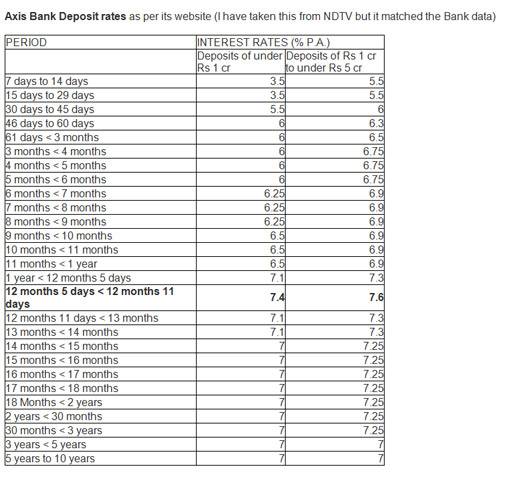

Axis bank, India's third largest private sector bank, has just introduced a new fixed deposit tenure of 12 months 5 days to under 12 months 11 days, which will earn interest at the rate of 7.4 per cent for deposits under Rs 1 crore. Deposits of Rs 1 crore to less than Rs 5 crore will earn an even more attractive 7.60 per cent. This is currently the highest interest rate that Axis Bank is offering across all available tenures (see table).

This development comes just days after country's largest lender, State Bank of India, hiked its term deposit rates on retail deposits below Rs 1 crore by up to 25 basis points. Now deposits for 1 year to 2 years will now accrue 6.65 per cent as against 6.40 per cent earlier. For the senior citizens, the new rate is 7.15 per cent from 6.90 per cent earlier. For the investments from 2 years to 3 years, the interest rate is revised to 6.65 per cent from 6.60 per cent.

There is no change in interest rate for deposits less than one year. Currently, the banks gives 5.75 per cent for deposits under 7 days to 45 days scheme. For 46 days to 179 days, the interest rate is 6.25 per cent with no change. For investment under 211 days to less than year, the rate is fixed at 6.40 per cent. In all these schemes, senior citizens get 50 basis points higher than their non-senior citizen customers. This is the second time in just three months the largest lender has raised the rates for term deposits. Earlier in February, the SBI had hiked interest rates on its retail deposits - those below Rs 1 crore - by 10-50 basis points.

Then, in April, HDFC Bank too raised interest rates for deposits by up to 100 basis points in a bid to grow its deposits. For deposits maturing between two years and five years, the rate was hiked by 100 bps to 7 per cent, while deposits with maturity of one year and 17 days to two years has been raised by 75 bps to 7 per cent.

This is a clear sign that system-level liquidity, which had spiked courtesy demonetisation, has moved towards neutrality. Late last year, banks started hiking interest rates on bulk term deposit rates before moving on to retail term deposits. With banks' credit growth recovering, banks need funds now and hence more banks are likely to follow suit in making fixed deposits more attractive.

According to a statement by the RBI yesterday, "The pick-up in credit growth during 2017-18 helped in improving the credit-deposit ratio to 75.6 per cent at end-March 2018 from 73.7 per cent a year ago". The apex bank added that during the March quarter, the private sector bank group recorded the highest credit growth both on sequential as well as on an annual basis. Although RBI data shows that the credit-deposit ratio slipped slightly to 74.66 per cent in April, last month it again climbed up to 75.06 per cent.

The bad news is that a hike in deposit rates is typically followed by an uptick in lending rates. It's started already. According to media reports, SBI has just hiked its effective Marginal Cost of Lending Rate (MCLR) by 0.10 per cent across all tenures with immediate effect. Punjab National Bank similarly revised its lending rates upwards by 0.05-0.10 percent, effective today. So expect costlier loans here on.

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal 'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got

'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got Cyberattack impact on Tata Motors PV earnings crosses Rs 3,200 crore; losses still mounting

Cyberattack impact on Tata Motors PV earnings crosses Rs 3,200 crore; losses still mounting 'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market.") Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma

Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook

RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.”

Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.” Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation

Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact

RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount Loss

TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount Loss IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates

Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates 'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag

'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag Bitcoin avoids $60,000 breakdown, still down over 50% from record high

Bitcoin avoids $60,000 breakdown, still down over 50% from record high