Photo: ReutersPhoto: Reuters

Photo: ReutersPhoto: Reuters

The Indian rupee appreciated by around two per cent on fresh dollar selling by exporters and some banks along with debt purchases by foreign institutions and gains in the local equity market. Also, statement by trade secretary Rajeev Kher that India's gold imports fell to 39 tonnes in December and were placed at 7 tonnes in the first week of January, compared with 152 tonnes in November, supported the rupee.

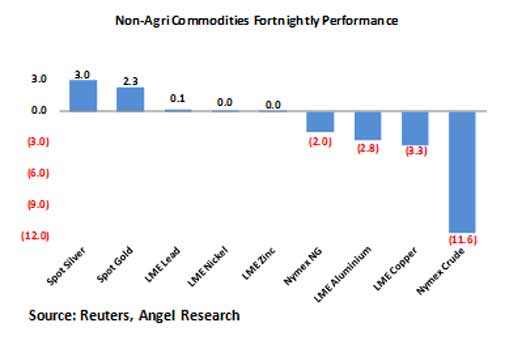

In the past fortnight, spot gold prices rose by 2.34 per cent while MCX gold prices declined by 1.01 per cent as the rupee appreciated. The impact of a stronger dollar was partially offset by demand from investors worried about tensions in Russia and political uncertainty in Greece.

Despite recent improvements in the job market, investors remained focused on the fact that minutes of the Federal Reserve's latest policy meeting released last week indicated that the US central bank would be patient in raising interest rates due to low inflation expectations. Gold prices rose to a three-week high having touched a peak of $1,222.40, its highest since Dec. 15. On the flip side, investor holdings in exchange-traded funds backed by gold last week were the lowest since 2009 suggesting falling investment demand for the yellow metal.

International spot silver prices rose by 3 per cent and MCX silver prices declined by around 1.3 per cent in the past fortnight. However, strength in the dollar index, which is at its highest point in last nine years, and weakness in copper prices capped the rally. In the Indian markets, silver prices declined on account of the rupee appreciation.

LME Copper prices plunged by 3.3 per cent during the last fortnight as China's factory-gate prices extended a record run of declines, signaling weakening demand in the world's largest metals user. In addition, concerns of Greece exiting the euro zone weighed on markets across the globe. Concerns that a supply surplus will hit the market next year just as Chinese economic growth shifts down another gear acted as a negative factor. Moreover, China introduced a new export tax rebate for some copper products in a move expected to increase copper product shipments by as much as tenfold. Also, FOMC meeting minutes indicated towards rate hike in 2015 exerted downside pressure on prices. MCX copper prices fell by 4.6 per cent in the last 15 days owing to the rupee appreciation.

WTI and Brent oil prices lost have declined by around 12 and 16 per cent in the past fortnight while MCX oil prices fell 16 per cent. The selloff in global oil markets showed few signs of slowing in the New Year, the lowest since spring 2009, as fears deepened a supply glut that has vexed the market for six months would continue. US driller ConocoPhillips added to the bearish mood by announcing it struck first oil at a Norwegian North Sea project. Top crude exporter Saudi Arabia revealed it made deep cuts to its monthly oil prices for European buyers, the sixth time since June it has slashed prices, corresponding with the rout in crude futures markets over the period.

Outlook

Gold and silver prices are expected to trade lower as waning investment demand, growth and optimism in the US economy, strength in the dollar index will exert downside pressure on prices.

Crude oil prices will continue to see weakness as ample supplies and bleak demand will exert downside pressure. The rupee's appreciation will drag prices further in the Indian markets.

Base metals are likely to trade lower in the coming fortnight as weak manufacturing data from China and the US, the world's biggest consumers, will exert downside pressure on prices. Also, rising risk aversion in the markets owing to Greece concerns will continue to drag prices lower.

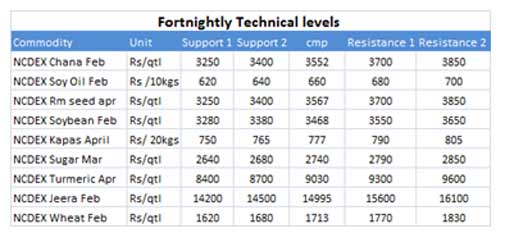

In the ongoing rabi season, chana sowing is lower by 18 per cent at 8.10 million hectares, as compared with 9.58 mn ha last year. During Apr-Sep 2014, Indian imports of chickpea from Australia and Tanzania stood around Rs 1.29 lakh metric tonne, much less than 2.76 lakh tonne the previous year.

For further movement, data of crop production, import volumes and acreage will provide direction to pulses prices. The decision to postpone the duty hike has kept speculators away and prompted them to offload their positions. We expect that weak spot market demand and adequate stocks position might keep pressure on chana futures.

Edible oils: We saw mixed to positive trend in price movement in futures market last fortnight. Refined soy oil and CPO traded on a positive note due to Malaysian flood worried traders over supply of vegetable oil. Prices in international markets have improved due to reports on palm oil output decline by 20 per cent during Dec 14 to Jan 15 as severe flooding disrupts harvesting exacerbating a seasonal drop in production and also on Chinese demand projections.

Global soybean production is projected at a record 312.8 MT in Dec 2014/15, up 9.6 per cent compared to 2013/14 estimates. However, US soybean futures rose for the third consecutive session last week, amid concerns about damage to crops from dry weather in key South American growers.

US soybean export demand prospects are improving and at the same time cold weather in the US might boost demand for animal food. The USDA reports weekly net soybean sales were 910,600 MT, a 49 per cent increase from last week.

Edible oil is expected to trade higher in the coming fortnight due to restricted supply of palm oil from Malaysia and seasonal demand in domestic market.

Sugar: We have witnessed a range-bound movement in sugar prices. Prices increased 0.70 per cent last fortnight on expectation of export subsidy on raw sugar. The government is considering extending subsidy on raw sugar exports for the ongoing marketing year 2014/15 by giving a higher incentive of Rs 4,000 per tonne to cash-starved mills.

Meanwhile, domestic sugar production reached 7.46 million tonnes during Oct-Dec 2014, as against 5.88 million tonnes a year ago, a rise of 27.3 per cent.

Sugar production is all set to outstrip demand for the fifth year in a row and world has huge carry-over stocks. Brazil, the world's largest producer, could shift more sugarcane for sugar output than ethanol in view of steep fall in global crude oil prices. It is also reported that EU sugar production might increase by 12 per cent this marketing year.

We are expecting sugar prices to trade on a mixed note due to export subsidy and pressure from the record production and ample supplies of sugar carryover stock in physical market.

Spices: Last fortnight, the spice segment traded mixed to negative. Jeera dropped 6.6 per cent as market participants offloaded positions in the futures market due to profit-booking at prevailing higher levels. The prices were down last week, despite 42 per cent drop in acreage in Gujarat, good export demand and tight supply in spot market. But good demand in spot market coupled with the slight expected delay of new crop due to late sowing and tension in Turkey and Syria might support prices.

Turmeric traded on a mixed note in the fortnight on technical reasons as the market participants offloaded their positions on higher levels for profit booking. Good quality arrivals, lesser expected production and good export demand will restrict the fall. As per trade sources, crop in Nizamabad and Maharashtra might be 12 to 13 per cent lower, which may support the prices further.

Dhaniya traded on a mixed to negative note on sluggish trading activity and reports of record sowing in Gujarat. Market participants are more interested towards reducing positions amid ample stocks in the spot market against sluggish demand.

We are expecting spices segment will trade on a positive note on account of export inquiries in Jeera and good demand in Turmeric. Dhaniya will trade mixed on expectation of good supplies and lower levels demand.

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal 'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got

'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got Cyberattack impact on Tata Motors PV earnings crosses Rs 3,200 crore; losses still mounting

Cyberattack impact on Tata Motors PV earnings crosses Rs 3,200 crore; losses still mounting 'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market.") Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma

Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma Golf & Life: Handling Every High And Low

Golf & Life: Handling Every High And Low It’s Time More Women Picked Up The Club. Golf Welcomes Women At Every Stage Of Life.

It’s Time More Women Picked Up The Club. Golf Welcomes Women At Every Stage Of Life. RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook

RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.”

Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.” Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation

Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves

SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates

Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates 'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag

'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag