After ICICI Prudential Life, ICICI Lombard and SBI Life it is now the turn of General Insurance Corporation of India (GIC), a reinsurance company, to make the most in the IPO market. While life and non-life insurers have got listed, this is the first time that a reinsurance company is getting listed in the Indian market with an issue size of Rs 11,372 crore. The price band of GIC is at Rs 855-Rs912 and is open from 11th October to 13th October 2017. The biggest IPO so far has been of Coal India that raised Rs15,200 through its public offering.

GIC is one of the oldest and the largest reinsurer which provides reinsurance across business lines including fire, marine, motor, engineering, agriculture, health, liability, credit and financial and life insurance. Reinsurance is insurance that is purchased by an insurance company from another insurance company to mitigate their risks. A company that provides insurance to an insurance company is called a reinsurance company.

GIC is the sole national reinsurer. It has significant presence in the local market as well as international market. To give you an idea it underwrote business from 161 countries as on June 30, 2017. According to CRISIL Research, it ranked as the 12th largest global reinsurer in 2016 and the 3rd largest Asian reinsurer in 2015, in terms of gross premiums accepted.

Considering insurance is a complicated business which takes into account the value of future business as well let's look at the financials and valuation of GIC.

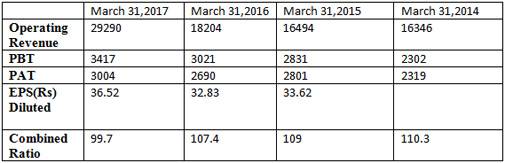

GIC Re Financials (Rs in Crore)

Price Earning and Price to Book Value: At the upper price band of Rs 912 the stock is available at P/BV of 1.6 times and P/E of 23 times based on FY17 EPS. Considering there are no listed reinsurance companies in India comparison with its peers is not possible. However, compared to other listings in the insurance space GIC looks fairly valued when compared with 46 times P/E ratio of ICICI Lombard.

Combined ratio: The combined ratio of the company was at 99.7 during 2016-2017. Though after years of high combined ratio they have managed it to bring below 100% the concern remains as GIC's share has been increasing big time in the agriculture sector. The combined ratio is calculated by taking the sum of incurred losses and expenses and then dividing them by earned premium.

The corporation has seen a huge jump in the agri reinsurance premium from Rs 644 crore in March 2015 to Rs 9,752 crore in March 2017. The growth in agriculture premium has been on account of Pradhan Mantri Fasal Bima Yojana (PMFBY). PMFBY was approved in 2016 under which premium of 2 percent to be paid by farmers for all kharif crops and 1.5 percent for all rabi crops. The rest of the premium is paid by the government.

Growth: The company's gross premium has witnessed a CAGR of 48.6% over FY15-17, driven by 64.5% CAGR in domestic premium. Owing to high growth of non-life and life insurance businesses and being a leader in the market, GIC Re should grow at a steady rate in coming years. Another positive is 30% of the GIC business comes from the international market which not only mitigates its risks but also provide ground for further expansion.

A report from Arihant Capital states, "based on qualitative pointers, robust past growth and future potential, strengths and management quality we have "4 star" rating for the issue."

IIFL Private Wealth has also recommend subscribe stating "gross premium growth for GIC Re should remain sturdy in the coming years owing to a) sustained brisk growth in Indian non-life insurance industry b) expanding reinsurance market in India and c) tapping of new global markets including the largest ones. The potent combo of likely inroads into global market along with better pricing in domestic market should further improve the combined ratio in the medium term, save for any untoward loss. At the IPO price of Rs 912, GIC Re is reasonably valued at 3.6x P/BV on a post money basis."

Union Budget 2026 may unveil targeted boosters for labour-intensive sectors

Union Budget 2026 may unveil targeted boosters for labour-intensive sectors India-EU FTA to be announced in Delhi today: Defence partnership, mobility framework - Check full schedule

India-EU FTA to be announced in Delhi today: Defence partnership, mobility framework - Check full schedule Top stocks in news: Kotak Bank, HCL Tech, Axis Bank, Hindustan Copper, Urban Company, BPCL

Top stocks in news: Kotak Bank, HCL Tech, Axis Bank, Hindustan Copper, Urban Company, BPCL Mark Carney’s India visit in early March may seal C$2.8 bn uranium supply agreement: Report

Mark Carney’s India visit in early March may seal C$2.8 bn uranium supply agreement: Report Successful India key to global stability: EU chief ahead of India-EU Summit talks

Successful India key to global stability: EU chief ahead of India-EU Summit talks Rajdeep Sardesai & Siddharth Zarabi On The Big Takeways From WEF, Davos

Rajdeep Sardesai & Siddharth Zarabi On The Big Takeways From WEF, Davos Davos 2026 | Global Investors Back Maharashtra For Frontier Tech & Space Innovation

Davos 2026 | Global Investors Back Maharashtra For Frontier Tech & Space Innovation AI Security Testing Improves, Yet Vulnerabilities Remain A Major Global Risk

AI Security Testing Improves, Yet Vulnerabilities Remain A Major Global Risk Why Global Tech Leaders Are Betting Big On India’s AI Mission | Davos 2026

Why Global Tech Leaders Are Betting Big On India’s AI Mission | Davos 2026 Europe, Asia And The New Reality: WEF Davos 2026 Exposes A Fracturing World OrderTop stocks in news: Kotak Bank, HCL Tech, Axis Bank, Hindustan Copper, Urban Company, BPCL

Europe, Asia And The New Reality: WEF Davos 2026 Exposes A Fracturing World OrderTop stocks in news: Kotak Bank, HCL Tech, Axis Bank, Hindustan Copper, Urban Company, BPCL Markets track Iran-US tensions, India-EU trade deal amid key global developments

Markets track Iran-US tensions, India-EU trade deal amid key global developments Adani Total Gas shares hit 52-week low; company issues clarification on 'US regulator report'

Adani Total Gas shares hit 52-week low; company issues clarification on 'US regulator report' Eternal shares slip 30% from record high in three months; what's next?

Eternal shares slip 30% from record high in three months; what's next? Multibagger Tata Group stock in correction mode, oversold on charts; time to buy?

Multibagger Tata Group stock in correction mode, oversold on charts; time to buy?