In the corporate world, there is a strong buzz about paperless offices. Governments, too, are betting big on e-governance. Yet, of late, health insurance paperwork has increased, a big area of concern for policyholders to whom the language of

.

(Irda) has stepped in. Its new guidelines, which take effect from July 1, will make the fine-print of health policies bolder and terms and conditions clearer.

The first, and perhaps the most important, thing Irda has done is clearly define 46 common terms and 11 critical illness procedures. At present, insurers define these in their own way, so much so that there is no clarity on even what constitutes a heart attack or a pre-existing disease. This will change now.

It has also listed permanent exclusions for hospital plans, made the claims process simpler and mandated a standard agreement between third-party administrators (TPAs), insurers and hospitals for faster claim settlement.

with the terms and conditions. The policies will also come with information sheets so that customers understand whatever information is given to them.

Though the July 1 deadline is for group plans (for retail plans it is October 1), insurers have started re-writing policies for retail customers as well.

Irda's aim is to bring transparency to a product that is among the fastest-growing in a rapidlyexpanding industry. "The segment has numerous companies and products. This necessitates maintenance of some parity. The customer must not feel perplexed and should be able to take well-informed decisions," says Antony Jacob, chief executive officer, Apollo Munich Health Insurance.

"This has become particularly important after the introduction of health insurance portability where customers are faced with the difficult task of comparing the terms and conditions of various policies while taking a decision to switch their insurer," says Subrahmanyam B, senior vice president & head, Health, Commercial Lines & Reinsurance, Bharti AXA General Insurance.

PRE-EXISTING DISEASE

Any condition for which you had signs or symptoms and/or were diagnosed and/or received medical advice/treatment within 48 months before the issuance of the first policy.

Standard DefinitionsOpaqueness in policy terms and conditions makes customers unhappy. Johnson Furtado, a resident of Mumbai, was hoping that his corporate health plan would cover all the expenses when his wife went for Laproscopic Hysterectomy, a surgical procedure to remove the uterus. The TPA passed the claim, but an amount of Rs 25,000, rental for equipment used in the surgery, was not paid; the TPA said Furtado's policy did not cover equipment rentals.

This was a wrong interpretation of the policy terms and conditions, something that standardisation would have avoided. This is because Irda has now clearly defined medical expenses as "expenses that an insured has … incurred for medical treatment on account of illness or accident on the advice of a medical practitioner, as long as these are no more than would have been payable if the insured had not been insured and no more than what other hospitals/doctors in the same locality would have charged."

"Equipment such as thermometers and blood glucose monitors that can be reused usually cannot be billed. However, in this case, the monitor and the 3D-laparoscope used in the surgery were sophisticated equipment used in the operation theatre," says Sudhir Sarnobat, CEO, Medimanage Insurance Broking, which services insurance accounts of Furtado's company. The equipment was used to perform a surgery advised by a doctor and, hence, should have been covered.

HOSPITALISATION

Admission in a hospital for at least 24 hours, except for specified treatments where it can be for less than 24 consecutive hours.

Among the 46 terms standardised by Irda are quite a few that have been creating problems. These bottlenecks will soon be history.

For instance, pre-existing diseases have been defined as "any condition, ailment or injury or related condition(s) for which the insured had signs or symptoms, and/or was diagnosed, received medical advice or treatment within 48 months (four years) prior to the first policy issued by the insurer." Right now, there is no time frame, and pre-existing diseases are covered after a waiting period, typically four consecutive policy years. So, such clarity is very much welcome.

This does not mean that ailments for which you have not been treated for the last 48 months will be covered as soon as you buy the policy. The norms also say that the customer should not be suffering from signs/symptoms related to the disease for the past 48 months.

Also, hospitalisation has been defined as "admission in a hospital for a minimum period of 24 'In patient Care' consecutive hours, except for specified procedures and treatments where such admission could be for a period of less than 24 consecutive hours."

Indemnity covers usually have a clause of 'minimum 24 hours of hospitalisation'; many claims are rejected on this ground alone. However, insurers are now covering day-care procedures as well.

MATERNITY EXPENSES

It will include expenses for delivery (including complicated ones and caesarean sections), lawful pregnancy termination and pre- and post-natal expenses for up to two deliveries or terminations.

"With technological advancement, the need for long hospitalisation has been greatly reduced. Procedures such as angiography, chemotherapy, dialysis, cataract, etc, require only a few hours. As many policyholders are not aware of the difference between day-care and outpatient treatments, there was a need to clear the confusion between these two," says Antony Jacob of Apollo Munich Health Insurance.

Reasonable charges have been defined as "charges for services or supplies, which are standard charges for the specific provider and consistent with the prevailing charges in the geographical area for identical or similar services."

This is not the first time that the industry has expressed the need to standardise rates. In July 2010, the four state-run health insurers-New India Assurance Company, United India Insurance Company, Oriental Insurance Company and National Insurance Company-had proposed to standardise rates for 42 procedures across hospital categories for cashless claims. Though many agreed, some big hospital chains such as Fortis, Max Healthcare and Apollo did not. They said a flat rate without accounting for the quality of infrastructure, doctors, services, etc, was not acceptable to them.

The new norms suggest something similar. But Irda has not given the method to be used for calculating the charges.

Critical IllnessA total of 11 critical illnesses/procedures have also been defined. The list includes cancer, first heart attack, coma, stroke, kidney failure, permanent paralysis, and major organ and bone marrow transplants. These will now mean the same for all insurers and plans. Companies which cover more (some cover as many as 35) critical illnesses than these 11 can continue with their definitions for the remaining ailments for the time being. But many industry experts say Irda will expand the list and redefine most critical illnesses in the coming months.

MEDICALLY NECESSARY

Any treatment, test, medication or stay in a hospital that is required... and does not exceed the level of care necessary to provide safe, adequate and appropriate medical care.

"The 11 illnesses are the major ones and covered by almost all insurers. Going forward, as companies widen their coverage of critical illnesses, we may see the regulator come out with more definitions," says Sanjay Datta, chief, Underwriting and Claims, ICICI Lombard.

Irda has also issued 199 exclusions for indemnity policies. While insurers will be free to cover these excluded items, they will not be able to exclude any expense that is not part of the standard list.

Smoother ClaimsThere is also a standard pre-authorisation procedure for cashless claims (both planned and emergency treatments). In planned treatments, hospitals will have to send the request for authorisation letters (RALs) at least seven days in advance. The insurer will have to take a call within 24 hours of receiving the RAL. However, in emergencies, hospitals need not wait for the insurer's decision and can start the treatment by charging a token amount.

The paperwork for cashless claims has also been streamlined. A common optical character recognition (OCR) format for claims and pre-authorisation forms has been annexed with the standardisation guidelines. This is expected to make processing of claims error-free and less time-consuming.

MEDICAL EXPENSES

Expenses necessarily and actually incurred on advice of a medical practitioner. These should not be more than what others charge in the locality or what would have been payable if the person had not been insured.

OCR is mechanical/electronic conversion of scanned images of text into a machine-encoded text.

"A standard form will help hospitals fill it up faster, reducing the time taken to activate the cashless facility or pass reimbursement claims," says Ravinder M, national head, Rural, Accident & Health, Tata AIG General Insurance.

At present, insurers have own claim forms with different requirements, making the process complicated and prone to errors/misinterpretation-a big reason for payment delays and claim rejections.

Vivek Nair faced such a situation when his father's fractional flow study and intra-vascular ultrasound investigations were interpreted as angiography (which had a limit of Rs 20,000 under his plan). This limit had already exhausted and hence his claim was rejected. It was only after Nair submitted a clarification from the doctor along with supporting documents that the insurer realised that these studies were not angiography. It then paid the claim.

Irda norms will ensure that all TPAs and insurers use similar OCR systems to convert text into data. Under the proposed system, documents will be scanned and processed through the OCR software. The software will "read" these images and provide electronic text as output, reducing dataentry errors.

"This will reduce complaints about wrong interpretation of complex medical situations by making the writing legible and free of errors, removing subjectivity," says V. Jagannathan, chairman and managing director, Star Health and Allied Insurance.

Standard Agreements and ClausesDiscord between the insurance company, the TPA and the hospital lowers service quality. So, Irda has brought standardisation in agreements between these three parties. At present, there are two agreements- between the TPA and the insurer and between the TPA and the hospital.

OPD TREATMENT

One in which the insured visits a clinic/hospital or associated facility like a consultation room for diagnosis and treatment based on the advice of a medical practitioner.

"Irda's move to standardise the agreement between TPAs, hospitals and insurers is aimed at ensuring that the decision to accept or reject a claim is the responsibility of insurers. The responsibility cannot be transferred to TPAs, who are only a servicing vehicle for the insurance process," says Jacob of Apollo Munich Health Insurance.

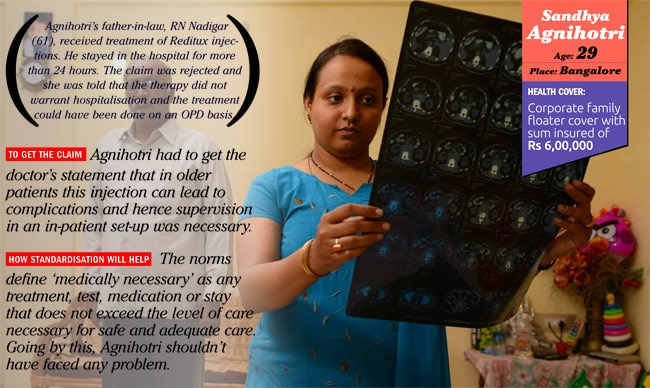

Sandhya Agnihotri's 61-year-old father-in-law, RN Nadigar, a patient of Non-Hodgkins Lymphoma (a cancer that starts in cells called lymphocytes that are part of the body's immune system) was advised a treatment of Reditux injections for which he was admitted to a hospital for a day (more than 24 hours). When Agnihotri filed a claim under her Corporate Family Floater Cover, the TPA rejected it, saying that the therapy did not warrant in-patient hospitalisation and that the injection could have been administered in the OPD, which the plan did not cover.

It was wrong. "Based on the doctor's advice and product literature, it was highlighted that the injection, if administered to old patients, may lead to heart complications or pneumonia and, hence, supervision of doctors in an in-patient set-up was necessary," says Sarnobat of Medimanage Insurance Broking, which was handling Agnihotri's case. However, after the clarification, the company decided to pay the expenses.

MEDICAL ADVICE

Any consultation or advice from a medical practitioner, including the issuance of prescription or repeat prescription.

"Such confusion arises as insurers are not aware of the processes followed by hospitals for dealing with patients and at the same time hospitals are not aware of insurers' processes/expectations," says Sarnobat. The new agreement makes the insurer the owner of the network and so accountable. This also ensures that the TPA does not use its own discretion in any process without the insurer's knowledge.

Although standardisation will make the process smoother, there will be an initial period of discomfort where all will have to go through a stage of adapting. For instance, according to the proposed regulation, an insurer dealing with multiple TPAs will need to have multiple tripartite agreements.

"This will have to be managed through a proper system which will require an increased level of management involvement. For instance, if an insurer has five TPAs and each TPA has 4,000 hospitals in the network, it will have to maintain 20,000 agreements if it enters into tripartite agreements with all. Additionally, since hospitals do not fall under Irda, it may be difficult to get their consent for so many agreements," says Joydeep Roy, CEO, L&T General Insurance. However, in the long run, it will beneficial, making processes transparent and improve service quality.

Innovation UnaffectedOne of the greatest concerns related to the new guidelines is that they will make all products look the same. But these concerns are unfounded.

HOSPITAL

Institution for in-patient care and day-care treatment with 15 beds (10 for towns with a population of less than 10 lakh), a fully-equipped operation theatre, qualified medical practitioners and nursing staff round the clock.

The norms do not talk about standardised products but standardised processes and definitions. The regulator has given insurers the freedom to add, delete and modify some of these conditions to improve their products.

Anyway, insurers will still be able to distinguish themselves from competition in terms of benefits offered and service quality. So, innovation and product design will not be hampered.

For instance, though the term co-pay has been defined, the insurer will decide how much (in percentage of sum insured) the customer will pay. Similarly, deductibles have been defined as a costsharing requirement. The regulator has left it to insurers to define whether specific deductible limits will be applied or the deductible will be applicable on per year, per life or event basis.

Also, there are features such as reinstatement of sum insured benefit or region-based pricing that some companies have adopted. These are not under the purview of the new norms. There will be a lot of scope for innovation in the industry.