Peter Lynch is a rockstar for investors around the world. One reason for this is his extensive writings where he shares, in a simple manner, how he invests. The bigger one is, perhaps, that under his stewardship as fund manager, Magellan returned an astounding 29% a year on an average. The fund beat the S&P 500, its benchmark, in 11 of the 13 years (1977-1990) during which Lynch was the fund manager.

"In my view, this is one of the very good books which investors with interest in long-term wealth creation should read. Lynch has an excellent record and tells you without jargon how he did it. He lays out his system of thinking about businesses using common sense principles," says Sanjay Bakshi, Adjunct Professor at Management Development Institute (MDI), Gurgaon.

Vikas V Gupta, fund manager, Alpha L50 (India), Arthveda Fund Management Pvt Ltd, says, "Peter Lynch was a versatile fund manager. His fund was not labelled as growth, value or mid-cap. It was a capitalappreciation fund. So, while imitating him, do so in principle and cover all the points that he mentions. If hardand-fast rules are developed with focus on select numbers, then it will be a problem."

To explain, he says that inflation and interest rates in the US when Lynch was fund manager were different from what we have in India at present. In the US, a mature company, according to Lynch, grew at 2-3% a year, close to the inflation rate. In India, the long-term inflation is close to 5-7%, requiring an adjustment of the rate at which a slow-growing company should expand.

THE PHILOSOPHY

Lynch is at his best while giving pointers on how to research a company, plus what should be looked at and what ignored. He also explains how one must classify a company based on market capitalisation and the business's life cycle.

Most important, he advises investors to stick to their field of competency, something that is also advocated by legendary investor Warren Buffett. Lynch's argument is that a doctor will always know more about medicines and hence will be in a better position to judge pharmaceutical companies than a civil engineer.

Lynch's investing strategy also involved placing companies in six categories, clearly defining expectations from them. This allows investors to identify the right focus points.

The first category is 'slow growers'. These are large companies that have been in existence for long and are expected to grow slightly faster than the country's gross national product. The most important characteristic of slow growers is that they pay regular and generous dividends. They must be included in the portfolio as a dividend cheque is always good.

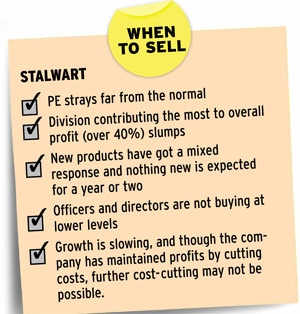

The second category is 'stalwarts'. These, too, are large, but haven't lost all the steam. Here, Lynch favours a clear strategy-investors should buy for a 30-50% gain. These companies are not meant to be held forever and should be included in the portfolio as they offer protection during recession and decent returns when market sentiment is positive.

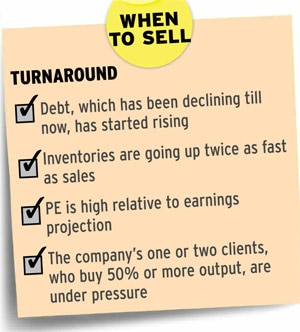

According to Lynch, the trick is to figure out when they will start slowing and what is the correct price for purchase. The third category is 'cyclicals'. Entities in this group, which includes automobile, airline, tyre, steel and chemical companies, see a rise and fall in sales and profits in a regular, if not predictable, fashion. While coming out of recession, cyclicals tend to flourish. But investors may suffer huge losses if they buy a cyclical stock at the wrong point of the cycle. Even though it is said that you should not time the market, in case of cyclical companies, timing is everything.

Once a company has been categorised, Lynch says, it's time to understand the business and reasons for investing in it. For this, he recommends that investors use the product of the company and list reasons it has the potential to beat competition. Though it sounds simple, it is not.

Lynch's another suggestion is to stay away from a company that diversifies into an unrelated business. Lynch calls this 'diworsefication'. He says investors should re-evaluate such companies. Perhaps it's best to book profit in them. He also says that one should invest in stocks only the amount that one can afford to lose as stock markets can be irrational. He also says that one should invest for the long term (5-10 years or more). He is against leverage and desists from speculation.

Lynch also suggests that before buying a stock, an investor should also check the price to equity, or PE, ratio for the last few years to get a sense of its normal level. If the company's PE is high, one must also check the PE growth rate ('PEG').

PEG = Price-to-Earnings/Per cent growth of the company

Bakshi explains this with an example from the dotcom boom. "People used PEG to justify overvalued stocks they wanted to own because they could see other people get rich (even temporarily) and did not want to be left out."

"That time many companies were growing at a torrid pace as they had started from a low base. So, people said that if they pay 100 times earnings when growth rates are 200%, the PEG ratio is only 0.5. Of course they got killed because that kind of growth was not sustainable," says Bakshi."The PEG ratio is an attempt (and a fairly crude one) to incorporate growth into a multiple and there is no US versus Indian quantitative standards. All markets are governed by the same first principles and your quantitative measures should not vary across markets," says Damodaran of Stern School of Business.

After investing, regular monitoring, at least once in six months, is a must. "Owning stock is like having children. Don't get involved with more than you can handle."