The lingering problems in Tata Steel Europe (TSE) - including high input costs, mounting losses and inability to service loans on its own - could drag down the business towards a grinding halt or a piecemeal sale of assets. Else, the Tata Steel management will have to work out another joint venture deal, like the one they planned with Thyssenkrupp AG to save its European business. TSE made operational losses in nine out of the last 12 financial years.

The company has a cumulative loss (excluding exceptional items) of about Rs 48,245 crore over the last 10 financial years. During the period, it made a profit only once - Rs 1,666 crore in 2010-11. The British subsidiary reported a non-cash accounting surplus of Rs 13,851 crore as exceptional gain in 2017-18, when it switched to the new pension scheme. This is what helped the company record a profit of Rs 11,687 crore.

Where is it leading TSE? It was pinning hopes on the proposed merger with Thyssenkrupp. But, the European Union (EU)'s powerful anti-trust authority blocked the merger, saying the deal would have pushed up prices and reduced competition. The merger intended to create the second largest steel company in the continent behind multinational giant ArcelorMittal.

Tata Steel's original plan was to reshape the company, deploying all its resources to focus back on the Indian market. According to its recent investor presentation, Tata Steel has 44 per cent of its 33 million tonne (MT) annual production from overseas and remaining 56 per cent from India. After carving out European business into tk-TSE JV and divesting its Tata Steel South East Asia operation (Singapore and Thailand businesses) and other non-core assets, it intended to move away from all its global operations, and expanding production only in India to 32 MT by 2025 from 18.5 MT now.

In January, Tata Steel had signed an agreement to sell its 70 per cent stake in South-East Asia to China's state-owned HBIS Group for $327 million. It is not sure whether Tatas will retain the rest of the 30 per cent stake, but the failure to merge the business with Thyssenkrupp leaves investors clueless as to where the European business is heading. Some of investors say that both the companies should revisit the merger plan and squeeze it complying with the norms of European Commission (EC).

"There is no clarity on the fate of TSE. They cannot survive in an environment where the UK government wants cheep import of steel from China to support other industries such as auto and food and beverages," says a foreign investor.

It was a dream comes true for Indian corporates when Tata Steel, India's oldest steel maker, acquired Anglo-Dutch giant Corus Plc (earlier name of TSE) for $12 billion (Rs 53,500 crore) in 2007, beating Brazilian steel maker CSN in a hair-raising takeover battle. The celebration inside Bombay House, the headquarter of Tata group, spilled over to next year when first full-year numbers of Corus released - the consolidated profit of Tata Steel shot up by three times and revenue by five times. Shareholders cheered as the board recommended 160 per cent dividend.

ALSO READ: BT Buzz: Does the amended Aadhaar Bill circumvent Supreme Court's order?

Tata Steel was cash surplus at the net debt level in March 2007 before the acquisition of Corus and Singapore and Thailand assets. The consolidated net debt rose to Rs 46,632 crore post acquisitions after discounting for the Rs 14,000 crore cash and current investments it had on its books. Accumulating losses in the last 10 years burdened the balance sheet and the steelmaker's consolidated debt skyrocketed to Rs 94,879 crore in March 2019, which is among the highest ones in the country.

In the domestic market, Tata Steel acquired Bhushan Steel (for Rs 36,000 crore) and steel business of Usha Martin (Rs 4,094 crore) last year. Previously, it had created 3 MT Greenfield capacity in Kalinganagar. It is now expanding it to 8MT. Despite building new capacities and acquiring assets, the standalone debt of the company has not moved up much - Rs 28,471 crore in March 2019 as compared to Rs 21,160 crore in March 2011. The company's steel-making capacity in India increased to 18.5 MT from 6.8 MT during this period. The company had funded Bhushan acquisition at a 50:50 debt-equity ratio.

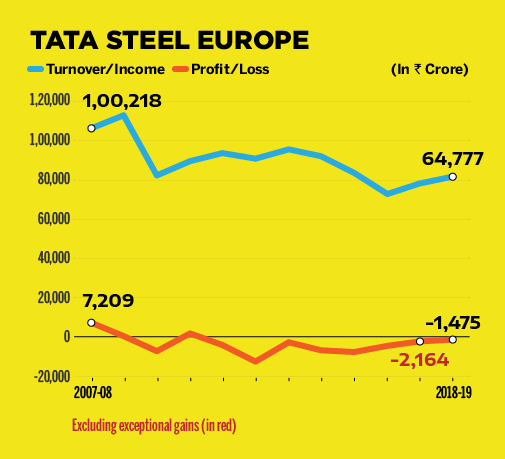

TSE never looked up

Tatas tried everything to make their European business work - idled blast furnaces, cut jobs and sold assets. In 2016, TSE sold off its Scunthorpe steel plant to Greybull Capital for one pound sterling. It represented roughly one-fourth of the Tata Steel's UK business. Greybull Capital took over largely working capital-related liabilities, but not identifiable size of debt. Tata Steel UK was reportedly losing $1 million a day in 2016, and losses were accumulating faster than the profitable Indian operations could clear them. They wrote off around $3 billion goodwill impairment from the books; invested a fresh capital of $2.5 billion to modernise plants.

Corus, which reported a topline of $18 billion (Rs 79,488 crore then) and a pre-tax net profit of $1 billion (Rs 4,416 crore then) at the time of the acquisition, made operational net losses in nine of the 12 financial years it has been managed by the Tata Group. (See Chart 1)

ALSO READ: BT Buzz: Malnutrition, healthcare system failure behind Muzaffarpur's season of despair

Cost of manufacturing for European mills is particularly high due to superior grade raw materials - pellets, coke and ferroalloys - along with environmental management costs. Besides, margins are under pressure due to higher wages and transportation costs for imported materials and expensive distribution, marketing and sales infrastructure. The employee benefits expense at TSE stood at Rs 12,444 crore in 2018-19, nearly 20 per cent of the revenue, while that of Tata Steel in India stands at 7 per cent.

Another threat for TSE's survival is the global steel prices, which have moderated since October 2018. The JV would have allowed the company to cut its exposure to its structural weaknesses of high costs and weak demand growth in Europe.

"Tata Steel had been pursuing several options for portfolio restructuring in Europe following the announcement of its plan on 29 March 2016. It had sold its unprofitable long-product business in 2016 before signing the definitive agreement for the proposed JV in June 2018. The company is still pursuing similar options for its European assets following the European Commission's rejection," Fitch said in the report. It's high time for Tata Steel to take a call on its business in Europe.

ALSO READ: BT Buzz: Early signals offer little comfort on monsoon front for that fiscal year.") Union Budget 2026: Just 0.08% of companies earned two-thirds of India Inc's profits before tax

Union Budget 2026: Just 0.08% of companies earned two-thirds of India Inc's profits before tax Joint statement on India-US trade deal in 2-3 days; $500 bn imports lined up over 5 years: Sources

Joint statement on India-US trade deal in 2-3 days; $500 bn imports lined up over 5 years: Sources Budget 2026 maintained continuity and consistency, says DEA Secretary

Budget 2026 maintained continuity and consistency, says DEA Secretary Rice exporters cheer as US cuts tariffs to 18%, boosting India’s export competitiveness

Rice exporters cheer as US cuts tariffs to 18%, boosting India’s export competitiveness 'Left, right switches checked, found satisfactory': DGCA rejects fuel switch malfunction claims on Air India Boeing 787

'Left, right switches checked, found satisfactory': DGCA rejects fuel switch malfunction claims on Air India Boeing 787 India–US Trade Deal Ignites Record Rally, Markets Add ₹20 Lakh Crore

India–US Trade Deal Ignites Record Rally, Markets Add ₹20 Lakh Crore 21-Year Tax Holiday Clears The Path For India’s GCC Boom, Where's The Big Opportunities?

21-Year Tax Holiday Clears The Path For India’s GCC Boom, Where's The Big Opportunities? India–US Trade Deal Sparks Massive Market Rally | Amit Goel Explains

India–US Trade Deal Sparks Massive Market Rally | Amit Goel Explains India–US Trade Deal After Tariff War: Trump Slashes Tariffs, Modi Welcomes Trade Reset

India–US Trade Deal After Tariff War: Trump Slashes Tariffs, Modi Welcomes Trade Reset India-US Deal: Not A Blanket Cut, But A Big Boost | Fine Print Matters

India-US Deal: Not A Blanket Cut, But A Big Boost | Fine Print Matters Bajaj Housing shares up 2% after Q3 results: What lies ahead for investors?

Bajaj Housing shares up 2% after Q3 results: What lies ahead for investors? IREDA shares climb 2%, snapping 4-session fall; trend still cautious or reversal sign?

IREDA shares climb 2%, snapping 4-session fall; trend still cautious or reversal sign? Sensex, Nifty roar back with 2.5% surge as India-US trade deal brightens outlook for markets, rupee

Sensex, Nifty roar back with 2.5% surge as India-US trade deal brightens outlook for markets, rupee Solar Industries Q3 earnings: Defence firm logs highest revenue, EBITDA; stock ends higher

Solar Industries Q3 earnings: Defence firm logs highest revenue, EBITDA; stock ends higher  Adani Enterprises Q3 earnings: Net profit surges 97 times; stock zooms 12%

Adani Enterprises Q3 earnings: Net profit surges 97 times; stock zooms 12%