On the 10th of every month, State Bank of India's headquarters at Nariman Point in South Mumbai plays host to some eager guests. Heads of several of India's 15 asset reconstruction companies (ARCs) make a beeline to review the 'for sale' bad loans that India's largest bank would be willing to hawk for a price. A similar exercise takes place at some of India's largest banks, though not necessarily with such regularity.

Under Rajan's stewardship, the RBI has announced a host of measures that have fuelled distressed asset sale business. Early last year, the central bank allowed the banks to sell even the loans where the principal or interest was overdue by 60 days rather than 90 days, earlier. In essence, it allowed banks to start selling assets early if they felt the loan was non-redeemable. Other factors are also responsible. ARCs are betting heavily on the proposed new bankruptcy law which will give them a greater leeway (including sale of whole or part of the company and change of management or promoter) to revive the distressed assets. Four, in general, the industry believes that the Indian economy has seen through the worst of the slowdown and things can only look up from here. And, those who have the cash are happy to buy distressed assets since they come at a significant discount to an identical greenfield project.

For over 10 years, it was only ARCIL, backed by SBI and ICICI, which was active in buying loans from its sponsor banks. But a majority of new ARCs have been set up after 2008/09. Among the newest, Edelweiss ARC which was set up in 2009, has worked up a portfolio of over Rs 20,000 crore. At the second spot is ARCIL with a portfolio of Rs 11,000 crore. The top five ARCs make for nearly 90 per cent of the accounts under management. Essentially, that means the ARC takes over the asset, or company, and tries to revive it by managing it better, instead of trying to recover money by selling off parts of it. Not everybody is chasing assets under management (AUMs) though. "We look at it as an investment business. We are not in the AUM game," grins Eshwar Karra, CEO of Phoenix ARC, Kotak Group, formed in 2004. Karra deals with only sub-Rs100-crore loans, with a focus on turning around the companies and sold quickly instead of volumes

The big reason why ARCs remain enthusiastic is because sale of bad loans will only intensify. Banks, after all, are sitting on a pile of bad debts. Of the Rs 70 lakh crore that the banking system has given in advances, nearly Rs 7.7 lakh crore is believed to be classified as 'stressed assets' that have defaulted on their payments. Of this, Rs3.1 lakh crore is already defined as gross NPAs on which there has been a default. A lot of that is likely to be made available to ARCs for sale. So, while the banks are being pushed by the regulator to clean up their books, ARCs see an opportunity of making big bucks like their counterpart asset management companies (AMCs) and hedge funds in the US.

A Hard Job

Despite the enthusiasm around distressed assets, it is not a job for the faint hearted.

Take the case of Bharati Shipyard. A year after Edelweiss ARC bought Bharati Shipyard's Rs 4,570 crore loan from 12 of its 23 bankers, there awaited a surprise. As many as nine winding up petitions appeared out of the blue in the Bombay High Court thwarting the attempts of Edelweiss to turn around the cash-strapped ship building firm. Surprisingly, insurance giant Life Insurance Corporation (LIC) was also one of the petitioners despite being a secured creditor.

Yet, Edelweiss group chairman and CEO Rashesh Shah remains bullish. Shah, who began his career with the ICICI group when it was still a development finance institution and had not turned into a bank, believes he knows how to deal with stressed assets. "Very often a distressed company is still viable, but it is just that it is indebted," says Shah.

Sitting at the Edelweiss House in a Mumbai suburb, Antony is strategising to push the Bharati Shipyard winding up petition out of his way. Bharati has promised to repay the unsecured creditors in 12-15 months. Antony has also engaged with Bharati Shipyard's promoters PC Kapoor and Vijay Kumar, and other lending banks which did not sell their loans.

Any setbacks, such as that of Bharati's, haven't deterred top ARCs from buying big. ARCIL, the oldest ARC, bought another whopper of a deal in April this year. It acquired the Rs 3,000 crore bad loans of Corporate Power, a company belonging to Nagpur-based Abhijeet Group.

There are success stories too. Edelweiss claims to put Electrotherm (India), a leader in induction furnace, on a revival path. Edelweiss bought Rs 1,500 crore of the Rs 3,400 crore debt from over half-a-dozen banks. "We converted a part of the debt into equity," says Antony, whose ARC now holds a 10 per cent stake in the unit. Today, Electrotherm, which has been a loss-making unit since March 2012, has seen its revenues jump from Rs 659 crore in 2013/14 to Rs1,829 crore in 2014/15. "I have to ensure 18 per cent IRR (internal rate of return) otherwise there is no business in the bad assets," says Antony.

Bankers' Dilemma

The sale of large NPAs, such as Bharati and Corporate Power, indicate a clear change in the banks' approach towards selling bad loans.

Earlier, banks sold only the written-off bad loans which were practically dead assets. They also sought a high price. Now, with the RBI on their case, banks are in a bind, even as there is no respite from bad loans. For public sector unit (PSU) banks, the government has stopped liberal funding of capital every year. The only option now is to generate cash by selling bad loans to ARCs.

Take for instance the case of SBI, which sold the biggest chunk of bad loans of around Rs 12,000 crore in its history in 2014/15. "This has helped us to clean our balance sheet. The transfer to ARC will also generate some return for us in the future," hopes Malhotra. This is true for the banking sector at large. ARCs, says SBI, remains the most pro-active. In fact, it has made sale of bad assets like an assembly line activity. The bank's monthly sale of NPAs (quarterly earlier) say a lot about SBI's seriousness to clean the books. "We have substantially improved our information inputs to ARCs," says Malhotra. SBI allows three weeks to ARCs to do their due diligence before accepting the bids. (See SBI's Sale To ARCs).

Undoubtedly, the big shift in SBI's approach is the sale of fresh NPAs, such as the Hotel Leela-venture exposure of Rs 4,200 crore. It was put up for sale within three months of declaring it as an NPA. The sale to JM Financial ARC, however, came as a big surprise to the promoters of the luxury hotel chain. The bank reasons that there was no hope of generating cash in the next four to five years.

Patron RBI

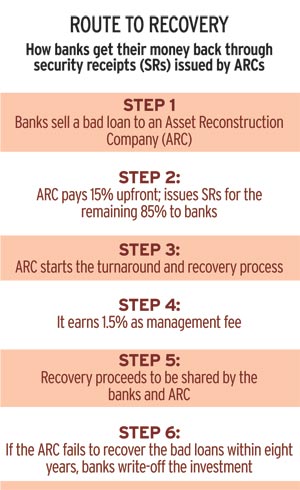

In the past 18 months, the RBI has introduced a slew of reforms, including hiking the initial investment by ARCs from 5 per cent of the acquisition amount to 15 per cent, to discourage ARCs from relying heavily on the management fee model for their survival.

In the 5:95 model, ARCs used to buy a bad loan at a discount from banks' book value by paying just 5 per cent upfront in cash, while the balance was in the form of security receipts issued by them. ARCs also get a management fee of 1.5 per cent every year on the overall AUM they manage. In the 5:95 scenario, ARCs were content playing the management fee model because on an investment of Rs 5 (on a Rs 100 loan), they were earning Rs 1.5, which meant a 30 per cent rate of return on the investment of Rs 5 (see Route To Recovery).

Ever since the RBI mandated the cash composition to 15 per cent (15:85 model) in August last year, ARCs have a greater stake in moving from the 'management fee' model to the 'investment model' as the 1.5 per cent management fee only amounts to 10 per cent rate of return on a cash investment of 15 per cent. This gives the ARCs more of an incentive to actually turn around the company and make it profitable, instead of just passively earning profits through management fees. It also ensures that they work harder.

ARCs have no magic wand to revive a sick unit. They mostly use the bilateral route by working alongside the promoter to de-leverage the business. "We are financial restructuring specialists. We are not business restructuring experts," says Eshwar Karra, CEO of Phoenix ARC. Players like ARCIL and Edelweiss are playing in big loans where dozens of banks are involved. Loan aggregation is a huge challenge and the resolution strategy centres around restructuring of loans to revive a unit.

Three months ago, JM had put out an advertisement for the sale of Hotel Leela's Chennai and Goa properties to reduce the debt burden. "They are yet to zero in on the sale. In this difficult environment selling a large hotel property is very difficult," says a banker. In May this year, the company decided to mobilise Rs 1,000 crore through equity or debt. "Ultimately, Hotel Leela will be a strategic sale to a big hotel chain," says a rival ARC official. JM Financial refused to participate in the story.

Edelweiss ARC, on its part, is arranging Rs 600 crore from high networth individuals (HNIs) to complete its order for delivering a couple of ships to Bharati Shipyard. Unlike banks, Edelweiss ARC has the flexibility to reduce the interest rates drastically, whereas banks cannot lend below their base rates. Similarly, Edelweiss could convert part of Bharati's debt into equity, whereas such decisions by banks would come under scrutiny. ARCs actually have no such worries. "Our short-term plan is to revive the company in 24-30 months," says Antony. There are some who say new investors (generally private equity) demand priority over existing lenders as they are taking a bigger risk. "This preference is not acceptable to those banks who have not sold their loans," says a market observer.

While ARCs try to identify and take only those assets which can be made viable, it does not always play out that way. The oldest, ARCIL finally got the Corporate Power loan at a hefty discount, but the entire economics of the project has now turned on its head. The coal mine was re-auctioned recently to another player. Now, the coal mine advantage does not exist any more. Another big negative is the location of the unfinished plant. The Corporate Power plant is in Chandwa in Latehar district of Jharkhand, which is a Naxalite-affected region. "We are working towards a resolution. We have to finish it. We have to get coal linkages. We have to also get the power purchase agreement (PPA) revised," says an official of ARCIL.

"Banks generally have factory buildings or land as security, but what about the other assets in a business which are not subject to security, such as business licenses, contracts, customers, employees, etc.? How do you transfer these assets under SARFAESI? There is a big hurdle in transferring the continuity of the business," says Haigreve Khaitan, Partner at Khaitan & Company.

In cases where an ARC decides to opt for the asset-stripping route without the consent of the promoters, there is lot of resistance. ARCIL has struggled to sell Tulip Star Hotel (erstwhile Centaur near Mumbai's Juhu beach) for many years. The company has successfully challenged the SARFAESI notice of ARCIL in the past. Board for Industrial and Financial Reconstruction (BIFR) is yet another escape route where, after the failure of a corporate debt restructuring (CDR), promoters can immediately approach the board. "Once you take a SARFAESI action, BIFR action gets abated. But practically, it doesn't happen," admits an ARC official.

Bankers hold a grudge against ARCs that they are unable to turn around the stressed assets despite a lot of flexibility in restructuring a loan. "ARCs have limited financial muscle, which leaves little scope for revival," says the head of a PSU bank. ARCs have spent barely Rs 3,400 crore to acquire total assets of Rs 1.89 lakh crore of book value till date. If all the NPAs do find themselves in the market, that's another Rs 3.10 lakh crore which require at least Rs 22,500 crore of capital from ARCs by the 15:85 principle. That's the kind of money ARCs do not have today because of various reasons: they are not allowed to go public for now and there is no secondary market for security receipts.

There are some who suggest that the ARC game play has changed with a higher initial contribution at 15 per cent for them. "This requires an integrated approach (involving) support from PE firms, distressed funds and turnaround specialists, among others," says Hari Hara Mishra of a Delhi-based ARC.

"There have been a couple of transactions in the recent past where foreign institutions were interested in ARCs. For example, KKR showed interest in International Asset Reconstruction Company (IARC) and Hong Kong-based SSG Capital in Delhi-based ACRE. For global players, investing in ARCs enable them to take an exposure in the growing distressed market and, this may prove to be a win-win for both. "These global investors provide transfer of technical knowledge, information and capabilities, which is going to equip ARCs to handle complex cases. This will also provide access to global network in terms of investments and industry knowledge," says Munesh Khanna, Partner (Corporate Finance) at PWC.

"Foreign capital must come here because ARCs are starved of capital. The track record of ARCs has been abysmal in terms of return on equity," says Vinayak Bhuguna, CEO and Managing Director of ARCIL. The return on equity is barely double digit. So the performance has to go up to attract foreign capital. Currently, the capacity of ARCs to take up more fresh bad loans is also limited because of their low capital base. According to a report on ARC business in India by turnaround specialist Alvarez & Marsal, the current capitalisation of all ARCs put together is around Rs 3,000 crore. "With the cash component increased to 15 per cent of acquisition, the net worth of ARCs would be sufficient to acquire only Rs20,000 crore of stressed assets. Assuming ARCs acquire the NPAs at a discounted norm of 60 per cent of the book value, all ARCs put together can garner Rs 33,300 crore of NPAs," says the report.

More Gaps to Plug

Either way, there's miles to go before ARCs have sound sleep. One of their biggest bugbear is that banks do not follow a consortium approach of selling and, therefore, ARCs have to resort to a time-consuming process of dealing with each bank separately. Bharati and Hotel Leela are good examples of the consortium approach where SBI took a lead, but in most cases, ARCs have to run after individual banks. This process could take as much as 6-12 months. "Big banks like SBI and ICICI, which are in big loans, can take a lead in bringing together all lending banks in a defaulting company," says an ARC official.

Raman Singh of Bank of India, who deals in stressed assets, says ARCs' track record shows a recovery of 10-12 per cent of the book value and 50 per cent of the acquisition cost. This indicates half the SRs are as good as junk.

{mosimage}The outstanding SRs currently stand at close to Rs 50,000 crore. And, more will get added along the way. If ARCs succeed, banks will also get their money, which is the objective of promoting specialised ARCs to recover bad loans in the economy. But if they fail to recover loans, it's merely a book entry of transfer of a junk asset from a bank to an ARC. It is in the interest of everybody- the government, the banks, the legal system and the ARCs - to make the system work so that the NPA monster can be tamed.