Banks such as HDFC Bank an SBI are looking to improve or maintain NIMs while others such as ICICI Bank and Axis Bank generally prefer higher NIM over growth.

Banks such as HDFC Bank an SBI are looking to improve or maintain NIMs while others such as ICICI Bank and Axis Bank generally prefer higher NIM over growth. Banks such as HDFC Bank an SBI are looking to improve or maintain NIMs while others such as ICICI Bank and Axis Bank generally prefer higher NIM over growth.

Banks such as HDFC Bank an SBI are looking to improve or maintain NIMs while others such as ICICI Bank and Axis Bank generally prefer higher NIM over growth.With the Reserve Bank of India (RBI) kicking off the policy easing cycle with a 25 basis points rate cut, the move is expected to hit net interest margin (NIM) of lenders in the short term. That said, the central bank's assurance to actively manage liquidity positions and postponing of some of the key regulatory aspects such as ECL, LCR and project finance guidelines, which could have been onerous under current circumstances, offer a sigh of relief in the near term, brokerages such as Elara Securities said.

"Expect NIMs to be under strain, more so for larger banks. Our sensitivity analysis (factoring in a 50bps rate cute for the full-year FY26E) with certain assumptions indicate: a) higher impact of 15-17bps on larger private banks, 3-5bps impact on mid-sized banks, 15-17bps impact on regional private banks, positive impact on some small finance banks and 10-20bps impact on PSU banks," Elara said.

With re-calibrated growth, balancing NIMs amid rate cut will be the key monitorable for players to deliver on core performance, it said.

MOFSL said private banks, with higher exposure to repo-linked loans, will face immediate margin pressure from rate cuts. Lenders with a greater share of fixed-rate loans, such as AU SFB, IndusInd Bank and Equitas, will be more resilient. PSBs, benefiting from MCLR-linked repricing, are likely to exhibit relative stability, it said.

The banking system has witnessed significant NIM compression over the past one and a half years, led by the repricing of funding costs, while loan yields moved in a narrow range.

Among private sector banks, lenders such as ICICI Bank, Axis Bank and Kotak Mahindra Bank have reported an 18 bps, 8 bps and 29 bps dip in margins, respectively, over the past one year. Margins for a few lenders have already dipped below the pre-rate-hike levels that started in 1QFY23.

While the consensus expectation is of a shallow rate cycle, MOFSL believe that NIMs for most banks will move one full circle and revert towards the pre-rate hike cycle by the end of FY26. PSBs are relatively better placed with a higher mix of MCLR loans and thus will likely report more resilient performance on the margin front, it said.

"Banking sector margins will remain under pressure with earnings growth expected to bottom out in FY26. Private banks are projected to deliver PAT growth of 10.8 per cent and 17.2 per cent YoY in FY26 and FY27, while PSBs will grow at 5.6 per cent and 11.1 per cent. Our top picks are: ICICI Bank, HDFC Bank, SBI, and AUBANK," it said.

Kotak Institutional Equities said a few large lenders such as HDFC Bank an SBI are looking to improve or maintain NIMs while others such as ICICI Bank and Axis Bank generally prefer higher NIM over growth. Most public banks have looked at growth a lot less favorably despite better liquidity (lower CD ratio), lower cost of deposits and better tier-1 ratio.

"With several banks focusing a lot more on NIM than growth, we see this as a higher probability but we need evidence of the same in the coming few weeks. Else, much of the earnings support has to come through lower credit costs and tighter cost controls, which tend to have a lower level of confidence, as it not sustainable," Kotak said.

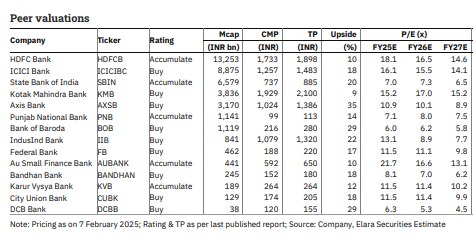

Target prices for bank stocks

Elara Securities has 'Accumulate' ratings on Punjab National Bank, AU SFB, Karur Vyvsa Bank, State Bank of India and HDFC Bank, It has 'Buy' ratings on IndusInd Bank, Federal Bank, DCB Bank, City Union Bank, Axis Bank, Kotak Mahindra Bank, Bank of Baroda and Bandhan Bank, among others.

Claims of sovereignty loss in India-US trade deal ‘absolute nonsense’: Piyush Goyal

Claims of sovereignty loss in India-US trade deal ‘absolute nonsense’: Piyush Goyal SEBI draws line between listing norms and RBI rules in guidance to PNB

SEBI draws line between listing norms and RBI rules in guidance to PNB") India’s US oil imports are strategic decisions, not trade pact obligations: Piyush Goyal

India’s US oil imports are strategic decisions, not trade pact obligations: Piyush Goyal Domestic airfares set to rise as IndiGo capacity cuts hit summer schedule: Report

Domestic airfares set to rise as IndiGo capacity cuts hit summer schedule: Report 'True luxury is here to stay’: Isprava’s Dhimaan Shah

'True luxury is here to stay’: Isprava’s Dhimaan Shah BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion

BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion Golf Is An Addiction. We Eat And Sleep Golf!

Golf Is An Addiction. We Eat And Sleep Golf! The Fairway Fixes Everything. Mindset, Life, Relationships

The Fairway Fixes Everything. Mindset, Life, Relationships BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala

BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise

AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s why

RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s why NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji

NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves

SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week