - with and without indexation, across various holding periods and property values. The key observations from the report are as follows:

> Substantial Tax Increases: The report highlights that the Long-Term Capital Gains (LTCG) tax incurred without indexation has surged remarkably by 290% in comparison to the tax burden imposed with indexation.

> Longer Holding Periods, Higher Taxes: Properties that were held for extended durations experienced more substantial escalations in tax obligations. In some instances, the tax liability surged by an alarming rate of up to 500%.

> Regional Disparities: While the tax impact is discernible across a broad spectrum, specific urban centers such as Mumbai and Kolkata have encountered pronounced tax burdens. Taxpayers in these cities have been particularly affected by exceptionally elevated tax liabilities.

The decision to eliminate indexation and implement a uniform 12.5% tax rate on LTCG has significantly diminished the advantages associated with holding onto properties for extended periods. This alteration is anticipated to impact investor confidence within the real estate industry, potentially leading to a decrease in the inclination to hold properties for the long term.

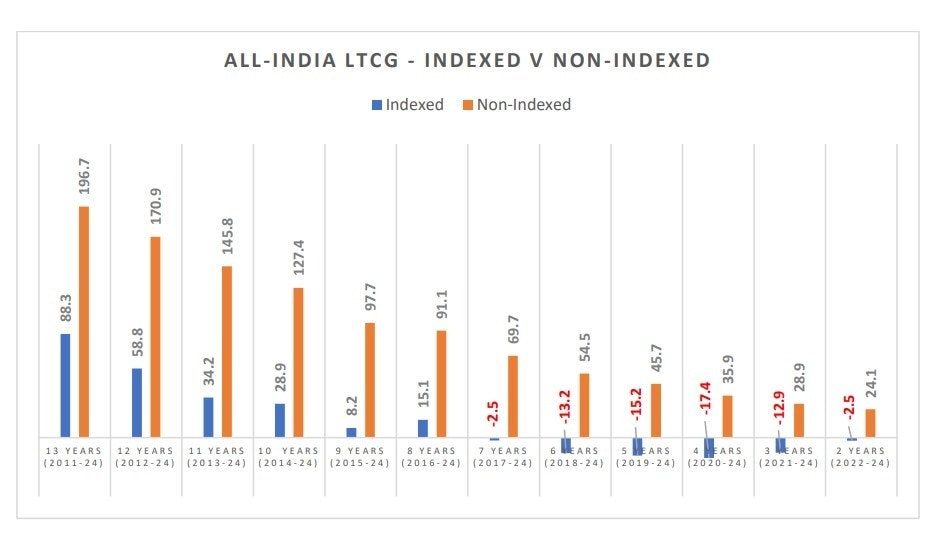

> The average indexed tax on LTCG in these 13 years is 3.90.

> This average non-indexed tax rises 2.90 times to 11.34, implying additional taxes of 7.44.

> Similarly, the median tax rises 12.10 times from 0.83 to 10.05.

> The actual simulated taxes for all periods will be larger post the updated HPI values for Q2-2024-25 and Q3-2024-25.

> Short-term holdings: All taxes with indexation were 0.00 from 2016-17. Without indexation, the taxes rise significantly with values of 3.02 to 8.70.

Adhil Shetty, CEO of BankBazaar, remarked, “The removal of indexation benefits significantly alters the financial landscape for property investors. While simplification of tax rates is a positive step, it is crucial to consider the impact on returns, especially for long-term investors.”

City-level findings

> Mumbai has the highest average additional tax at 7.02.

> Kolkata is next at 6.71. The city sees a 500x jump in applicable taxes for properties purchased in 2014-15, and 106x increase for properties purchased in 2017-18 – the two highest such values in the study.

> Delhi and Jaipur, with largely 0.00 tax with indexation, now have higher taxes with the new rules

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market.") Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma

Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs

India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’, MRF, Hero MotoCorp, Mazagon Dock Shipbuilders and Power Grid Corporation of India, among others.") BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook

RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.”

Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.” Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation

Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact

RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates

Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates 'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag

'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag Bitcoin avoids $60,000 breakdown, still down over 50% from record high

Bitcoin avoids $60,000 breakdown, still down over 50% from record high